Transferring an annuity to a trust is a strategic move in estate planning. It involves shifting ownership of an annuity to a trust. This can offer several benefits.

An annuity provides a steady income stream, often used for retirement. A trust, on the other hand, is a legal arrangement. It allows a trustee to manage assets for beneficiaries.

Combining these two can enhance financial security. It can also offer asset protection and tax advantages. However, the process is not without complexities.

Understanding the differences between annuities and trust funds is crucial. Each has unique features and benefits. Annuities provide income, while trust funds offer flexibility.

Tax implications are a significant consideration. Transferring an annuity to a trust can trigger tax liabilities. It’s essential to understand these before proceeding.

Legal and financial advice is vital. Professionals can guide you through the process. They ensure that your financial goals are met.

This guide will explore the nuances of transferring an annuity to a trust. It will help you make informed decisions.

Summary

Transferring an annuity to a trust can combine predictable income with enhanced control, asset protection, privacy, and estate planning efficiency. The strategy includes important choices, like revocable and irrevocable trusts. It requires a careful review of annuity contract terms. You must also pay attention to legal and tax consequences. These include ordinary income tax, trust tax rates, state rules, and possible taxable events from ownership changes.

A structured process—reviewing contracts, consulting advisors, and executing proper documents—is essential, with common use cases including special needs planning, probate avoidance, and Medicaid strategies. Professional legal, financial, and tax guidance is strongly recommended to align the transfer with your goals and minimize pitfalls.

Understanding Annuities and Trusts

Annuities and trusts serve distinct purposes in financial planning. An annuity is a contract with an insurer to receive regular payments. This income stream is often aimed at retirement needs.

On the other hand, a trust acts as a legal tool. It allows a trustee to hold and manage assets for beneficiaries. Trusts can include various types of assets, providing control and protection.

Let’s look at their core functions:

- Annuities: Primarily designed for income.

- Trusts: Focus on asset management and distribution flexibility.

Deciding whether to use an annuity or a trust involves many factors. The choice depends on your financial situation and objectives. Annuities offer predictability; trusts offer versatility.

Understanding these two options helps in planning a comprehensive estate strategy. Each plays a role in securing your financial future.

Legal and financial experts often recommend a combination of both. This ensures greater control and stability.

The synergy between annuities and trusts can strengthen an estate plan. Consider both avenues to optimize your financial legacy.

Why Consider Transferring an Annuity to a Trust?

Transferring an annuity to a trust can offer several advantages. This action is often motivated by estate planning needs. It allows for the combining of benefits from both annuities and trusts.

A primary reason for this transfer is asset protection. Trusts can shield annuity payouts from creditors. This could provide peace of mind for those wanting to protect their financial legacy.

Another factor is control over annuity distribution. A trust can direct how and when beneficiaries receive funds. This can be beneficial for managing long-term financial needs, especially for minors or those with special needs.

Key reasons to consider transferring an annuity include:

- Asset protection from creditors.

- Controlled distribution to beneficiaries.

- Facilitating estate planning and avoiding probate.

The transfer can streamline estate settlement. Trusts avoid the public nature of probate, providing privacy. This privacy can be beneficial for individuals who wish to keep financial matters confidential.

