Is Allianz Benefit Control Annuity Good?

After completing my Allianz Benefit Control Annuity review, I don’t see a realistic client profile where Allianz Benefit Control (ABC) is the best annuity choice. Strong carrier, but this contract combines limited growth, high complexity, and underwhelming value. Below, I’ll quickly cover the features, what the illustration really shows, and where better options exist.

Based on the illustration and recent crediting history, its guaranteed values, surrender economics, and actual (not just hypothetical) performance don’t compete with simpler, higher‑yield alternatives or more transparent indexed designs.

While Allianz is a strong carrier, this specific contract asks the buyer to accept too little growth potential, too much complexity, and not enough value for the trade-offs. In short, I don’t see a client profile where this annuity would rise to the top of the shortlist. I’ll outline the features briefly and explain why.

Allianz Benefit Control at a Glance

| Detail | Information |

|---|---|

| Product Type | Fixed Index Annuity with Protected Income Value (PIV) rider |

| Issuing Carrier | Allianz Life Insurance Company of North America |

| AM Best / S&P / Comdex | A+ (Superior) / AA / 93 |

| Surrender Period | 10 years |

| Surrender Schedule | 9.3% / 9.3% / 8.3% / 7.3% / 6.25% / 5.25% / 4.2% / 3.15% / 2.1% / 1.05% |

| Minimum Premium | $20,000 |

| Income Base Bonus (PIV) | 25% on premium in the first 18 months |

| Current S&P 500 Cap | 4.00% (1-year point-to-point) |

| Allocation Charge | 0% current on most strategies; 0.95% on annual point-to-point indexed strategies; 2.5% maximum |

| Free Withdrawals | 10% of premium per year |

| Market Value Adjustment | Yes, on surrenders and excess withdrawals during the surrender period |

| Income Rider Fee | None (PIV rider bundled with the contract) |

Why Avoid the Allianz Benefit Control Annuity?

The Allianz ABC Annuity is very complicated, has low index caps and participation rates, and requires you to make a 10 year committment. Allianz has been a major player in the index annuity marketplace for the last 15 years, and they do have other indexed annuities in the product line-up far superior to this one.

Historical Rate of Return

When you buy a fixed index annuity, you do not know exactly what interest rate you will earn over the life of the annuity. This is because the interest is determined by the performance of a stock market index. You can get a hypothetical illustration that essentially applies today’s cap and participation rates to a backtest of the index over the last 10 years.

Below are the hypothetical returns for one of the index options, the Bloomberg Dynamic Index. You see, it would have returned an average of 3.84% over the last 10 years. I am sorry, but you can get a 5-year fixed annuity at 5.05% guaranteed from A+ rated Nationwide at the time of writing this article.

Morgan Stanley Strategic Trends Hypothetical Returns: Below are hypothetical returns for the Morgan Stanley Index option, which shows an annualized credited rate of 4.74% over the last 10 years.

Illustrated Crediting Rates and 10-Year Results

The live illustration we reviewed was run for a 74-year-old in Indiana with $100,000 split evenly across four strategies. Here are the current rates and what they produced:

| Strategy (25% each) | Current Rate | 10-Year Annualized (illustrated) |

|---|---|---|

| S&P 500 (1-yr point-to-point) | 4.00% cap | Capped at 4% in any up year |

| Morgan Stanley Strategic Trends 10 ER | 45% participation | 4.74% |

| Bloomberg US Dynamic Balance III ER | 75% participation | 3.84% |

| PIMCO Tactical Balanced ER | 70% participation | Contact agent for current rate |

| Blended portfolio (illustration) | n/a | 3.83% effective |

At a 3.83% blended effective rate, $100,000 grows to roughly $145,700 over 10 years. The single most telling number in the entire illustration is the 4.00% S&P 500 cap: even if the S&P 500 returns 25% in a year, this contract credits you 4%. As of this writing, an A+ rated MYGA pays around 5% guaranteed with no cap and no complexity. That is the core problem, and the chart below makes it visual.

How has Allianz ABC actually credited interest vs. the S&P 500?

The line graph below does not paint a pretty picture for the Allianz Benefit Control Annuity. As you can see, the S&P 500 (red line) earned about $140,000 over the last 10 years.The Allianz ABC Annuity earned about $24,000.This assumes an initial investment of $100,000.

