When is the Best Time to Take Social Security?

Understanding social security optimization can help you make informed decisions about your claiming age.

Social Security isn’t just a monthly check–it’s an asset. Optimizing your claim date can add six figures to your lifetime household income. Social Security is the backbone of most retirement income plans–and your claiming age can change your lifetime benefits by six figures. This guide will help decide when to claim, how to coordinate with your spouse, and how to integrate Social Security with your retirement paycheck and taxes.

The Claiming Decision Framework

Choosing when to claim drives lifetime benefits and survivor outcomes. Consider health and longevity, your earnings record, spousal status, other guaranteed income, and your tax picture. Use breakeven analysis to compare claiming at 62, your FRA, or age 70.

Coordinate with your broader retirement paycheck so your monthly income is stable while you pursue the highest lifetime value. Effective social security optimization considers various factors including health, earnings, and spousal benefits.

Key Inputs:

- Health and longevity: If your family’s longevity is strong and your health is good, delaying often increases lifetime benefits.

- Earnings record: Higher earners get more leverage from delaying; check your earnings history for missing years.

- Spousal status: Couples should coordinate to maximize survivor benefits; see Strategies for Couples.

- Other income: Pensions, annuities, or portfolio withdrawals can bridge cash flow while delaying the increase in Social Security.

- Taxes: Social Security interacts with provisional income; plan withdrawals to minimize taxation.

“Not sure how long to plan for? Use the SSA Life Expectancy Calculator to see the statistical average for your age.”

The Breakeven Concept

Engaging in social security optimization helps clarify the pros and cons when determining your claiming age. Breakeven analysis compares the total benefits received when claiming early versus waiting.

For many retirees, the breakeven between claiming at 62 and 70 lands in the late 70s to early 80s. If you expect to live beyond that horizon–or if you’re protecting a spouse–delaying can make sense.

Social Security Optimization

Claiming Ages: 62 vs FRA vs 70

Pros and cons of each age

When considering your claiming age, remember that social security optimization strategies can significantly affect your lifetime income.

Claim at 62

- Pros: Immediate income; helpful if retiring early or with limited savings.

- Cons: Permanently reduced benefit; reduced survivor benefit for your spouse

Claim at Full Retirement Age (FRA)

- Pros: Full benefit; earnings test ends after FRA; balanced approach.

- Cons: Lower lifetime total than delaying to 70 for long-lived households.

Verify your exact Full Retirement Age based on your birth year at the official SSA planner. Your approach to social security optimization can affect the financial outcomes for you and your spouse.

