What Is the Corebridge Power 7 Protector?

The Corebridge Power 7 Protector (official product brochure) is a 7-year accumulation fixed index annuity issued by American General Life Insurance Company (AGL), a wholly owned subsidiary of Corebridge Financial. It is the short-surrender member of the Power Series Protector family, and it is built for one job: protected, tax-deferred growth without a premium bonus, without an income rider, and without the fees that pay for either. The headline numbers are a 9.6% S&P 500 annual point-to-point cap, a 52% uncapped S&P 500 participation rate, and a 4% one-year fixed account as of July 2026.

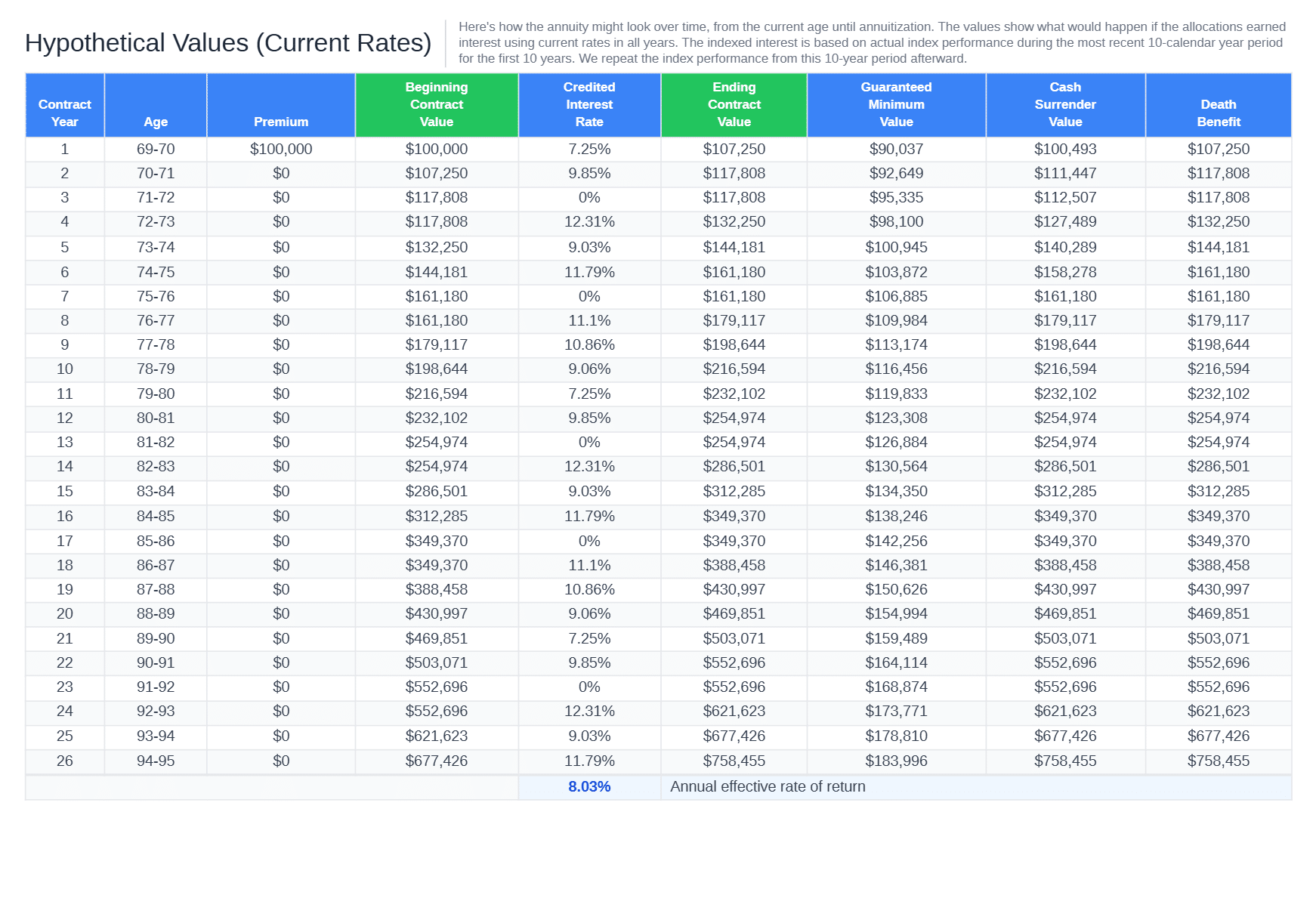

On a live illustration we ran on July 20, 2026 for a male annuitant age 69 with a $100,000 non-qualified premium in Arizona, a 50/50 allocation between the two S&P 500 strategies produced an accumulation value of $216,594 after 10 years using current rates against the most recent 10-year index performance. That is an 8.03% annualized effective return with a zero floor in negative index years. This review is built on that illustration, and we show you the carrier’s own low-scenario numbers alongside the headline figure, because the gap between the two is where the real buying decision lives.

