🏆 Annuity Awareness Challenge

Test your knowledge of annuities, contract features, and regulations

Annuity Awareness Challenge: Complete Answer Guide

Understanding the complexities of annuities through detailed explanations

Congratulations on completing the Annuity Awareness Challenge! Whether you aced the quiz or discovered areas for improvement, this detailed guide will deepen your understanding of annuities and their key features. Let’s dive into each question and explore not just the correct answers, but also what the other options represent in the world of annuities.

Question 1: Guaranteed Payment Annuities

Question: Which type of annuity provides guaranteed payments for a specific period or lifetime, regardless of market performance?

Correct Answer: Fixed Annuity

Deep Dive Explanation

Fixed annuities are the cornerstone of guaranteed income in retirement. When you purchase a fixed annuity, the insurance company promises to pay you a predetermined amount, typically expressed as an interest rate, regardless of how the broader financial markets perform. This guarantee is backed by the insurance company’s general account and its financial strength.

Here’s what makes fixed annuities unique:

- Predictable returns: You know exactly what rate you’ll earn during the accumulation phase

- Guaranteed income: During the payout phase, your monthly payments are fixed and guaranteed principal protection: Your initial investment is protected from market downturns

- Conservative growth: While returns are typically lower than market-based options, they’re stable

Understanding the Other Options

Variable Annuity: These products tie your returns directly to underlying investment options (sub-accounts). Your account value and future income payments will fluctuate based on market performance. While they offer growth potential, they provide no guarantees against market losses.

Indexed Annuity (Fixed Indexed Annuity): These hybrid products offer a middle ground, providing principal protection while allowing participation in market gains through links to market indices like the S&P 500. However, the “guarantee” aspect is limited to principal protection, not guaranteed growth rates.

Immediate Annuity: This refers to the timing of when payments begin (immediately after purchase) rather than the guarantee structure. Immediate annuities can be fixed, variable, or indexed, so this option doesn’t specifically address the “guaranteed payments regardless of market performance” aspect of the question.

Question 2: Market Participation with Downside Protection

Question: Sarah wants an annuity that allows her to participate in market gains but protects her from market losses. Which type should she consider?

Correct Answer: Fixed Indexed Annuity

Deep Dive Explanation

Fixed Indexed Annuities (FIAs) represent one of the most innovative developments in the annuity world, designed specifically for people like Sarah who want growth potential without downside risk. These products accomplish this through several key mechanisms:

How Market Participation Works:

- Your account value is linked to the performance of market indices (S&P 500, NASDAQ, etc.)

- When the index performs well, you receive credited interest based on that performance

- Participation rates and caps may limit how much of the index gain you receive (e.g., 80% participation rate or 6% annual cap)

How Downside Protection Works:

- Your principal is never at risk due to market downturns

- Most FIAs guarantee at least 0% credited interest in negative market years

- Some offer minimum guaranteed interest rates (like 1-2% annually)

Additional Features:

- Multiple crediting methods (annual point-to-point, monthly averaging, etc.)

- Flexibility to allocate among different indices and strategies

- Optional riders for enhanced benefits (income guarantees, death benefits)

Understanding the Other Options

Fixed Annuity: While providing guaranteed returns, fixed annuities don’t offer market participation. Sarah would miss out on potential market gains during bull markets.

Variable Annuity: These provide full market participation but no downside protection. Sarah’s account value could decrease significantly during market downturns, failing to meet her risk tolerance.

Immediate Annuity: Again, this describes payment timing rather than the underlying guarantee structure. Sarah could choose an immediate FIA if she wanted income to start right away, but this doesn’t address her specific needs for growth with protection.

Question 3: Market Value Adjustment (MVA)

Question: What does MVA stand for in annuity contracts?

Correct Answer: Market Value Adjustment

Deep Dive Explanation

Market Value Adjustment (MVA) is a sophisticated feature that protects insurance companies from interest rate risk while potentially providing benefits to contract owners. Understanding MVA is crucial for anyone considering annuities with this feature.

How MVA Works:

- When interest rates rise after you purchase your annuity, and you surrender early, you may receive less than your account value

- When interest rates fall after purchase, and you surrender early, you may receive more than your account value

- The adjustment reflects the current market value of the bonds and investments backing your contract

Why Insurance Companies Use MVA:

- Protects them from losses when interest rates change significantly

- Allows them to offer potentially higher initial interest rates

- Helps manage their investment portfolio risk

Impact on Contract Owners:

- Creates potential surrender value volatility in the short term

- May enhance long-term returns through higher credited rates

- Encourages long-term holding rather than frequent surrenders

Important Considerations:

- MVA typically only applies during the surrender charge period

- The adjustment can work in your favor if rates have declined

- Most contracts provide detailed formulas for calculating MVA

Understanding the Other Options

Minimum Value Addition: This isn’t a standard insurance term and doesn’t relate to actual annuity features.