Key Features:

Two Lifetime Income Rider Options

While the client is accumulating assets, the client can choose between two options for how to grow the contract’s “protected income value,” or PIV:

- The Accelerated PIV Rider

- The Control Balanced PIV Rider

Let’s take a look at the differences between the two income options:

1. Accelerated Protected Income Value rider

- 50% accumulation value interest factor.

- The annual payment amount will increase following any year there is fixed and/or indexed interest credited, and will receive the 250% interest bonus.

- The Protected Income Value (PIV) can receive two bonuses: a premium bonus on any premiums in the first 18 months and a bonus of any earned fixed and/or indexed interest for as long as they own the contract.

- Anytime after age 50, your client can access the Protected Income Value immediately or on any monthly anniversary by electing either single or joint lifetime withdrawals.

2. Balanced Protected Income Value rider

- The Protected Income Value (PIV) can receive two bonuses: a premium bonus on any premiums in the first 18 months and a bonus of any earned fixed and/or indexed interest for as long as they own the contract.

- Anytime after age 50, your client can access the Protected Income Value immediately or on any monthly anniversary by electing either single or joint lifetime withdrawals.

- The annual payment amount will increase following any year in which there is fixed and/or indexed interest credited, and will receive the 150% interest bonus.

The accelerated PIV option would be the best for someone is is certain they will be turning this annuity into a lifetime income stream while the balanced PIV option is best for someone who may not end-up using the annuity for lifetime income.

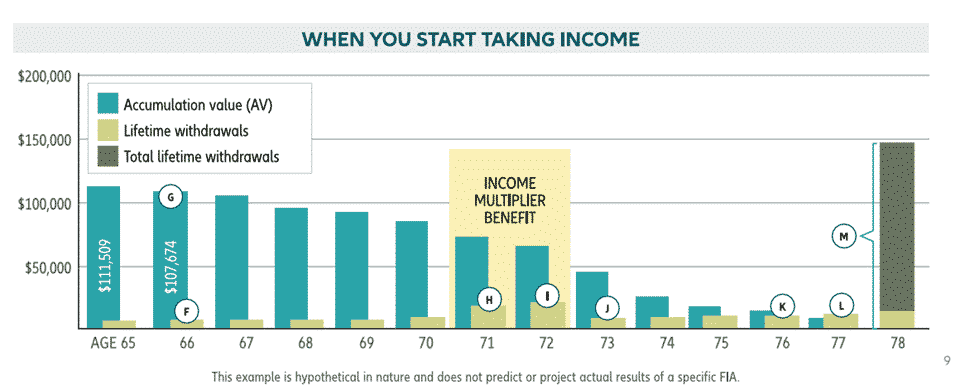

Allianz Income Multiplier (AIM) benefit.

The AIM benefit allows you to double your annual maximum lifetime income withdrawal if confined to a qualifying nursing home, hospital, or assisted living facility for at least 90 days in a consecutive 120-day period, or if you are unable to perform at least two of the six activities of daily living (ADLs).

Confinement must occur after the first contract year and either during the contract year before the start of lifetime income withdrawals or at any time thereafter.

Allianz Benefit Control Details

The Allianz Benefit Control Annuity+ is a fixed index annuity with a 10-year surrender charge period. Like all fixed index annuities, it’s designed to help you save money for retirement and provide a steady stream of income after you retire. But if you need to access your money sooner, you can take out a portion through free partial withdrawals – or even start lifetime withdrawals right away (must be at least 50 years old as of the most recent contract anniversary).

Income Flex Benefit (not illustrated)

The Income Flex Benefit is designed to give you more financial flexibility to adjust to unexpected expenses. Starting on the first contract anniversary after you begin lifetime withdrawals, you can choose to waive your income increase in any crediting period where you earn an interest credit, and instead set aside an additional withdrawal amount called the Income Flex Benefit Amount.

And, you have the option to take a withdrawal from that amount at any point in the year, which can aid you in effectively managing your finances during challenging times.

Blended Futures Index

The Blended Futures Index is comprised of four sub-indices: S&P 500 Futures Index ER, Bloomberg International Equity Custom Futures ER Index, Bloomberg US 10yr Note Custom Futures ER Index, and Bloomberg US Small Cap Custom Futures ER Index.

