How Do Index Annuities Work?

Annual Point to Point

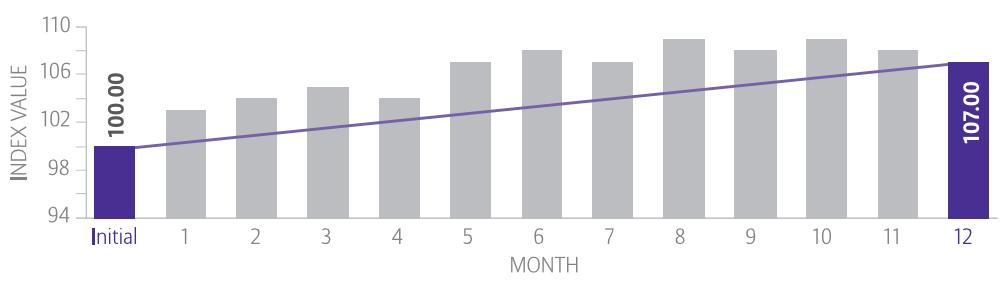

Annual point-to-point is the simplest and most commonly used indexed annuity crediting method. Annual point-to-point uses the index value from only two points in time so this may be a good choice if you want to minimize the effects of mid-year market volatility.

- The index value from the beginning of the crediting period is subtracted from the value of the index at the end of the crediting period.

- The percentage of change is calculated.

- If the value at the end of the year is higher than the beginning of the year crediting component is applied to determine your interest credited.

As an example let’s assume an index change of 7% and apply the cap, spread, or participation rate. For this example, we will assume a 5% cap, a 2% spread, and a 75% participation rate.

5% Cap = 5% Interest credited (index change up to the cap)

2% Spread = 5% Interest credited (index change – spread)

75% Participation Rate = 5.25% Interest Credited (index change X spread)

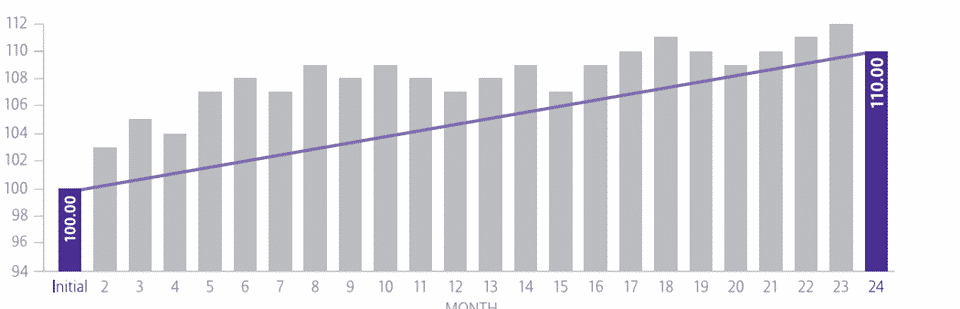

2-year point-to-point uses the index value from two points in two contract years apart so this index annuity crediting method may be a good choice if you want to limit the effects of volatility between these two points.

The index value from the beginning of the crediting period is subtracted from the value of the index at the end of your second crediting period (two years). The percentage of change is calculated. If the value at the end of the second year is higher than the beginning of period one a crediting component is applied to determine your interest credited.

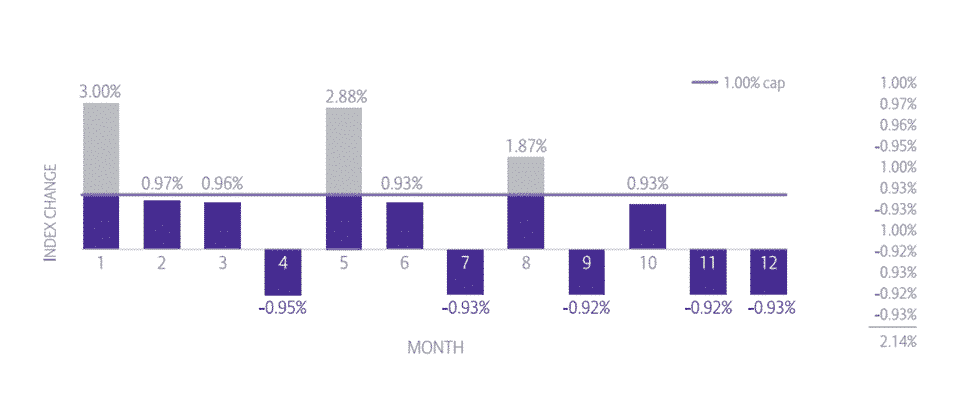

The monthly sum is the most volatility-sensitive index annuity crediting method. It can provide the most interest in steady up-markets but it can be adversely affected by large monthly decreases.

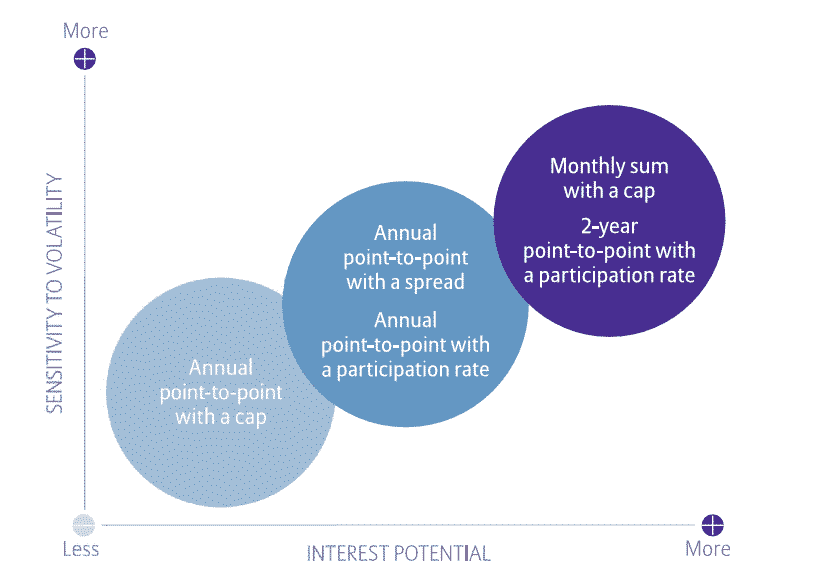

The index annuity crediting method you select can significantly impact how much interest you earn so you should consider your options carefully. The chart below shows each index annuity crediting method’s sensitivity to volatility and interest potential.

The monthly sum is the most sensitive to volatility but also has the highest earning potential.