Power 7 Protector at a Glance

| Feature | Details |

|---|---|

| Product Type | Fixed Index Annuity (FIA), accumulation-focused, no living benefit rider |

| Issuing Carrier | American General Life Insurance Company (AGL), member of Corebridge Financial |

| Surrender Period | 7 years |

| Surrender Schedule | 8% / 7% / 6% / 5% / 4% / 3% / 2% |

| Premium Bonus | None |

| Rider Fee | None (optional 1.5% annual fee applies only to the four Enhanced crediting accounts) |

| Minimum Premium | $25,000 (qualified and non-qualified) |

| Maximum Premium | $2,000,000 (higher with home office approval) |

| Additional Premium Window | 30 days after issue, $100 minimum additional |

| Issue Ages | 18 to 85 (owner and annuitant), annuitization by age 95 |

| Free Withdrawal | 10% of contract value annually (based on prior anniversary value), not cumulative |

| Market Value Adjustment | Yes, on excess withdrawals and annuitization during the 7-year surrender period, tied to the Barclays US Credit Index yield |

| Guaranteed Minimum Cash Surrender Value | 87.5% of premium (90% in NJ), currently growing at 2.9% annual interest |

| Death Benefit | Greater of contract value or minimum withdrawal value, avoids probate |

| Charge Waivers | Nursing home, terminal illness, extended care (extended care waiver ends at age 86; state-dependent) |

| AM Best Rating | A (Excellent) |

| Comdex Score | 82 |

| State Availability | All states except Guam, Idaho, New York, Puerto Rico, and the U.S. Virgin Islands |

Is Corebridge a Good Annuity Company?

Corebridge Financial is the publicly traded life insurance and retirement business that was spun off from AIG in September 2022 and is now majority-owned by Brookfield Reinsurance. The issuing entity for the Power 7 Protector, American General Life Insurance Company, has been writing life and annuity contracts since 1919 and is one of the largest annuity issuers in the United States. Corebridge has consistently ranked as the third-largest fixed indexed annuity carrier nationally, posting $10.0 billion in FIA sales in 2025 (see our FIA industry sales history for the full 11-year carrier ranking).

The financial strength profile is strong across all four major rating agencies as of July 2026:

| Rating Agency | Rating |

|---|---|

| AM Best | A (Excellent) |

| Standard & Poor’s | A+ |

| Fitch | A+ |

| Moody’s | A2 |

| Comdex Composite | 82 |

For more on Corebridge’s history, ownership transitions, and complete product lineup, see our full Corebridge Financial Annuity Review.

Index Options and Current Rates

The Power 7 Protector offers 16 indexed crediting strategies across four indices (S&P 500, ML Strategic Balanced, AQR DynamiQ Allocation, and PIMCO Global Optima), plus a 1-year fixed account paying 4% as of July 2026. Ten strategies reset annually and six reset every two years. To see how these stack up against every FIA we track, compare current fixed index annuity rates.

Current Rates: 1-Year Reset Strategies

| Strategy | Crediting | Fee | Recent 10-yr Annualized |

|---|---|---|---|

| S&P 500 Enhanced Participation | 62% participation | 1.5% | 10.05% |

| S&P 500 Participation | 52% participation | None | 8.45% |

| S&P 500 Cap | 9.6% cap | None | 7.60% |

| AQR DynamiQ Enhanced Participation | 235% participation | 1.5% | 7.60% |

| ML Strategic Balanced Enhanced Participation | 140% participation | 1.5% | 7.40% |

| PIMCO Global Optima Enhanced Participation | 95% participation | 1.5% | 6.74% |

