IRA Contribution Limits 2021

The IRS announced Monday that IRA contribution limits would remain unchanged for 2021. They also announced the income ranges for eligibility would increase for 2021, although not by much.

For 2021, the total max contributions you make to all of your traditional IRAs and Roth IRAs can’t be more than:

- $6,000 ($7,000 if you’re age 50 or older), or

- If less, your taxable compensation for the year

Roth IRA contribution limit

In addition to the general contribution limit that applies to both Roth and traditional IRAs, your Roth IRA contribution may be limited based on your filing status and income.

The IRA contribution limit does not apply to:

- Rollover contributions

2021 IRA Contribution Limits

- 401(k) contribution limits for 2021 are unchanged at $19,500.

- Catch-up contribution limits for employees aged 50 and over remain unchanged at $6,500.

- The limitation regarding SIMPLE retirement accounts remains unchanged at $13,500.

- The limit on annual contributions to an IRA remains unchanged at $6,000.

As the IRS explains in Notice 2020-79, taxpayers can deduct contributions to a traditional IRA if they meet certain conditions.

If during the year either the taxpayer or his or her spouse was covered by a retirement plan at work, the deduction may be reduced, or phased out, until it is eliminated, depending on filing status and income. (If neither the taxpayer nor his or her spouse is covered by a retirement plan at work, the phase-outs of the deduction do not apply).

2021 IRA Income Phase-Out Amount

- For single taxpayers covered by a workplace retirement plan, the phase-out range is $66,000 to $76,000, up from $65,000 to $75,000.

- For married couples filing jointly, where the spouse making the IRA contribution is covered by a workplace retirement plan, the phase-out range is $105,000 to $125,000, up from $104,000 to $124,000.

- For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out if the couple’s income is between $198,000 and $208,000, up from $196,000 and $206,000.

- For a married individual filing a separate return who is covered by a workplace retirement plan, the phase-out range is not subject to an annual cost-of-living adjustment and remains $0 to $10,000. The income limit for the Saver’s Credit (from $65,000; $49,500 for heads of household, up from $48,750; and $33,000 for singles and married individuals filing separately, up from $32,500.

IRA Alternatives

QLACs

- The income phase-out range for taxpayers making contributions to a Roth IRA is $125,000 to $140,000 for singles and heads of household, up from $124,000 to $139,000. For married couples filing jointly, the income phase-out range is $198,000 to $208,000, up from $196,000 to $206,000. The phase-out range for a married individual filing a separate return who makes contributions to a Roth IRA is not subject to an annual cost-of-living adjustment and remains $0 to $10,000.

Roth IRA Phase-Out Limits 2021

The inflation adjustment helps Roth IRA savers too. In 2021, the AGI phase-out range for taxpayers making contributions to a Roth IRA is $198,000 to $208,000 for married couples filing jointly, up from $196,000 to $206,000 in 2020. For singles and heads of households, the income phase-out range is $125,000 to $140,000, up from $124,000 to $139,000 in 2020.

2021 Deductible IRA Phase-Outs

You can earn a little more in 2021 and get to deduct your contributions to a traditional pretax IRA. Note: Even if you earn too much to get a deduction for contributing to an IRA, you can still contribute–it’s just nondeductible.

In 2021, the deduction for taxpayers making contributions to a traditional IRA is phased out for singles and heads of household who are covered by a workplace retirement plan and have modified adjusted gross incomes (AGI) between $66,000 and $76,000, up from $65,000 and $75,000 in 2020. For married couples filing jointly, in which the spouse who makes the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $105,000 to $125,000 for 2021, up from $104,000 to $124,000.

Estate and Gift Tax Changes for 2021

The annual exclusion gifts that can be made to anyone remained at $15,000, per person.

The estate and gift tax exemptions saw the biggest increases; the 2021 transfer tax exemption (estate, gift and generation-skipping tax) is $11,700,000 per person, up from $11,580,000 in 2020, an increase of $120,000.

The standard deduction, is up slightly to $25,100 for married – joint, $12,550 for singles, and $18,800 for the head of household.