Index Lock

React to volatility by locking in a positive index value at any point during the crediting period. Index Lock can help assure you receive a positive index credit, no matter what happens in the market during the remainder of the crediting period.

Exercising an Index Lock may result in an interest credit higher or lower than had the lock not been exercised. Allianz will not provide advice or notification regarding whether to exercise an Index Lock or the optimal time for doing so.

MY (Multi-Year) Point-to-Point Crediting

MY (multi-year) point-to-point crediting methods may be a good choice for clients with a longer time horizon, while still offering short-term control with Index Lock. MY point-to-point crediting offers two options: a 2-year or 5-year crediting period. And whichever option your clients choose, the participation rates are guaranteed until the end of the crediting period.

But remember, you don’t have to wait until the end of the crediting period. If they see an index value they like, they can lock in that value with Index Lock.

Allocation Charge

Annual point-to-point, 2-year MY point-to-point, and 5-year MY point-to-point crediting methods are subject to an allocation charge, deducted annually from the contract accumulation value and guaranteed minimum value (in most states). The current allocation charge percentage is 0%.

After a contract issue, the allocation charge percentage can only change when specified criteria are met, and can never be greater than the maximum allocation charge percentage of 2.5%. The charge does not impact the contract Protected Income Value (PIV). Please refer to the official Allianz website for rates and illustrations.

Additional Premium

You may add more premium for the first 18 contract months in any amount between $25 and $25,000, unless we approve a larger amount. Additional premium is not allowed if you have taken a partial withdrawal or required minimum distribution (RMD) in the same contract year. Additional premium is not allowed once lifetime withdrawals or annuitization have begun.

Protected Income Value Premium Bonus

Anytime you put money into your contract in the first 18 months, you’ll get a premium bonus. We’ll credit this bonus to your Protected Income Value (PIV), giving you an immediate increase in the value of your lifetime withdrawals.

Increasing Lifetime Income Payments

Once you start receiving lifetime withdrawals from your Protected Income Value, there is an opportunity to increase your lifetime withdrawals based on the interest rate credited to your allocations, including the interest bonus.

After you’ve owned your annuity for at least five years, you can double your annual lifetime withdrawal amount with the Allianz Income Multiplier Benefit rider if you qualify due to hospitalization or confinement in an eligible nursing home or assisted living facility, or if you become unable to perform two of the six activities of daily living (ADLs).

Free Withdrawals:

In the contract year following the most recent premium payment, up to 10% of the contract’s premium paid, minus withdrawals, can be withdrawn each contract year without incurring withdrawal charges or market value adjustment, or penalties; the maximum is cash surrender value.

Surrender Charge Schedule

| Contract Year | Surrender Charge | Cost on $100,000 |

|---|---|---|

| Year 1 | 9.30% | $9,300 |

| Year 2 | 9.30% | $9,300 |

| Year 3 | 8.30% | $8,300 |

| Year 4 | 7.30% | $7,300 |

| Year 5 | 6.25% | $6,250 |

| Year 6 | 5.25% | $5,250 |

| Year 7 | 4.20% | $4,200 |

| Year 8 | 3.15% | $3,150 |

| Year 9 | 2.10% | $2,100 |

| Year 10 | 1.05% | $1,050 |

| Year 11+ | 0% | $0 |

A Market Value Adjustment also applies to surrenders and excess withdrawals during the surrender period, which can increase or decrease these amounts depending on how interest rates have moved since issue.

Death Benefit

Before annuitization, the Allianz Benefit Control Annuity gives you two death benefit options. Your beneficiary can receive the greater of the accumulation value, guaranteed minimum value, or cumulative withdrawal amount as a lump sum (this option doesn’t include any premium or interest bonuses).

Or, they can receive the Protected Income Value – including the premium and interest bonuses – in payments over a minimum of five years, limited to 250% of the accumulation value (PIV death benefit limit can vary by state).

Available Indexes and Crediting Methods

| Index | Crediting Method(s) | Current Rate |

|---|---|---|

| S&P 500 | 1-Year Point-to-Point with Cap | 4.00% cap |

| Nasdaq-100 | 1-Year Point-to-Point | Contact agent |

| Russell 2000 | 1-Year Point-to-Point | Contact agent |

| Morgan Stanley Strategic Trends 10 ER | 1-Year PTP Participation | 45% par |

| Bloomberg US Dynamic Balance III ER | 1-Year PTP Participation | 75% par |

| PIMCO Tactical Balanced ER | 1-Year PTP Participation | 70% par |

| Blended Futures Index | 1-Year, 2-Year, or 5-Year MY Point-to-Point | Contact agent |

Amounts allocated to annual point-to-point and 2-year point-to-point crediting methods are subject to an allocation charge that is deducted annually from the accumulation value and guaranteed minimum value.