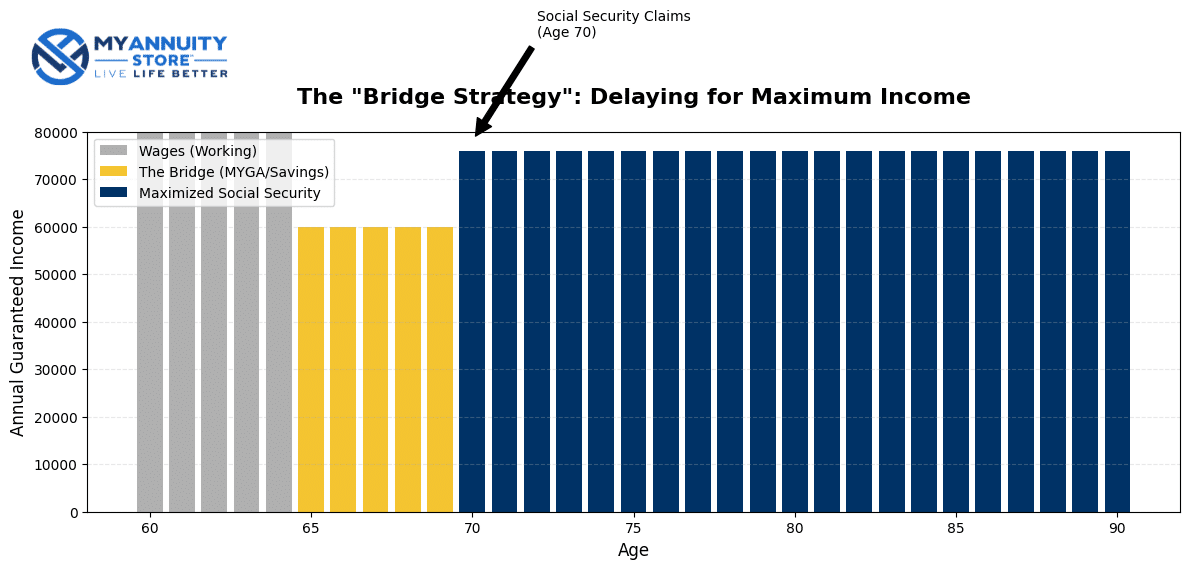

Delay to Age 70

- Pros: Highest monthly benefit via delayed retirement credits; strengthens survivor benefits.

- Cons: Requires a bridge strategy until 70; more tax planning considerations.

Impact on survivor benefits

Understanding how social security optimization impacts survivor benefits is key to planning for your family’s future.

The higher earner’s claiming decision typically sets the floor for survivor income. Delaying the higher earner’s benefit to 70 can materially improve the surviving spouse’s financial security.

- Learn more: Special Situations (widowed/divorced scenarios)

Strategies for Couples and Divorce/Widowhood

Social security optimization strategies can be adjusted based on your unique financial situation.

Couples can coordinate spousal and survivor benefits to maximize household income. Often, the higher earner delays until age 70 to boost survivor benefits while the lower earner claims earlier to provide near-term cash flow.

Divorced individuals (married 10+ years, currently unmarried) may qualify for divorced spousal or survivor benefits. Widows and widowers can sequence survivor and retirement benefits for optimal outcomes.

Note: Restricted Application strategies are largely phased out for those born after Jan 1, 1954.

Coordinating spousal benefits

- Common approach: Lower earner claims earlier; higher earner delays to 70.

- Survivor focus: Prioritize the higher earner’s delay to protect the survivor benefit.

- Integration: Use annuity or portfolio bridges to cover the gap while delaying.

Careful social security optimization requires an understanding of both your needs and your partner’s needs.

Survivor benefits optimization

- If you are the higher earner, delaying typically increases the survivor benefit your spouse may receive.

- Consider life insurance or an income annuity as a contingency if delaying isn’t feasible.

Divorced benefits (10-year rule)

- If you were married at least 10 years and are currently unmarried, you may qualify for divorced spousal or survivor benefits based on your ex’s record.

- Timing and remarriage rules matter; model scenarios before filing.

Taxes on Social Security

Taxes can reduce your take-home benefit depending on your provisional income. Smart withdrawal sequencing and well-timed Roth conversions can lower lifetime taxes and reduce the percentage of your Social Security subject to tax.

Provisional income and thresholds

Understanding provisional income is part of effective social security optimization.

- Provisional income includes half of your Social Security, plus taxable interest, ordinary income, and some tax-exempt interest.

- As provisional income rises, up to 50%–85% of Social Security benefits may become taxable.

- Use our calculator to see your exposure: Social Security Taxable Benefits Calculator

Mitigating taxation with withdrawal order and Roth conversions

- Withdrawal order: Typically spend taxable accounts first, then traditional IRA/401(k), and reserve Roth for later–but personalize based on brackets and RMDs.

- Roth conversions: Converting in low-income years (often early retirement) can reduce future RMDs and lower Social Security taxation later.

- Defer SS, fill brackets: Bridging income from MYGAs, SPIAs/DIA, or portfolio withdrawals can help you convert efficiently before claiming.

- Learn more: Tax-Efficient Withdrawals

Integrating Social Security with Your Paycheck

Your Social Security decision should fit into a broader “retirement paycheck” that blends guaranteed income, withdrawals, and liquidity. If you delay to increase your benefit, build a bridge with predictable cash flows.