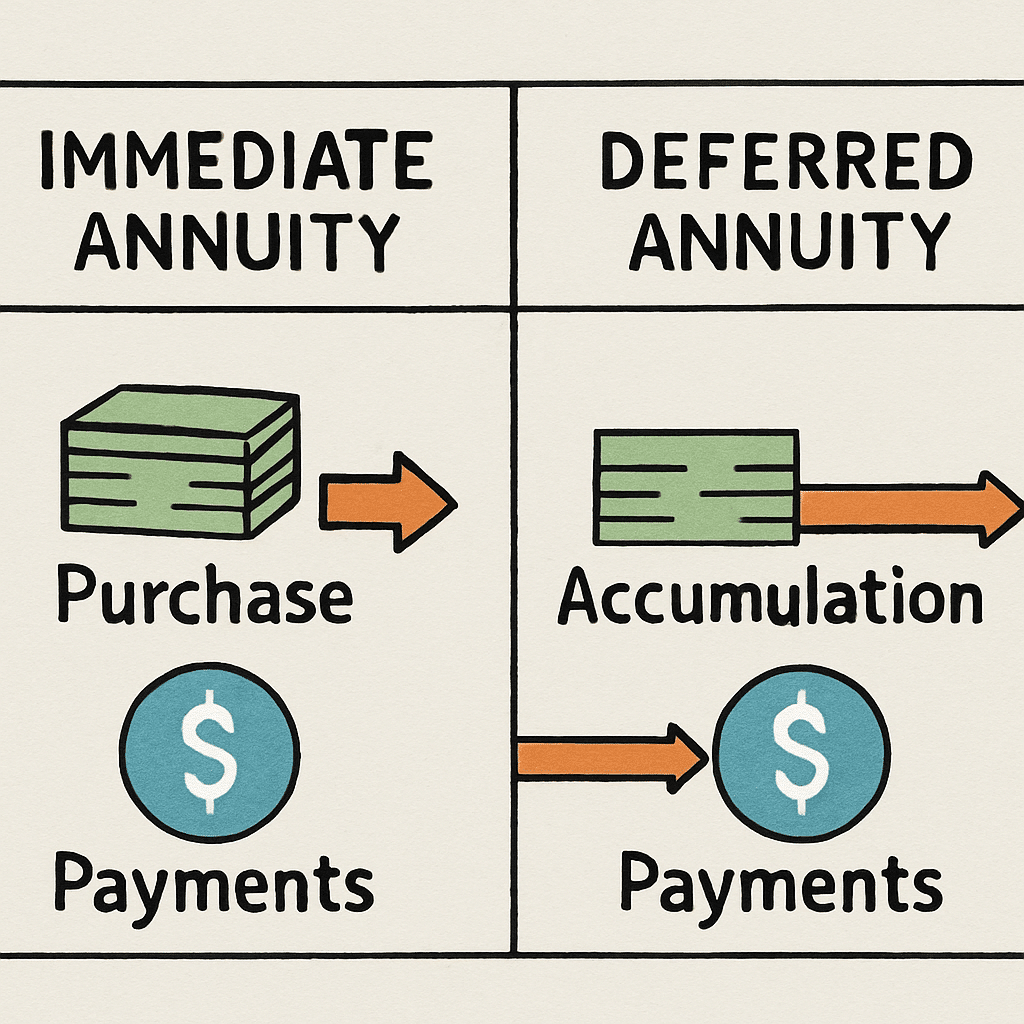

Annuities

Despite the not-so-good news, there is no limit on how much you can invest in an annuity. Annuities are meant to be long-term retirement savings vehicles and as such, they can grow tax-deferred allowing you to earn compound interest on the money you normally would have been paying taxes on.

You do not have to claim interest earned as income in the year it was earned. For those savers with money in a CD; an annuity may be a good option to consider. You can compare today’s best annuity rates at our online annuity store.

Roth IRA Phase-Out Limits 2021

The inflation adjustment helps Roth IRA savers too. In 2021, the AGI phase-out range for taxpayers making contributions to a Roth IRA is:

- $198,000 to $208,000 for married couples filing jointly.

- For singles and heads of households, the income phase-out range is $125,000 to $140,000

2021 Deductible IRA Phase-Outs

You can earn a little more in 2021 and get to deduct your contributions from a traditional pretax IRA. Note: Even if you earn too much to get a deduction for contributing to an IRA, you can still contribute–it’s just nondeductible.

In 2021, the deduction for taxpayers making contributions to a traditional IRA is phased out for singles and heads of household who are covered by a workplace retirement plan and have modified adjusted gross incomes (AGI) between $66,000 and $76,000, up from $65,000 and $75,000 in 2020. For married couples filing jointly, in which the spouse who makes the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $105,000 to $125,000 for 2021, up from $104,000 to $124,000.

Estate and Gift Tax Changes for 2021

The annual exclusion gifts that can be made to anyone remained at $15,000, per person.

The estate and gift tax exemptions saw the biggest increases; the 2021 transfer tax exemption (estate, gift, and generation-skipping tax) is $11,700,000 per person, up from $11,580,000 in 2020, an increase of $120,000.

The standard deduction, is up slightly to $25,100 for married – joint, $12,550 for singles, and $18,800 for the head of household.

Annuities

Despite the not-so-good news, there is no limit on how much you can invest in an annuity. Annuities are meant to be long-term retirement savings vehicles and as such, they can grow tax-deferred allowing you to earn compound interest on the money you normally would have been paying taxes on.

You do not have to claim interest earned as income in the year it was earned. For those savers with money in a CD; an annuity may be a good option to consider. You can compare today’s best annuity rates at our online annuity store.

IRA Alternatives

QLACs

The dollar limit on the amount of your IRA or 401(k) you can invest in a qualified longevity annuity contract is still $135,000 for 2021.

Annuities

Despite the not-so-good news, there is no limit on how much you can invest in an annuity. Annuities are meant to be long-term retirement savings vehicles and as such, they can grow tax-deferred allowing you to earn compound interest on the money you normally would have been paying taxes on.

You do not have to claim interest earned as income in the year it was earned. For those savers with money in a CD; an annuity may be a good option to consider. You can compare today’s best annuity rates at our online annuity store.