Maximum Variable Allocation: This might sound like it relates to variable annuities, but it’s not a standard term in annuity contracts.

Monthly Value Assessment: While some annuities do provide monthly statements, this isn’t what MVA stands for and doesn’t capture the interest rate adjustment concept.

Question 4: Contract Cancellation Rights

Question: During which period can an annuity owner cancel their contract and receive a full refund of premiums paid?

Correct Answer: Free Look Period

Deep Dive Explanation

The Free Look Period is one of the most important consumer protections in annuity contracts, providing a safety net for purchasers who may have second thoughts or discover the product isn’t suitable for their needs.

Key Features of the Free Look Period:

- Typically lasts 10-30 days (varies by state and insurance company)

- Begins when you receive your contract or sometimes when you sign the application

- Allows complete cancellation with full premium refund

- No surrender charges, fees, or penalties apply

- May include a small deduction for investment losses in variable products

Why This Protection Exists:

- Annuities are complex products that require careful consideration

- Provides time to review contract details with advisors or family

- Protects against high-pressure sales tactics

- Ensures purchasers fully understand their commitment

How to Exercise Free Look Rights:

- Must provide written notice to the insurance company

- Usually must return the original contract

- Should be sent via certified mail for proof of delivery

- Some companies accept electronic cancellation requests

State Variations:

- California: 30 days for all annuities

- New York: 30 days, with additional protections for seniors

- Texas: 20 days for most annuities

- Many states: 10-20 day periods, depending on product type

Understanding the Other Options

Surrender Charge Period: This is when you’ll pay penalties for withdrawing money, the opposite of fee-free cancellation. This period typically lasts 5-10 years after purchase.

Accumulation Period: This refers to the phase when your annuity is growing in value before you begin receiving payments. You can often make partial withdrawals during this time, but not cancel completely without potential charges.

Annuitization Period: This is when you convert your annuity into a stream of income payments. Once annuitized, you typically cannot cancel the contract or access the lump sum value.

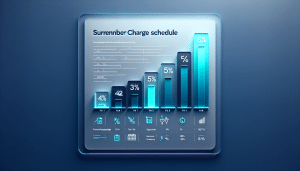

Question 5: Surrender Charge Structure

Question: Surrender charges typically:

Correct Answer: Decrease over time and eventually disappear

Deep Dive Explanation

Surrender charges represent one of the most significant features affecting annuity liquidity, and understanding their structure is crucial for effective financial planning.

Typical Surrender Charge Schedule:

- Year 1: 7-10% of the withdrawal amount

- Year 2: 6-9%

- Year 3: 5-8%

- Continuing to decrease annually

- Years 7-10: 0% (charges eliminated)

Why Surrender Charges Exist:

- Compensate insurance companies for upfront costs (commissions, underwriting, setup)

- Encourage long-term holding to match the company’s investment strategy

- Allow companies to offer higher interest rates or better features

- Help insurance companies manage their asset-liability matching

How They’re Applied:

- Usually calculated as a percentage of the amount withdrawn

- Often applied only to amounts exceeding the annual free withdrawal allowance (typically 10% of account value)

- May be based on premium payments or account value, depending on the contract

- Some contracts use a declining percentage of the premium rather than the account value

Strategies to Minimize Impact:

- Take advantage of annual free withdrawal allowances

- Plan withdrawals to occur after the surrender period ends

- Understand exactly when the surrender period begins and ends

- Consider contracts with shorter surrender periods if liquidity is important

Understanding the Other Options

Increase over time: This would be highly unusual and consumer-unfriendly. No reputable insurance companies structure surrender charges this way.

Remain constant throughout the contract: While some contracts might have level charges for a few years, the industry standard is decreasing charges that eventually disappear.

Only apply to variable annuities: Surrender charges are common across all annuity types – fixed, variable, and indexed. The charge structure is more related to the insurance company’s cost recovery than the underlying investment approach.

Question 6: Variable Annuity Fund Management

Question: John purchased a variable annuity and wants to move money between different investment options. This process is called:

Correct Answer: Fund transfer or exchange

Deep Dive Explanation

Fund transfers or exchanges are a fundamental feature of variable annuities that provide flexibility in investment management while maintaining the tax-deferred status of the contract.

