What is a MYGA?

A multi-year guaranteed annuity (MYGA) is one of the safest, most predictable ways to grow retirement savings tax-deferred. You deposit a lump sum with an insurance company. They lock in a guaranteed interest rate for a set term, typically 3, 5, 7, or 10 years, and your money grows without any market risk whatsoever.

In 2026, top MYGA rates from top-rated carriers are running 5.00%-5.75%, depending on term length and deposit amount. If you have money sitting in a bank CD earning 3.5%-4%, the math strongly favors a MYGA.

What Is a MYGA?

A multi-year guaranteed annuity (MYGA) is a fixed annuity contract that locks in a single guaranteed interest rate for a set term, typically 3, 5, 7, or 10 years, with zero exposure to market losses. You hand a lump sum to an insurance company. The insurance company contractually guarantees the rate and the principal for the full term.

Think of a MYGA as the insurance industry’s answer to a bank CD, with three differences that matter for retirees: the rate is usually higher, the interest grows tax-deferred, and the contract is backed by an insurance company plus the state guaranty association rather than the FDIC.

MYGAs are not investments; they are insurance contracts. Your return is not tied to the stock market, bond market, or any index. You get exactly what the contract guarantees.

What Does MYGA Stand For?

MYGA stands for Multi-Year Guaranteed Annuity. The “multi-year” part is the defining feature: unlike a traditional fixed annuity that may guarantee a rate for only the first year and reset annually after that, a MYGA guarantees a single rate for the entire term you select.

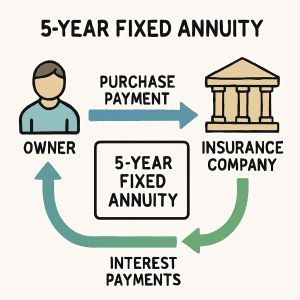

How Does a MYGA Work?

A MYGA works in three simple steps: you deposit a lump sum, the insurance company guarantees a fixed interest rate for the full term, and your money grows tax-deferred until you withdraw it.

Here is what a 5-year MYGA actually looks like in practice. Mary, age 62, has $200,000 in a maturing CD earning 3.75%. She moves it into a 5-year MYGA paying 5.50%.

| Year | Starting Balance | Interest @ 5.50% | Ending Balance |

|---|---|---|---|

| 1 | $200,000 | $11,000 | $211,000 |

| 2 | $211,000 | $11,605 | $222,605 |

| 3 | $222,605 | $12,243 | $234,848 |

| 4 | $234,848 | $12,917 | $247,765 |

| 5 | $247,765 | $13,627 | $261,392 |

Mary’s $200,000 grows to $261,392 over 5 years, a guaranteed gain of $61,392. She pays no taxes on the interest until she withdraws it. Open the MYGA calculator to run your own numbers.

Are MYGAs Safe?

MYGAs are among the safest places to put retirement money. Your principal cannot decline because of market activity. The insurance company is contractually obligated to honor your rate for the full term, and three layers of protection sit behind that promise.

Layer 1: Insurance company reserves. Insurance carriers are required by state law to hold reserves backing every annuity contract they issue. Most top-rated carriers maintain reserve ratios well above legal minimums. Use AM Best, Moody’s, S&P, and Comdex scores to evaluate carrier strength before buying.

Layer 2: State guaranty associations. If an insurance company becomes insolvent, the state guaranty association in your state covers annuity contracts up to a stated limit, most commonly $250,000 in present-value benefits per owner per insurer.

Layer 3: Diversification across carriers. If you have more than the guaranty limit to invest, you can split it across two or three different top-rated carriers and get full coverage on each contract.

MYGAs are not FDIC-insured. They are insurance products, not bank deposits. But in 35+ years of state guaranty association history, no annuity owner who stayed within coverage limits has ever lost principal due to insurer insolvency.

MYGA Rates in 2026

In 2026, the best MYGA rates from top-rated carriers range from 5.00% to 5.75%, with 5-year contracts typically paying the highest yields. Rates change daily as carriers reprice in response to Treasury yields and reserve requirements.

