A Simple Annuity Wealth Transfer Strategy Anyone Can Implement

When you hear a financial advisor talking about wealth transfer strategies Life Insurance is almost always at the heart of the conversation which certainly makes sense.

However, I’ve often seen situations where a client isn’t healthy enough to purchase life insurance, at least not at a reasonable rating. Sometimes you can simply be too old for life insurance to provide any real attractive leverage.

While an annuity is often thought of as a tool to generate lifetime income or safely grow your retirement savings there are a few annuity wealth transfer strategies worth knowing about. lifetime income or safe retirement savings tool they

Thanks, Gramps!

Immediate Annuity with a Non-Spousal Joint Annuitant

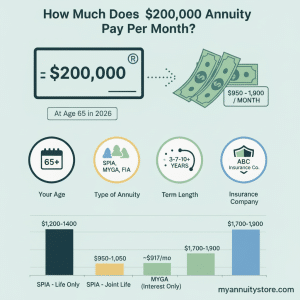

My “Thanks Gramps” annuity wealth transfer strategy is very simple to implement and Ihas also been known to pull on your heartstrings. I refer to it as the “Thanks Gramps” strategy so I will use a grandfather and granddaughter as the example. You may be aware of immediate annuities, or income annuities. An income annuity is the oldest form of an annuity as guarantees a monthly income for as long as you are alive in exchange for a lump-sum payment.

Oftentimes, a husband and wife will purchase an immediate annuity to generate a floor level of income in retirement and purchase the joint lifetime income option, this way the income is guaranteed to continue as long as either is alive. If your goal is to transfer wealth to your beneficiaries you may consider purchasing an immediate annuity with a grandchild as the joint annuitant rather than your spouse.

The younger annuity has a very big impact on income annuities’ monthly income factor as they have the longest life expectancy. When you purchase an immediate annuity with a much younger joint annuitant your income payments are going to be quite small. This can be a good thing since we’ve already established you have more assets than you need for income and a smaller income payment will have very little to no adverse tax consequences for you.

Cost of Living Adjustment Option (COLA)

Since a joint lifetime, the immediate annuity continues to pay for as long as either annuitant is alive the income payments will continue much after you’ve passed. There are a couple of additional techniques to implement should you decide to utilize this annuity wealth transfer strategy. First, rather than take a level income option you will want to select the highest COLA (cost of living adjustment) option available in the annuity contract. The available COLA options will range anywhere from 3 to 6% depending on the insurance company issuing the policy.

In doing so, your grandchild’s income will increase drastically over his or her lifetime. Consider you utilize this strategy with a 7-year-old grandchild with a 6% cost of living adjustment and they live to be 87. That means they will get a 6% pay increase 80 times.

Give Your Beneficiaries Birthday Gifts from your Grave

Finally, I think it is a really neat idea to take annual income payments rather than monthly income should you consider utilizing this concept. In addition to taking an annual income payment, I suggest making structuring the immediate annuity so that the annual payments fall on your grandchild’s birthday.

I have had a handful of clients take me up on this over the years and I asked that they make out a few birthday cards to their grandson or granddaughter for the more monumental birthdays such as sweet-16 and 21.

Advantages of an Immediate Annuity with a Non-Spousal Joint Annuint and COLA

- Spread out any gains in contract over a long period of time if it is a Non-Qualified Annuity

- If it is an IRA Annuity your withdrawals may help to satisfy you RMD amont.

- There is a very long time for the Cost of Living Adjustment to Compound

- Give Your Beneficiary a Birthday Gift Every Year even after you've gone

- Can be purchased with as little as $10,000