| ML Strategic Balanced Participation | 110% participation | None | 5.84% |

| S&P 500 Performance Triggered | 7% trigger | None | 5.56% |

| AQR DynamiQ Participation | 165% participation | None | 5.41% |

| PIMCO Global Optima Participation | 70% participation | None | 5.00% |

Current Rates: 2-Year Reset Strategies and Fixed Account

| Strategy | Crediting | Fee | Recent 10-yr Annualized |

|---|---|---|---|

| 2-Yr ML Strategic Balanced Enhanced Participation | 190% participation | 1.5% annually | 8.08% |

| 2-Yr PIMCO Global Optima Enhanced Participation | 135% participation | 1.5% annually | 7.32% |

| 2-Yr AQR DynamiQ Enhanced Participation | 315% participation | 1.5% annually | 7.05% |

| 2-Yr ML Strategic Balanced Participation | 140% participation | None | 6.04% |

| 2-Yr PIMCO Global Optima Participation | 100% participation | None | 5.53% |

| 2-Yr AQR DynamiQ Participation | 240% participation | None | 5.48% |

| 1-Year Fixed Account | 4.00% | None | 1% contractual minimum after year 1 |

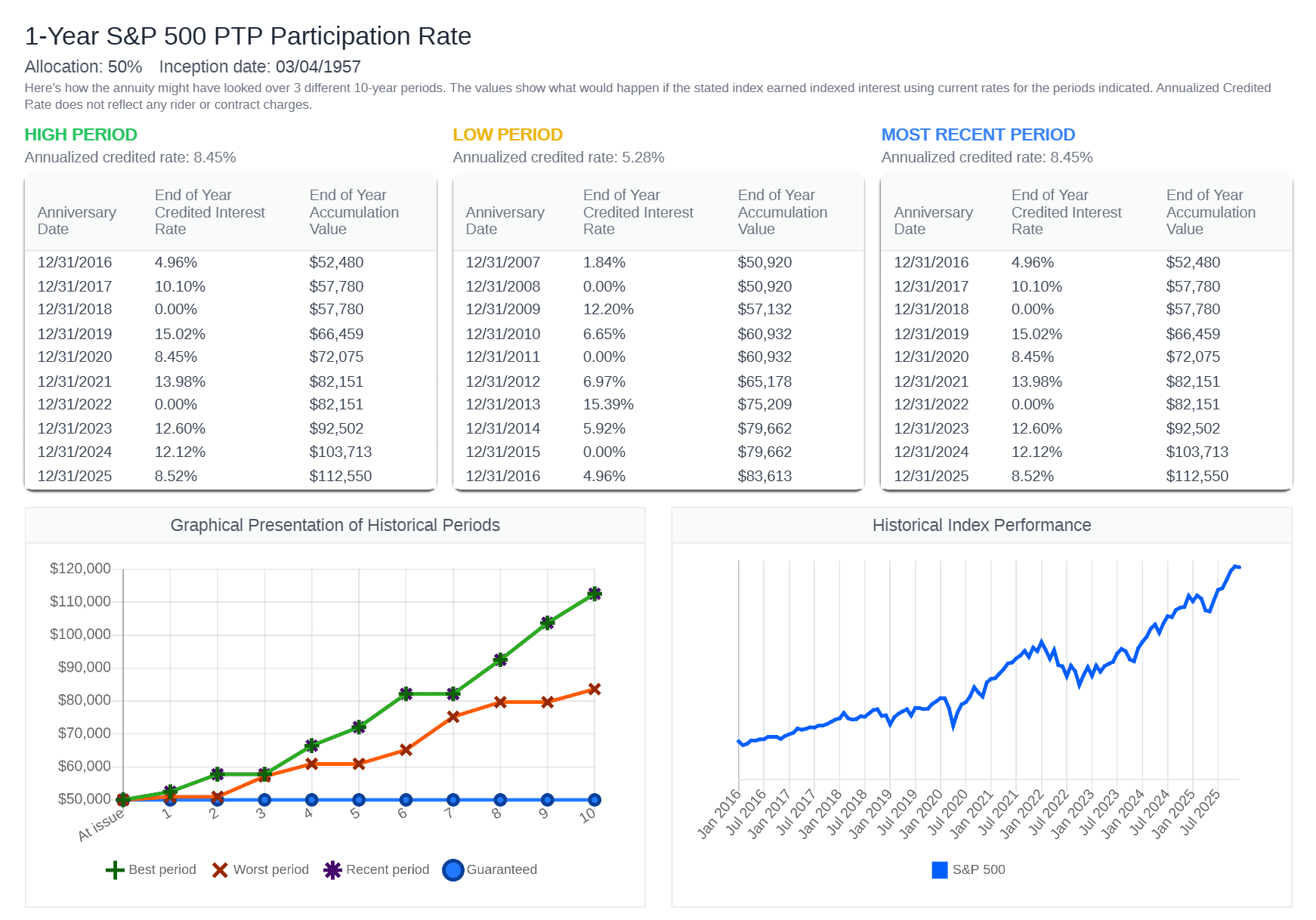

The standouts are the two plain S&P 500 accounts. A 9.6% annual point-to-point cap is genuinely competitive for a 7-year FIA in the current rate environment, and the 52% uncapped participation option credited as much as 15.02% in a single year of the illustrated period. These two no-fee strategies, on a transparent index with nearly seven decades of real history, are the reason to buy this product.

Two cautions on the rest of the menu. First, the enormous participation rates on the volatility-controlled indices (235% on AQR DynamiQ, 315% on the 2-year version) look spectacular, but their own backtests land at just 5.41% to 7.60% annualized. Volatility-controlled indices dampen their own movement by design, so the insurer can afford a huge multiplier on returns that are structurally small. To Corebridge’s credit, these indices come from established managers rather than a months-old custom index, but the math still says the giant numbers are marketing surface area, not extra return. For a deeper look at how these volatility-controlled structures actually work, see our Merrill Lynch Strategic Balanced Index review (MLSB is one of this product’s core index options) and our PIMCO Tactical Balanced ER Index review.