Here is how MYGA rates typically stack up by term in 2026:

- 3-Year MYGA: 4.85%-5.40%

- 5-Year MYGA: 5.10%-5.75% (often the sweet spot)

- 7-Year MYGA: 5.20%-5.65%

- 10-Year MYGA: 5.10%-5.50%

For the most current rates from 90+ top annuity companies, see our live tables:

- Best 3-Year MYGA Rates

- Best 5-Year MYGA Rates

- Best 7-Year MYGA Rates

- Best 10-Year MYGA Rates

- Compare All MYGA Rates

| Annuity | Carrier | Rate | AM Best | Term |

|---|---|---|---|---|

| Anchor MYGA 5 | American Gulf | 6.00% | B++ | 5 yr |

| Anchor MYGA 6 | American Gulf | 6.00% | B++ | 6 yr |

| Safe Haven 10 | Atlantic Coast Life | 5.80% | B | 10 yr |

| Waypoint 5 MYGA | Axonic Insurance | 5.80% | A- | 5 yr |

| IQumulate 5 | Baltimore Life Insurance Company | 5.80% | B++ | 5 yr |

| IQumulate 7 | Baltimore Life Insurance Company | 5.80% | B++ | 7 yr |

Rates updated daily · Source: AnnuityRateWatch · Not a solicitation · Rates vary by state

Best MYGAs of 2026: Editor’s Picks

The “best” MYGA depends on what matters most to you: highest rate, strongest carrier, most flexible withdrawals, lowest minimum, or specialty features like return of premium. We track the full marketplace of 90+ top annuity companies and evaluate every product on rate, AM Best rating, surrender schedule, free withdrawal allowance, and contract flexibility.

These are our editor’s picks across the categories that matter most to retirees.

For full carrier ratings and product lineups, browse the complete list of 90+ top annuity companies or our annuity reviews database.

Here's your estimated lifetime monthly income.

Live income rider quotes for your scenario.

Top 3 MYGA rates available right now.

Two top fixed-index annuities to compare.

MYGA vs. CD: Which Pays More?

MYGAs typically pay 1-2 percentage points more than equivalent-term CDs and offer tax-deferred growth, while CDs are FDIC-insured and CD interest is taxed annually. For non-IRA money, the tax deferral advantage often makes MYGAs the clear winner.

| Feature | MYGA | Bank CD |

|---|---|---|

| Typical 5-Year Rate (2026) | 5.10%-5.75% | 3.75%-4.50% |

| Tax Treatment (Non-Qualified) | Tax-deferred | Taxed annually |

| Insurance/Backing | State guaranty association (typically $250k) | FDIC ($250k per depositor) |

| Free Withdrawals | Typically 10% per year | None (early withdrawal penalty) |

| Minimum Deposit | Often $5k-$25k | As low as $500 |

| Penalty for Early Withdrawal | Surrender charge (declines yearly) | Forfeit several months of interest |

For a deeper dive, see our full side-by-side breakdown of fixed annuities vs. CDs and run the numbers in our Fixed Annuity vs. CD Calculator.

MYGA vs. Treasury Bonds and High-Yield Savings

MYGAs typically out-yield Treasury notes and high-yield savings accounts of similar duration, while Treasuries offer state-tax-free interest and unmatched liquidity, and high-yield savings offers full liquidity. The right choice depends on your tax situation and how soon you need the money.

| Feature | MYGA (5-yr) | 5-Year Treasury | High-Yield Savings |

|---|---|---|---|

| Typical 2026 Yield | 5.10%-5.75% | 4.20%-4.60% | 3.75%-4.50% |

| Federal Tax | Tax-deferred until withdrawal | Taxed annually | Taxed annually |

| State Tax | Taxed at withdrawal | Exempt | Taxed annually |

| Liquidity | 10% free / year | Sell anytime (price varies) | Full liquidity |

| Rate Lock | Yes, full term | Yes, if held to maturity | No, variable |

If you live in a high-tax state and the money sits in a non-qualified account, Treasury bonds may close the gap. If you need full liquidity, high-yield savings is the answer. For everything in between, MYGAs usually win on after-tax math.

MYGA vs. Fixed Annuity: What’s the Difference?

A MYGA is a type of fixed annuity that locks in one guaranteed rate for the full term, while a traditional fixed annuity often guarantees a rate only for the first year and resets annually after that. Every MYGA is a fixed annuity, but not every fixed annuity is a MYGA.

The practical difference: with a MYGA you know your rate for the entire term on day one. With a non-MYGA fixed annuity, your rate after year one depends on what the carrier decides to credit, subject only to a contractual minimum. For predictability, MYGA wins. For potentially higher renewal rates if interest rates rise, a non-MYGA fixed annuity can sometimes pay more, though most do not.

For most retirees who want certainty, MYGA is the right answer. See our complete fixed annuity guide for the full breakdown.

Who Should Buy a MYGA?

MYGAs are best for retirees and pre-retirees aged 55-75 who want guaranteed growth, principal protection, and tax-deferred compounding on money they don’t need for at least 3-10 years.

You are probably a good fit for a MYGA if any of these describe you:

- You have $50,000 or more sitting in CDs, money market, or savings earning less than 4%.

- You want predictable growth without market risk for the next 3-10 years.

