Should I Rollover My 401k?

Do you have assets in one or more employer-sponsored retirement plans (i.e., 401(k), 403(b), profit-sharing plans) to which you are no longer contributing?

Funds in a 401(k) may be exposed to the highs and lows of the stock market, and may not be protected from losses. This exposure can be especially risky as you get close to retirement because your savings have less time to recover from a market downturn.

Do you want to continue...?

- Tax Deferral

- Growth Potential

With the added benefits of...

- Protection from loss due to market downturns

- Guaranteed lifetime income

- Flexibility to customize income

- Creating a legacy

Achieve your retirement goals

Rolling over tax-qualified retirement assets into

an indexed annuity can help you achieve your

retirement goals. Plus, you’ll receive the added

benefits an annuity provides.

What is an annuity?

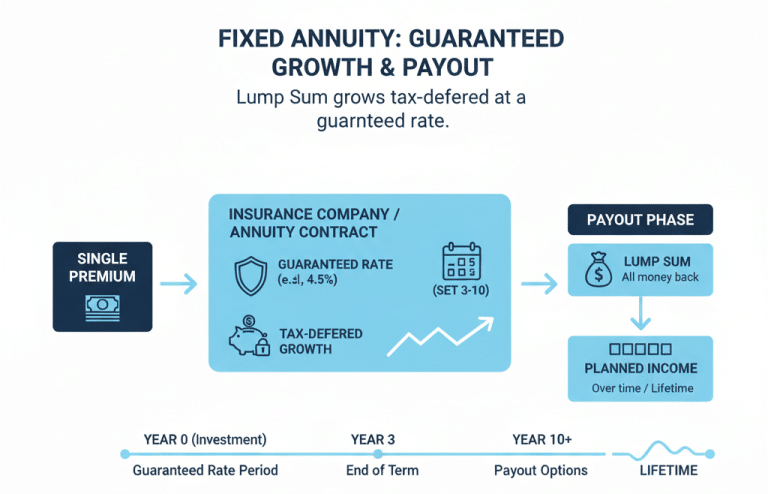

Annuities provide insurance against the risk that you’ll outlive your money after you retire. They give you the potential to grow your retirement savings and create a guaranteed income stream to last a lifetime.

A rollover into an annuity can help you achieve your retirement goals if you’re looking for…”

Continued tax deferral

Continued tax deferral — Rollovers are tax-free as long as they follow IRS guidelines. You don’t pay taxes on any growth in your annuity until you withdraw money.

Guaranteed Lifetime Income

Create a stream of income using Lifetime Income Withdrawals from an income rider, available for a charge.

Growth Potential

Pursue additional growth with interest credits based, in part, on the upward movement of an external market index

Flexibility

In addition to guaranteed lifetime withdrawals, an income rider may also offer additional benefits, such as inflation protection, benefits for confinement or terminal illness, and a death benefit.

Protection from market downturns

Fixed and fixed index annuities guarantee your annuity will not lose money due to market downturns. Although you may earn zero percent interest in any given term period, you’ll never earn less than zero.

Legacy for you loved ones.

Offer your loved ones a quick source of funds to settle matters after your death. Your beneficiary is guaranteed to receive your annuity’s full Accumulated Value or Minimum Guaranteed Contract Value, whichever is greater.

Are you currently working and have a 401k?

Consider this...

Funds in a 401(k) may be exposed to the highs and lows of the stock market, and may not be protected from losses. This exposure can be especially risky as you get close to retirement, because your savings have less time to recover from a market downturn.

Protect a portion of your retirement savings with an in-service distribution in an annuity.

How do you benefit?

The money in a fixed or fixed indexed annuity is not directly exposed to the risks of the stock market or individual stocks. We guarantee you will not lose money due to stock market risk or losses.

How does it work?

An in-service distribution, if permitted by your plan, allows individuals who are still working to directly roll over a portion of their vested balance from an employer-sponsored retirement plan into an Individual Retirement Account (IRA), such as an indexed annuity or fixed annuity.

In-service distributions may be taken from 401(k), 403(b) and 457 plans, as well as pensions and profit-sharing plans.

Since the money directly moves from one qualified plan to another, in-service distributions are not a taxable event and the money remains shielded from taxes until you begin taking money from your annuity.

Additional Features

You can withdraw money from your annuity without an IRS penalty before you retire once you reach age 59½.4 Plus, an annuity gives you the ability to create a guaranteed stream of income for life.