How Fund Transfers Work:

- Money moves between sub-accounts within the same variable annuity contract

- Transfers are typically processed at the next business day’s closing prices

- Most contracts allow transfers via phone, online, or written requests

- No immediate tax consequences since money stays within the annuity wrapper

Transfer Limitations and Rules:

- Many contracts limit the number of free transfers per year (often 12)

- Excessive trading restrictions may apply to prevent market timing

- Some transfers may incur fees after exceeding free limits

- Dollar amounts and percentage restrictions may apply

Strategic Uses:

- Rebalancing portfolios to maintain target asset allocations

- Moving to more conservative investments as retirement approaches

- Taking advantage of perceived market opportunities

- Implementing tactical asset allocation strategies

Tax Advantages:

- All transfers within the variable annuity are tax-free

- Maintains tax-deferred growth on all investments

- Avoids the wash sale rules that might apply in taxable accounts

- Allows for sophisticated tax planning strategies

Understanding the Other Options

Dollar Cost Averaging: This is an investment strategy involving regular, systematic investments over time to reduce timing risk. While you might implement dollar cost averaging within a variable annuity, it’s not the term for moving money between existing investments.

Asset Allocation: This refers to how you divide your investments among different asset categories (stocks, bonds, cash). While fund transfers help implement asset allocation strategies, the term doesn’t specifically describe the transfer process.

Portfolio Rebalancing: This is the practice of adjusting your portfolio back to your target allocation, often accomplished through fund transfers. However, rebalancing is the strategy, while fund transfer/exchange is the mechanism to execute it.

Question 7: Consumer Protection Timeline

Question: The typical free look period for annuities is:

Correct Answer: 10-30 days

Deep Dive Explanation

The 10-30 day range for free look periods reflects the variation in state insurance regulations and individual insurance company policies, representing a balance between consumer protection and business practicality.

State-by-State Variations:

Longer Periods (20-30 days):

- California: 30 days for all annuities

- New York: 30 days with enhanced senior protections

- Florida: 21 days for most products

- Illinois: 20 days with additional review periods for seniors

Standard Periods (10-15 days):

- Many states provide 10-day minimums

- Some extend to 14-15 days for certain products

- Federal regulations may influence state standards

Factors Affecting Length:

- Product complexity (variable annuities often have longer periods)

- Purchaser age (seniors may receive extended periods)

- Sales method (direct vs. agent sales)

- Insurance company policies (may exceed state minimums)

When the Period Begins:

- Contract delivery date (most common)

- Application signature date

- First premium payment date

- Varies by state regulation and company policy

Enhanced Protections:

- Some states provide additional review periods for seniors

- Certain products may have extended suitability review periods

- High-premium contracts might receive longer consideration periods

Understanding the Other Options

5-7 days: This would be insufficient time for most consumers to properly review complex annuity contracts and would fall below most state minimum requirements.

60-90 days: While this might seem consumer-friendly, such long periods would be impractical for insurance companies to manage and would likely increase product costs significantly.

One year: This would essentially make annuity purchases tentative for an entire year, creating significant business and regulatory challenges that no state has implemented.

Key Takeaways for Annuity Buyers

Before You Buy

- Understand your needs: Determine whether you need guaranteed income, growth potential, or downside protection

- Review the free look period: Know exactly how long you have to change your mind

- Examine surrender charges: Understand the cost of early withdrawals and plan accordingly

- Consider product complexity: Match the product sophistication to your understanding and needs

During Ownership

- Monitor performance: Regularly review your annuity’s performance and features

- Utilize transfer privileges: In variable annuities, use transfer options strategically

- Plan withdrawals: Take advantage of free withdrawal allowances when possible

- Stay informed: Keep up with any contract changes or new features

Working with Professionals

- Ask questions: Don’t hesitate to seek clarification on any features you don’t understand

- Get everything in writing: Ensure all representations are documented

- Review regularly: Schedule periodic reviews to ensure your annuity still meets your needs

- Understand fees: Be clear on all costs associated with your annuity

Conclusion

Annuities are sophisticated financial products that can play valuable roles in retirement planning, but they require careful consideration and understanding. Each type of annuity serves different needs, and features like MVA, surrender charges, and free look periods significantly impact their suitability for individual situations.

The key to successful annuity ownership lies in matching the right product features to your specific financial goals, risk tolerance, and liquidity needs. Take advantage of the free look period to ensure you’ve made the right choice, and don’t hesitate to seek professional guidance when navigating these complex products.

Remember, the best annuity is the one that aligns with your financial situation and retirement goals, not necessarily the one with the highest returns or most features.