You Probably Want to Buy an Annuity but You Just Don't Know it!

The annuity industry has seen much change since I began my career in 2005. As an annuity wholesaler 10 years ago I was constantly battling a negative stereotype of annuities; fixed index annuities in particular.

Quite a few of the Broker-Dealers I worked with would not even allow their advisers to sell an indexed annuity. It seemed like it was on a daily basis that advisers would ask why someone would sell an indexed annuity with an income rider when they could add a similar guaranteed lifetime withdrawal benefit rider to a variable annuity.

I once had an older financial advisor tell me buying an indexed annuity was like putting a trampoline in the basement.

Fixed annuity sales have outperformed variable annuity (VA) sales in 11 of the last 13 quarters and represent 63% of overall annuity sales. If you want my opinion – I believe fixed indexed annuities are the darling of all available fixed-income options.

I feel we should all take pride as an industry and a profession in what we’ve been able to accomplish in terms of helping so many Americans protect a portion of their retirement savings/ income using annuities. According to LIMRA SRI, fixed annuity sales grew from $73 Billion in 2007 to $117 Billion in 2016.

2016 also marked the first time that fixed annuity sales surpassed variable annuity sales. While we’ve taken great strides a recently published study suggests we still have a lot of work to do in terms of educating consumers on the features and benefits of an annuity.

Retirees Describe Annuities as Ideal Investment

A study titled “The Language of Retirement” was conducted in March 2017 on behalf of the Insured Retirement Institute (IRI) and Jackson National. The results of the survey revealed much about advisers’ and consumer attitudes toward income in retirement.

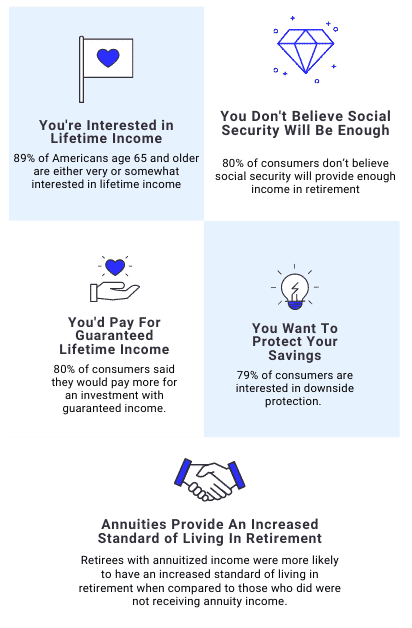

Interviews were conducted with 1000 consumers and 400 advisors to gauge their familiarity with and favorability towards various financial products. Of the respondents who were 65 years old or older, 89% were very/somewhat interested in lifetime income.

Behind lifetime income, principal protection was the second most commonly desired feature of a financial product, and tax deferral wasn’t far behind. Below are a few of the survey’s findings that would indicate we still have a bias against annuities to overcome:

80% of consumers don’t believe social security will provide enough income in retirement

51% of surveyed retirees said they intend to withdraw from retirement savings as needed for income

More than 90% of respondents were very interested in lifetime income but only 48% own an annuity

79% listed downside protection as a top priority

80% of respondents said they would pay more for investments that provide a guaranteed lifetime income

Why Don't Advisor's Like Annuities?

The 400 financial advisors surveyed were asked to list the top reasons they did not offer annuity products to more of their client base.

The top reasons, in order, were:

Negative client perception

Regulatory concerns

Transaction complexity, and

Difficulty explaining the annuity products

More than half of the advisers interviewed believe at least some of their clients who don’t own annuities will run out of money in retirement.

Annuities Increase Satisfaction in Retirement

A 2003 RAND study found that retirees who receive annuity income payments tend to be more satisfied in retirement than those who do not.

They were also more likely to maintain their standard of living in retirement than their peers who didn’t hold an annuity in their retirement portfolio.

In 2012 TIAA CREF studied 1000 retirees age 60 and older, with at least $400K in IRA assets. 500 had an annuitized income stream while the other 500 did not. Those clients with annuitized income were more likely to have an increased standard of living in retirement when compared to those who did not receive annuity income.

Annuitization and guaranteed lifetime income riders are consistent with the top financial priorities of pre-retirees and those who are already enjoying retirement.

The vast majority of annuity and non-annuity owners reported almost identical financial priorities.

Researchers have yet to identify a driving reason so many in more retirees do not own an annuity. After much effort, the best identifying factor academia can offer is that there appears to be some disconnect regarding this decision.

"A lack of educational materials and access to structured products and annuities have hindered the widespread adoption of these strategies in the United States."

Annuities Help Mitigate Volatily & Inflation

It is quite possible that those retirees who choose not to invest a portion of their retirement nest egg into an annuity don’t know annuities likely address their top financial concerns.

80% of those surveyed that were 65 or older were either advised not to purchase an annuity, or, did not receive any advice at all regarding annuities. Meanwhile, 60% of those with an annuitized income stream were advised to do so.

Annuities are the only financial product that can provide the guaranteed lifetime income that so many Americans want and need. As uncertainty creeps back into the marketplace the guarantees that only annuities provide will become increasingly important.

My takeaway from all of this is that advisers can be the ones to move the needle in helping more retirees secure lifetime income using annuities, but they need more support and education regarding annuity solutions.

At My Annuity Store, we have a strong passion and are 100% committed to the annuity industry. As a result, we’ve invested much time and resources into building an annuity platform that provides everyone access to independent, unbiased, and transparent annuity products and education.

Our team is experienced, knowledgeable, and eager to help you, help your clients. We’ve internalized the importance of what we do for a living and I know you’ll enjoy the professionalism with which we conduct business.

📊

Get Today's Best MYGA Rates

Compare A-rated carriers. Rates up to 6.50%. No obligation.

Editorial Disclosure: Our editorial team independently reviews and rates annuity products. We may earn commissions when you request a quote through our partner links. This content is for informational purposes only and does not constitute financial advice. Learn more.

Disclaimer: This content is for informational and educational purposes only. It does not constitute financial, tax, or legal advice. Annuity products vary by state and carrier. Always consult a licensed financial professional before making any financial decisions. My Annuity Store is an independent marketplace and does not provide investment advice.

My Annuity Store sources rate data from AnnuityRateWatch, which surveys MYGA and fixed annuity offerings from insurance carriers across all available terms (2–10 years). Rate data is refreshed daily to ensure accuracy.

To identify the best rates, we evaluate carriers on: credited interest rate, AM Best financial strength rating (A- or better only), minimum premium requirement, surrender charge schedule, and free withdrawal provisions. Only A-rated carriers are included in our comparisons.

Rates shown are not an offer or solicitation. Rate availability varies by state. Always verify current rates with a licensed insurance professional before purchasing an annuity product.

📊 Data: AnnuityRateWatch · A-rated carriers only · Updated daily

Carriers We Monitor

My Annuity Store tracks rates from 50+ A-rated carriers. Here are some of the top providers included in our comparisons.

Product innovation and our current interest rate environment have turned the tables. According to LIMRA Secure Retirement Institute’s Q1 2019 U.S. Retail Annuity Sales Survey, first quarter 2019 fixed annuity sales were $38 billion, a 38% increase Year over Year.

Product innovation and our current interest rate environment have turned the tables. According to LIMRA Secure Retirement Institute’s Q1 2019 U.S. Retail Annuity Sales Survey, first quarter 2019 fixed annuity sales were $38 billion, a 38% increase Year over Year.