The current allocation charge percentage is 0.95%. If you are not very familiar with how the above strategies work, you will likely benefit from reading Index Annuity Crediting Methods Explained.

Want to compare current fixed index annuity rates? See our regularly updated fixed index annuity cap and participation rates to benchmark this product against the market.

What We Like and What Gives Us Pause

What We Like

- There is a lot of flexibility built into the contract,t with the ability to select between 2 income rider options.

- The Index Lock feature allows you to lock in your interest mid-year

- The Income Multiplier Benefit doubles your income should you be confined to a facility or require in-home health care (based on restrictions)

- Lots of available indexes and crediting methods

- Increasing Income Potential even after the lifetime income feature has been turned on

What Gives Us Pause

- The 4 different riders can make this product confusing

- It has the potential for multiple fees

- The cap, spread, and participation rates are not very competitive

- The Accelerated income rider only credits your account value 50% of the total interest earned, and with the fees, it would be almost impossible to even break even, in my opinion.

- If you choose the Balanced income rider option, the income feature is watered down and not as good as the benefits found elsewhere.

Bottom Line Verdict

To complete this Allianz Benefit Control Annuity review, I spent over an hour running different hypothetical reports using the available index options and crediting methods. The reasonable expected rate of return is under 4% in almost every scenario I tested, and the guaranteed lifetime income amount is not in the top 10 in almost every scenario.

If you want guaranteed lifetime income, there are far better options, and if you want a safe accumulation vehicle, you’d be far better off with a fixed annuity guaranteed 5%. If a financial advisor recommends this annuity to you, I would ask them what made them select it over other options, such as Nationwide Peak 10 FIA or Athene’s Performance Elite 7.

If you would like a second opinion or have questions about the Allianz ABC Annuity (or any indexed annuity), a My Annuity Store expert is available at 855-583-1104.

Rating: 2.5 out of 5 stars – A strong, highly rated carrier wrapped around an uncompetitive contract: a 4% S&P 500 cap and a roughly 3.8% blended illustrated return that a simpler MYGA beats, layered with rider complexity and a 10-year commitment.

Next Steps:

- Compare to today’s best fixed annuity rates

- Use our lifetime income rider quoting tool to see the top 10 index annuity payouts

- Request a personalized annuity rates report

FAQs: Allianz Benefit Control Annuity

Is Allianz Benefit Control (ABC) a good annuity?

It’s a credible product from a strong insurer, but based on recent illustrations and guaranteed values, ABC rarely offers the best combination of growth potential, simplicity, and liquidity compared to alternatives like MYGAs or cleaner FIAs.

What are the main trade‑offs with ABC?

Complex crediting, modest caps/participation, and rider mechanics that add moving parts. You’re trading simplicity and competitive yield for a bundle of features that often underdeliver versus straightforward options.

How has ABC credited interest versus the S&P 500?

Illustrations show ABC credits lagging far behind the index due to caps, spreads, and volatility‑controlled designs. The gap is expected–FIAs don’t own equities–and ABC’s configuration amplifies that drag.

What do the guaranteed values and cash surrender values tell me?

They highlight limited downside but also limited upside and constrained access. If guaranteed value and liquidity are your priority, a MYGA or higher free‑withdrawal structure is usually cleaner.

Who, if anyone, should consider ABC?

Possibly someone who prioritizes a specific rider feature and accepts lower growth and extra complexity. For most buyers seeking yield, simple guarantees, or transparent indexing, better fits exist.

What alternatives usually beat ABC?

Multi‑Year Guaranteed Annuities (MYGAs) for fixed, high, simple yields; and select FIAs with competitive caps/participation and fewer moving parts. Product selection depends on age, state, horizon, and liquidity needs.

Are there big fees or surrender charges?

Like most deferred annuities, ABC includes surrender charges during the term and possible rider costs. Liquidity is typically limited to penalty‑free withdrawals; read the schedule before buying.