- You are 5-10 years from retirement and want to lock in a guaranteed rate before the next rate cycle.

- You want tax-deferred growth on non-qualified money outside of an IRA or 401(k).

- You have IRA money you want to move out of the stock market into something with a guaranteed rate.

You are probably not a good fit for a MYGA if:

- You need full liquidity (use high-yield savings instead).

- You are under age 50 and want long-term equity-like growth.

- You will need the principal in less than 3 years.

How MYGAs Are Taxed

MYGA earnings grow tax-deferred and are taxed as ordinary income only when withdrawn. If the MYGA is held outside an IRA, withdrawals before age 59½ may incur a 10% IRS penalty on the gain in addition to ordinary income tax.

Two scenarios cover most MYGA buyers:

Non-qualified (after-tax) money. Your principal is already taxed, so only the interest is taxable on withdrawal. Tax deferral compounds your growth for the full term. At withdrawal, gains are treated as ordinary income, not capital gains.

Qualified (IRA / 401(k)) money. Both principal and earnings are pre-tax. The full withdrawal is taxed as ordinary income. There is no additional layer of tax deferral because IRAs are already tax-deferred, but the rate guarantee and principal protection still apply.

At maturity, you can take the cash (taxable on the gain), roll into a new MYGA, do a tax-free 1035 exchange into a different annuity, or annuitize for guaranteed income.

Surrender Charges and Free Withdrawal Rules

MYGA surrender charges typically start at 8-9% in year one and decline 1% per year until they reach zero at the end of the contract term. Most MYGAs allow a free annual withdrawal of 10% of the contract value with no surrender charge.

A typical 7-year MYGA surrender charge schedule looks like this:

| Year | Surrender Charge |

|---|---|

| 1 | 8% |

| 2 | 7% |

| 3 | 6% |

| 4 | 5% |

| 5 | 4% |

| 6 | 3% |

| 7 | 0% |

The surrender charge applies only to amounts withdrawn above the free withdrawal allowance during the surrender period. After the surrender period ends, you can withdraw any amount with no charge. Read the full breakdown of how annuity surrender charges work.

Surrender Charge Comparison Table

Surrender charge schedules vary widely between MYGA carriers. Some use the typical 8-7-6-5-4-3-0 declining pattern. Others front-load with steeper early charges and lower late-year charges. A few specialty carriers use a flat 5% schedule that doesn’t decline. Free withdrawal allowances also differ – most carriers offer 10% per year, some only allow interest-only withdrawals, and a few permit no free withdrawals at all.

When comparing two MYGAs with similar rates, the surrender schedule and free withdrawal terms can swing the after-tax return on a 5-year hold by 1-2% or more if you ever need to access the money early.

For side-by-side surrender schedules across the full marketplace, browse the live MYGA rate table (each product page lists the surrender schedule) or contact our team for a customized comparison based on your liquidity needs.

MYGA Laddering Strategy

A MYGA ladder is the strategy of splitting a lump sum across multiple MYGAs with staggered terms (typically 3, 5, and 7 years) so that one contract matures every few years. This gives you regular access to a portion of your principal without surrender charges and the flexibility to reinvest at prevailing rates as each contract matures.

Here is what a $300,000 MYGA ladder might look like:

| Bucket | Amount | Term | Rate | Matures |

|---|---|---|---|---|

| Short | $100,000 | 3 years | 5.20% | 2029 |

| Mid | $100,000 | 5 years | 5.60% | 2031 |

| Long | $100,000 | 7 years | 5.50% | 2033 |

Every two years a contract matures, giving you the option to take cash, reinvest into a new long-term contract at current rates, or move the money to a different vehicle. Laddering is the standard playbook for retirees who want predictable growth plus periodic flexibility. See our full annuity laddering guide.

Market Value Adjustment (MVA) and Return of Premium (ROP)

Two MYGA features confuse buyers more than any others: market value adjustment and return of premium. Both change how the contract behaves if you exit early, so look closely before you sign.

Market Value Adjustment (MVA). An MVA is a feature that adjusts your surrender value up or down based on how interest rates have moved since you bought the contract. If rates have risen since issue, an MVA reduces your surrender value. If rates have fallen, an MVA can increase it. MVA-equipped MYGAs typically pay slightly higher base rates because the carrier is sharing some interest-rate risk with you. If you intend to hold to maturity, MVA is a non-issue.

Return of Premium (ROP). Return of premium is a contractual guarantee that you can never receive less than your original deposit at any point in the contract, even if you surrender early during the surrender period. ROP is a powerful feature for risk-averse buyers but typically comes with a slightly lower base rate.

Not every MYGA includes an MVA, and not every MYGA includes ROP. Read the contract carefully or work with a licensed agent who will translate the language for you.