Achieve your retirement goals with a 401k rollover.

An annuity provides you with continued tax deferral, growth potential and protection from market risk or losses in addition to an income you can’t outlive.

Today’s retirees are living longer, more active lives than any generation before them. In fact, Americans on average will spend 20 years in retirement.¹ Making sure you have adequate income for two decades after you stop working can be a challenge, and fixed-indexed annuities can help.

Case Study: Cliff and Sherri's Story

Cliff and Sherri are married and are both 50 years old. They are employed full time and contribute regularly to 401(k) plans and Individual Retirement Accounts (IRAs). Both Cliff and Sherri hope to retire in 10 years so they can devote time to travel. One of their goals is to visit each one of America’s National Parks.

While they are confident that they are doing all they can to save for retirement, Cliff and Sherri are concerned about retirement income. Since neither has an employer sponsored pension plan they’ll need to rely on their personal savings to help cover essential expenses, especially during their first 10 years of retirement.

This is because they want to delay taking Social Security until they reach age 70 so they can maximize their benefits. They’re also worried about potentially hefty medical insurance premiums until Medicare kicks in at age 65. After talking with their insurance agent, the couple purchases a fixed indexed annuity with an income rider as part of their overall retirement income strategy.

Fixed indexed annuity in action

AGE 50

Roll over $100,000, from a 401(k) that Jim has from a previous

employer, to a fixed indexed annuity (10-year withdrawal charge

schedule) with an income rider.

What does this do?

• Allows Cliff and Sherri to continue to grow those assets on a tax-deferred basis.

• Preserves principal by protecting against loss due to market downturns.• Provides income growth potential

AGE 60

Turn on income from the rider.

Cliff and Sherri receive $6,300 annually, which is their guaranteed

lifetime withdrawal amount.²

What does this do?

• Gives Cliff and Sherri a steady flow of income they can count on

for the rest of their lives.

• Provides an additional income stream to help pay for health

insurance and other expenses.

AGE 65

Medicare Begins

AGE 70

The couple starts taking Social Security benefits.³

Fixed indexed annuities are not stock market investments and do not directly participate in any stock or equity investments. Market Indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an Index nor any market-indexed annuity is comparable to a direct investment in the equity markets. Clients who purchase indexed annuities are not directly investing in a stock market index.

Guarantees provided by annuities are subject to the financial strength of the issuing insurance company. Check with your plan administrator or review your plan documents for withdrawal options, eligibility, and rules. This includes how an in-service withdrawal may affect vesting and your ability to contribute to your employer-sponsored plan. 4 Taxable amounts withdrawn prior to age 59½ may be subject to a 10% IRS penalty in addition to ordinary income tax. Withdrawals in excess of the free amount allowed in the contract may be subject to Withdrawal Charges and a Market Value Adjustment and will forfeit any interest accrued during the term that is attributed to the excess amount. Annuities contain features, exclusions, and limitations that vary by state. For a full explanation of an annuity, please refer to the Certificate of Disclosure and contact your Financial Professional or the company for costs and complete details. Under current tax law, the Internal Revenue Code already provides tax deferral to qualified money, so there is no additional tax benefit obtained by funding a qualified contract, such as an IRA, with an annuity; consider the other benefits provided by an annuity, such as lifetime income and a Death Benefit. Any information regarding taxation contained herein is based on our understanding of current tax law. The tax and legislative information may be subject to change and different interpretations. We recommend that you seek professional legal advice for applicability to your personal situation.

1 Department of Labor, “Top 10 Ways to Prepare for Retirement,” September 2015, https://www.dol.gov/sites/default/files/ebsa/about-ebsa/our-activities/resourcecenter/publications/top-10-ways-to-prepare-for-retirement.pdf

2 Assumes a hypothetical income rider roll-up rate of 8.0% and 10 years of income deferral. Also assumes no withdrawals during the 10-year withdrawal charge

period. The hypothetical example is for informational purposes only and is not indicative of the past, nor intended to predict the future performance of any specific

product including an annuity; nor is it intended to represent any particular product or interest crediting method.

3 It’s important to consult with financial, tax, and legal professionals to determine when it’s best to begin taking your Social Security benefits. A number of factors

can play into this very important decision, including taxes, future income, the age difference between spouses, potential medical issues, and former earnings

history. For more information about Social Security, you can read: “When to Start Your Benefits” available at http://www.ssa.gov/retire2/applying1.htm