Second, and more important: the four Enhanced accounts charge a 1.5% annual fee that is deducted even in years the index credits 0%. In a flat or down year, an Enhanced allocation loses 1.5% of value. That quietly breaks the “Power of Zero” promise on those specific accounts, and Corebridge’s own brochure footnotes concede that contract value can be reduced by account fees in prolonged down markets. Most buyers drawn to an FIA for the no-loss guarantee should stick to the no-fee accounts.

Hypothetical Historical Rate of Return

We ran a live illustration on July 20, 2026 for a male annuitant age 69 with a $100,000 non-qualified premium in Arizona, allocated 50% to the S&P 500 participation account (52% participation) and 50% to the S&P 500 cap account (9.6% cap). Using actual S&P 500 performance from the most recent 10 calendar years at current rates, the blend produced an 8.03% annual effective rate, growing $100,000 to $216,594 in 10 years:

Treat that 8.03% the way the fine print tells you to. The most recent 10-year window contained one of the strongest equity runs in market history, with only two zero-credit years (2018 and 2022). The same illustration’s own low-period windows tell the honest story. Over the worst 10-year stretch shown, which begins in 2007 and runs straight into the financial crisis, the participation account earned 5.28% annualized and the cap account earned 6.02%:

That low-period range is the number to weigh against a MYGA. The realistic framing for the Power 7 Protector’s S&P accounts is this: in a bad decade you roughly match what a top multi-year guaranteed annuity pays today, in a strong decade you meaningfully beat it (the high-period windows ran 7.60% to 8.45%), and in every scenario the no-fee accounts can never credit less than zero. That is a fair trade, and it is a much more defensible pitch than the 8.03% headline alone.