How to Choose a MYGA Term Length

The right MYGA term length depends on three things: when you’ll need the money, your view on where interest rates are heading, and how much liquidity flexibility you want during the contract.

A simple decision framework:

- Need the money in 3-4 years? A 3-year MYGA. Lower rate, but you’re back in cash before life changes.

- 5-7 year horizon and you think rates have peaked? A 5- or 7-year MYGA. Lock in today’s rate before they decline. This is the most common choice for retirees in 2026.

- 10+ year horizon (often IRA money)? A 10-year MYGA. Maximum rate lock, ideal for money you won’t touch.

- Want the flexibility of multiple maturity dates? A 3-5-7 ladder. Sacrifice a small amount of yield for predictable access to portions of principal.

Inflation is the often-overlooked factor. If you expect inflation to run hot for the next decade, a longer-term MYGA at today’s rate may underperform. If you expect inflation to remain near 2-3%, today’s 5-5.75% MYGA rates produce solid real returns.

How to Buy a MYGA: Step-by-Step

Buying a MYGA is a straightforward five-step process that typically takes 7-14 business days from quote to issued contract.

- Compare current rates and carriers. Use our live MYGA rate table to see what’s available today across 90+ top annuity companies. Filter by term, AM Best rating, and minimum premium.

- Pick a contract that fits your goals. Match the term to when you’ll need the money. Confirm the surrender schedule, free withdrawal allowance, and any MVA or ROP features.

- Submit an application. Most MYGAs require basic personal information, beneficiary designations, and an indication of premium source (cash, IRA, 1035 exchange).

- Fund the contract. Wire funds, mail a check, or initiate a custodian-to-custodian transfer for IRA or 1035 money. The clock on your guaranteed rate typically starts the day funds are received in good order.

- Receive your contract and review. Most carriers send the contract within 7-14 business days. Most states give you a “free look” period (typically 10-30 days) during which you can return the contract for a full refund if you change your mind.

For a deeper how-to walkthrough, see How to Buy an Annuity (Without Getting Ripped Off) or book a free 15-minute call with our team.

How to Buy a MYGA with an IRA Rollover

You can fund a MYGA with Traditional IRA, Roth IRA, SEP IRA, or 401(k) rollover money using a direct trustee-to-trustee transfer, with no taxes owed at the time of rollover. The MYGA simply becomes the new vehicle holding your IRA dollars.

The four-step IRA rollover process:

- Choose a qualified MYGA. Confirm the carrier accepts IRA money (almost all do) and that the contract is set up as an IRA, Roth IRA, or 401(k) rollover at issue.

- Complete a rollover/transfer form. Your new carrier sends a transfer request to your existing IRA custodian (Schwab, Fidelity, Vanguard, Edward Jones, etc.). You sign once.

- Funds move directly between custodians. The money never touches your hands. Because it’s a direct transfer (not a 60-day rollover), there is no withholding and no reportable distribution.

- The MYGA contract is issued in your IRA’s name. Required minimum distributions (RMDs) for Traditional IRAs continue as normal at age 73, and the MYGA can satisfy them either through partial withdrawals or by annuitizing a portion of the contract.

One nuance: Roth IRA MYGAs grow tax-free, not just tax-deferred. If you’re rolling Roth money, the tax deferral the MYGA provides is duplicative, but the rate guarantee and principal protection still make sense for the right buyer.

Frequently Asked Questions About MYGAs

What is the minimum investment for a MYGA?

Can I lose money in a MYGA?

Are MYGAs FDIC insured?

What happens when my MYGA term ends?

How is a MYGA different from a fixed index annuity?

Can I use IRA money to buy a MYGA?

Are MYGAs safe?

How are MYGA rates set?

What is a MYGA ladder?

Can I withdraw from a MYGA before the term ends?

Sources and Citations

- U.S. Securities and Exchange Commission. Investor Bulletin: Annuities.

- FINRA. Annuities Investor Education.

- Internal Revenue Service. Publication 575: Pension and Annuity Income.

- National Association of Insurance Commissioners. Buyer’s Guide for Deferred Annuities (Fixed).

- National Organization of Life and Health Insurance Guaranty Associations. Policyholder Information and State Guaranty Association Coverage.

Get a Free Quote

Want a custom MYGA recommendation tailored to your goals, tax situation, and timeline? Our team compares 90+ top annuity companies and gives you a free, no-pressure quote.

Still have questions? See our complete annuity FAQ with 45 answers covering rates, taxes, surrender charges, RMDs, ladders, 1035 exchanges, and more.

Cost note: Wondering about price? See our full breakdown on how much a fixed annuity costs in 2026, MYGAs have zero annual fees.