Bridging strategy if delaying to 70 (MYGA or portfolio withdrawals)

- MYGA ladder: Stagger maturities (e.g., 3/5/7 years) to cover living expenses while you delay.

- Structured withdrawals: Use taxable accounts first to keep provisional income lower later.

- Links: | MYGA Rates | Annuity Ladder Calculator

SPIA/DIA timing with SS claiming

- SPIA now, SS later: Lock in immediate income to relieve sequence risk while investments ride out volatility.

- DIA for later-life: Turn on income in the 70s+ to pair with SS and reduce longevity risk.

- Links: SPIA explainer | Immediate Annuity Quotes

Advanced Situations

Some cases need extra coordination due to public pensions, high income, or Medicare-related costs. Advanced situations require careful social security optimization planning to avoid pitfalls.

Public pensions and WEP/GPO overview

- Windfall Elimination Provision (WEP): May reduce your worker benefit if you have a pension from non-covered employment.

- Government Pension Offset (GPO): May reduce spousal/survivor benefits for those with certain public pensions.

- Model these rules alongside your claiming age before filing.

High earners and IRMAA considerations

High earners should pay attention to social security optimization to manage IRMAA considerations.

- Higher income can trigger Medicare’s IRMAA surcharges.

- Coordinated Roth conversions, timing of RMDs, and charitable strategies (QCDs) can help manage MAGI and IRMAA.

- Learn more: Tax-Efficient Withdrawals

Tools and Calculators

Utilize tools and calculators that emphasize social security optimization in your retirement planning.

- Plan with Journey Guide: Model your claiming age, bridge strategy, and tax outcomes together.

- Social Security Taxable Benefits Calculator: Estimate how much of your Social Security will be taxed.

- Social Security Savvy Playbook (26 pages)

- Social Security Administration Website

FAQs

- Is it worth delaying Social Security to age 70?

- Delaying increases your monthly benefit and often maximizes lifetime income and survivor benefits for long-lived households.

- How do taxes affect Social Security benefits?

- Benefits can be taxed based on provisional income. Coordinating withdrawals and Roth conversions can reduce the percentage taxed.

- Can divorced spouses claim Social Security benefits?

- Yes. If you were married at least 10 years, are currently unmarried, and meet age and eligibility rules, divorced spousal or survivor benefits may apply.

- What’s the best way for couples to coordinate claiming?

- A common strategy is for the higher earner to delay until age 70 to boost survivor benefits while the lower earner claims earlier to provide cash flow.

- How can I bridge the income if I delay until 70?

- Consider a MYGA ladder, a SPIA, or systematic withdrawals from taxable accounts to fund expenses while you delay.

- Does working in retirement reduce my benefits?

- Before FRA, the earnings test can withhold benefits if you exceed annual limits (withheld amounts may increase later benefits). After FRA, there’s no earnings test.

Next Steps

Important Disclosures Regarding Social Security & Financial Planning

Not a Government Agency: My Annuity Store and its representatives are not affiliated with, endorsed by, or employed by the Social Security Administration (SSA) or any federal government agency. The information provided here is for educational purposes only and should not be considered official government guidance.

Not Legal or Tax Advice: We are not attorneys or tax professionals. Any discussion regarding tax implications or estate planning is general in nature. You should consult with a qualified tax advisor or legal counsel regarding your specific situation before making any claiming decisions.

Accuracy of Information: Social Security rules, benefit amounts, and tax thresholds are subject to change by the federal government. While we strive to keep this information current, we make no warranties regarding the accuracy or completeness of the data presented. Always verify your specific benefit details directly with the Social Security Administration at SSA.gov or by visiting your local SSA office.

Solicitation of Insurance: This content is part of a retirement planning service that may involve the solicitation of insurance products, including fixed and fixed-indexed annuities.