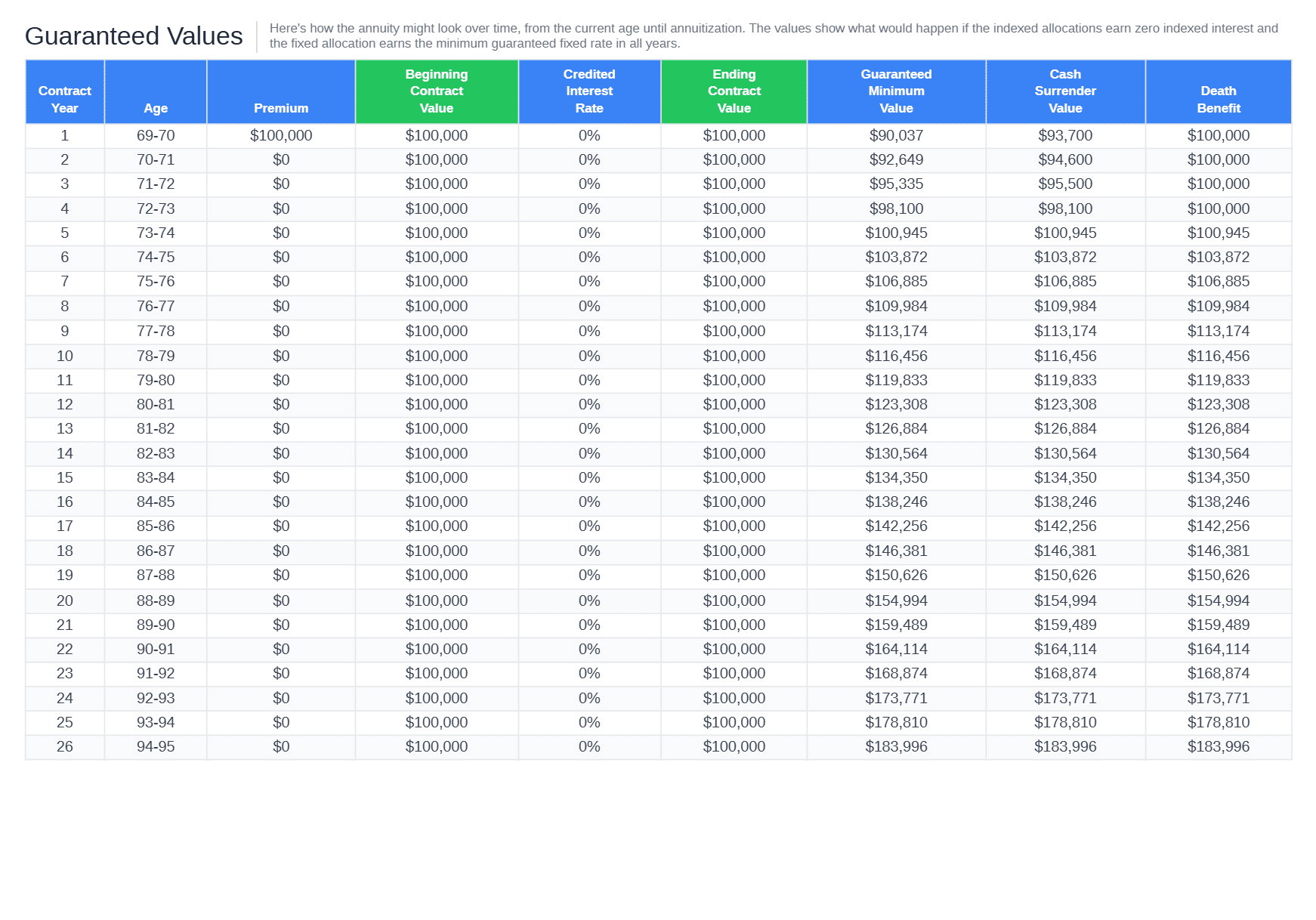

The Guaranteed Floor: What If the Index Never Pays?

If the index accounts credited zero every single year, the contract value would simply stay at $100,000. The Minimum Withdrawal Value, which starts at 87.5% of premium and currently grows at 2.9% annually, crosses above the original premium in year 5 and reaches $116,456 by year 10:

Understand what that floor is and is not. It is protection from market-based losses: index goes down, you lose nothing on the no-fee accounts. It is not a return-of-premium guarantee on early exit. Surrender in year one of our illustration and the cash value is $93,700 on a $100,000 premium, a 6.3% haircut from the surrender charge. The brochure’s own worst-case framing, that you get your money back through the minimum withdrawal value “after 14 years,” reflects the lower contractual minimum interest rate rather than the current 2.9%.

Surrender Schedule, Liquidity, and the MVA

The 7-year schedule (8%, 7%, 6%, 5%, 4%, 3%, 2%) is middle-of-the-pack at the front and friendlier than most at the back; plenty of competing 7-year FIAs still charge 4% to 5% in year seven. Free withdrawals are 10% of contract value based on the prior anniversary value, which is modestly better than premium-based free withdrawals once the contract has grown. They are not cumulative: skip a year and you do not get 20% the next.

The Market Value Adjustment applies to excess withdrawals and annuitization during all 7 surrender years and keys off changes in the Barclays US Credit Index yield since issue. It can work in your favor if rates fall and against you if rates rise. The formula itself is not disclosed in the illustration materials, so ask for the contract’s MVA specification before signing if an early exit is a realistic scenario for you.

The waiver package is better than average: nursing home, terminal illness (one partial or full withdrawal), and an extended care waiver requiring a 90-consecutive-day qualifying stay after a 1-year deferral. The catch worth knowing: the extended care waiver terminates at age 86. For a 69-year-old buyer that means 17 years of coverage; for an 80-year-old buyer it means 6.

No Bonus, No Income Rider, No Gimmicks

The Power 7 Protector has no premium bonus, and we mean that as a compliment. Bonus FIAs recover their bonus through some combination of longer surrender schedules, lower caps, and higher fees; Corebridge’s own disclosure language says exactly that. This product puts its budget into a 9.6% S&P cap and a 4% fixed account instead of a headline giveaway.

There is also no guaranteed living benefit rider, so there is no rider fee, no benefit-base shell game, and no rollup math to audit. Lifetime income is available only through annuitization, which is built into every annuity contract at no cost. Corebridge sells the rider version separately as the Power 7 Protector Plus Income, which pays for its income guarantee with lower crediting rates. For the right buyer this is a feature, not a gap: if you are shopping for guaranteed lifetime income, this is simply the wrong product. If you are shopping for protected accumulation, the absence of a rider is exactly why the rates here are as strong as they are.

What We Like

- A 9.6% S&P 500 annual cap on a no-fee account is at the competitive end for 7-year FIAs right now, and the 52% uncapped participation alternative credited as much as 15.02% in a single illustrated year.

- A 4% one-year fixed account gives conservative money a real parking spot inside the contract, not the token 1% to 2% fixed rate many FIAs offer.

- The 7-year schedule ends at 2%, and the 10% free withdrawal is based on contract value rather than premium.

- No bonus recapture and no rider fees on the core accounts. The two no-fee S&P 500 strategies are among the most transparent FIA allocations available: a public index, annual reset, one number to understand.

- Corebridge is a substantial carrier: A from AM Best, A+ from Standard & Poor’s and Fitch, roots back to 1919, and a Comdex of 82.

What Gives Us Pause

- The 1.5% annual fee on the four Enhanced accounts undermines the product’s own “Power of Zero” pitch. A zero-credit year on those accounts is a negative 1.5% year.

- The 87.5% minimum withdrawal value plus an 8% year-one charge makes early exits genuinely expensive, and the MVA can deepen that in a rising-rate environment. Year-one cash surrender value in our illustration: $93,700.

- Ten of the sixteen index strategies backtest below 7%, and several backtest below what a guaranteed MYGA pays today. The menu is wide, but most of it is filler around the two good S&P accounts.

- Free withdrawals are not cumulative, and the extended care waiver ends at age 86, which limits its value for the older buyers a 7-year product naturally attracts.

- A Comdex of 82 is solid but not elite. Buyers who rank carrier strength above everything else can find FIAs from carriers scoring in the 90s, though usually with less competitive rates.

Who the Power 7 Protector Is Best For

Best for: a buyer in their 60s or 70s moving CD, MYGA, or excess-cash money who wants S&P 500-linked upside with no market-loss risk, plans to hold at least 7 years, and does not need an income rider. Our illustrated profile, a 69-year-old with $100,000 of non-qualified money split between the two S&P accounts, is close to the ideal use case. The 85 maximum issue age also makes it one of the options still open to buyers in their early 80s who want a shorter commitment.

It is not the right contract for buyers who want guaranteed lifetime income (see the Power 7 Protector Plus Income or a dedicated income FIA), who may need more than 10% of the money in any year before year 8, who live in New York or Idaho where it is not available, or who are drawn to the 235% to 315% participation headlines expecting equity-like returns. The backtests say those accounts are 5% to 8% strategies.

How It Compares to Other Accumulation FIAs

The Power 7 Protector’s most direct comparison is inside its own family. Three points of distinction:

- Versus the Corebridge Power Select Builder. The Power Select Builder runs a 10-year surrender schedule with a deeper, tiered crediting menu and a 9% S&P 500 cap. The Power 7 Protector currently carries a higher S&P cap (9.6%) on a shorter 7-year commitment, at the cost of a smaller index menu. Buyers who want maximum crediting depth and can commit 10 years should compare both; buyers who prize the shorter schedule have their answer already.

- Versus the Power 10 Protector. The Power 10 Protector is the same protector chassis stretched to a 10-year schedule. Same carrier, same design philosophy, longer commitment.

- Versus 7-year bonus FIAs. Contracts like the Athene Performance Elite 7 lead with premium bonuses and optional rider features, and typically cap the S&P 500 meaningfully lower. A shopper comparing this class of product should run matched illustrations side by side; in our experience the no-bonus, higher-cap product wins for most accumulation buyers.

How to Buy the Power 7 Protector

My Annuity Store places the Power 7 Protector through Corebridge’s independent distribution channel. We are licensed in 47 states and have placed more than $1 billion in annuity premium since 2020. To request a personalized illustration showing your specific premium, age, state, and chosen allocation, use our free annuity quote request form or call us directly at 855-277-8088.

The illustration referenced throughout this review (male, age 69, $100,000 non-qualified premium, Arizona, 50/50 allocation across the S&P 500 participation and S&P 500 cap accounts) was run July 20, 2026. Current crediting rates are subject to change. Your specific projected accumulation value will depend on premium, state of issue, allocation choices, and the carrier’s rate sheet in effect on your purchase date.

Frequently Asked Questions

Does the Corebridge Power 7 Protector have an income rider?

No. The Power 7 Protector is a pure accumulation FIA with no guaranteed living benefit rider available. Lifetime income is available only through no-cost annuitization. Corebridge offers the rider separately on the Power 7 Protector Plus Income, which trades lower crediting rates for the income guarantee.

What are the current rates on the Power 7 Protector?

As of July 2026, the headline rates are a 9.6% cap or 52% uncapped participation on the S&P 500 annual point-to-point accounts, and 4% on the one-year fixed account. Fourteen additional indexed strategies are available across the ML Strategic Balanced, AQR DynamiQ Allocation, and PIMCO Global Optima indices. All rates are subject to change on contract anniversaries.

Can I lose money in the Power 7 Protector?

Not from market performance on the no-fee accounts: when the index falls, those accounts credit 0% and your value holds. You can lose value three other ways: the 1.5% annual fee on the four Enhanced accounts applies even in zero-credit years, surrender charges of 8% down to 2% apply during the first 7 years, and a market value adjustment can reduce excess withdrawals during the surrender period.

What is the minimum guaranteed value?

The Minimum Withdrawal Value starts at 87.5% of premium (90% in New Jersey) and currently grows at 2.9% annually. On our $100,000 illustration it crosses above the original premium in year 5 and reaches $116,456 by year 10 even if the index accounts never credit a penny. The contract value itself simply stays at $100,000 in that all-zero scenario.

What is the difference between the Power 7 Protector and the Power 10 Protector?

The surrender period. The Power 7 Protector runs a 7-year schedule starting at 8%, while the Power 10 Protector stretches the same protector design to 10 years. Crediting rates differ between the two products and change over time, so compare current rate sheets for both before choosing. Read our full Power 10 Protector review for the long-schedule version.

Is the Power 7 Protector available in New York?

No. American General Life Insurance Company does not solicit, issue, or deliver contracts in New York, and the Power 7 Protector is also not available in Idaho, Guam, Puerto Rico, or the U.S. Virgin Islands. It is available in the other 45 states and Washington, D.C.

Want to model how a deposit grows year by year? Try our fixed annuity calculator.

Bottom Line Verdict

The Power 7 Protector is one of the cleaner accumulation FIAs we place: two genuinely competitive, fully transparent S&P 500 crediting options, a 4% fixed account, a short surrender schedule that ends at 2%, and no bonus or rider gimmicks, from a carrier rated A by AM Best. Its flaws are real but avoidable. Skip the 1.5%-fee Enhanced accounts and the weak proprietary-index options, and you are left with a contract we would comfortably shortlist for protected-growth money against any 7-year FIA in this rate environment.

Rating: 4 out of 5 stars – A disciplined, well-priced 7-year accumulation FIA with a top-tier S&P 500 cap; docked for the fee-account drag on the menu, the 87.5% early-surrender floor, and non-cumulative free withdrawals.

To request a personalized illustration based on your age, premium, and state, use our free annuity quote request or call 855-277-8088. The consultation and the illustration are free.