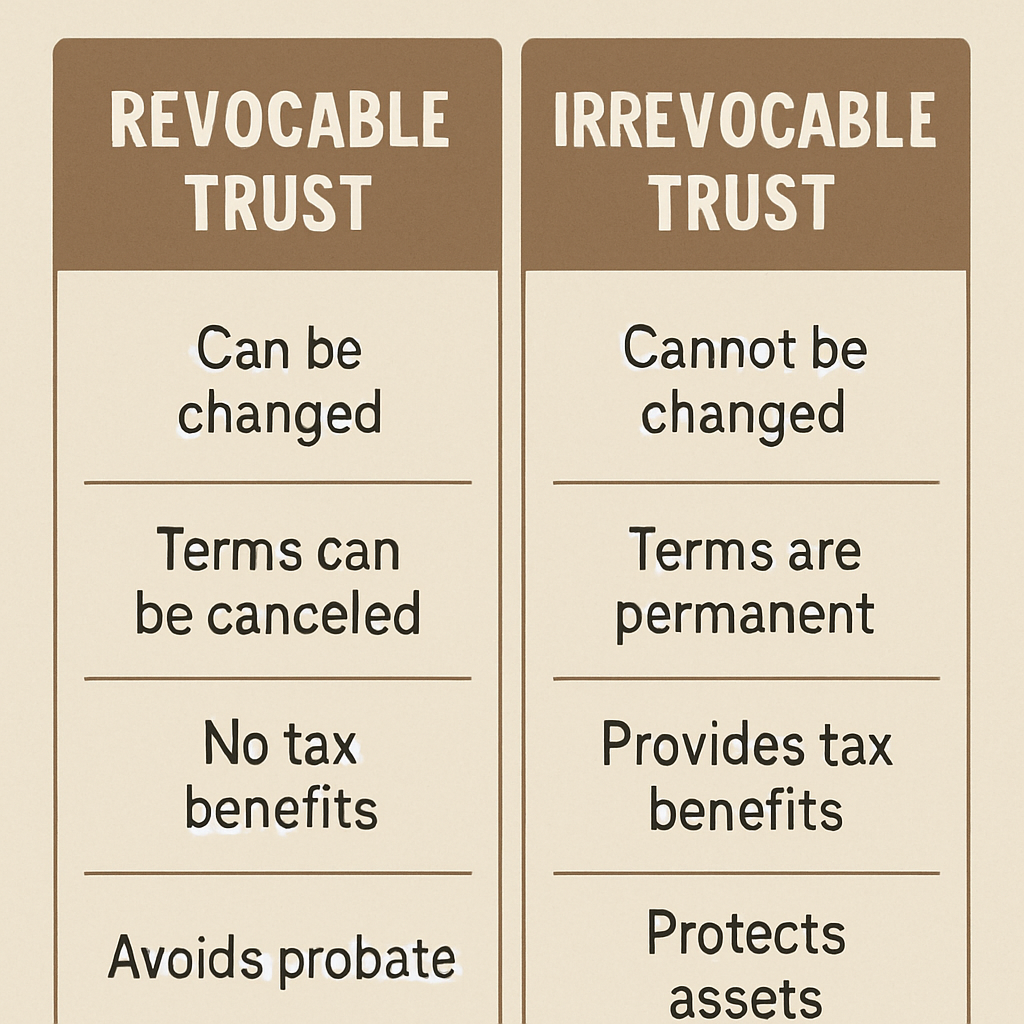

Types of Trusts: Revocable vs. Irrevocable

Understanding the types of trusts is crucial before transferring an annuity. Trusts are primarily categorized as revocable or irrevocable. Each type has distinct benefits and limitations.

A revocable trust offers flexibility. The grantor can modify or dissolve it at any time. This type of trust allows for amendments if circumstances change. However, the assets within a revocable trust are not protected from creditors.

An irrevocable trust is more rigid but provides stronger asset protection. Once established, the grantor cannot easily alter it. Assets in this trust type are typically shielded from creditors. This makes it a suitable choice for long-term asset protection.

Here’s a summary of key differences:

- Revocable Trust:

- Can be amended.

- No creditor protection.

- Irrevocable Trust:

- Cannot be changed easily.

- Provides creditor protection.

Choosing the right trust depends on your financial goals. Consider discussing options with a financial or legal advisor for tailored advice.

The Process of Transferring an Annuity to a Trust

Transferring an annuity to a trust involves several steps, each requiring careful consideration. This process should be approached with detailed planning. It’s vital to ensure the transfer aligns with your estate planning goals.

First, review the terms of your annuity contract. Understand any restrictions or fees associated with transferring ownership. Some annuities may impose penalties for such changes, impacting your decision.

Next, consult with legal and financial advisors. They can provide guidance on structuring the trust to meet your needs. Their expertise is invaluable in navigating the complexities of tax implications and legal documentation.

Once you have a clear plan, draft the necessary legal documents. These typically include amendments to your annuity contract and the trust deed. Completing these accurately is crucial to avoid future complications.

Here are the main steps summarized:

- Review the annuity contract.

- Consult advisors for guidance.

- Draft necessary legal documents.

Finally, ensure the trust is correctly established to manage the annuity. The trustee’s role is significant in overseeing payouts according to your wishes.

by Uran Wang (https://unsplash.com/@uranwang)

by Uran Wang (https://unsplash.com/@uranwang)

Legal and Financial Considerations

When transferring an annuity to a trust, understanding the legal and financial considerations is crucial. This complex process involves various factors that can impact your decision.

It’s essential to evaluate potential legal consequences. Changes in annuity ownership may involve legal requirements. Ensure compliance with all applicable laws to avoid complications.

Financial implications also play a significant role. Annuities transferred to trusts may face taxation or penalties. Consider the costs and benefits to determine the best course of action.

Consulting professionals is highly recommended. Legal advisors can assist with document preparation. Financial planners offer insights into how the transfer aligns with your financial strategy.

Key considerations include:

- Legal compliance requirements.

- Potential tax implications.

- Professional consultation for guidance.

Exploring these aspects ensures that your annuity transfer aligns with your financial and legal goals. This diligence helps protect your assets and secures a smooth transition.

Tax Implications of Transferring an Annuity to a Trust

Transferring an annuity to a trust can lead to various tax implications. Understanding these consequences is critical for effective estate planning.

When annuities are transferred, tax liabilities may arise. These taxes can impact the overall value of your financial assets. Certain transfers might result in capital gains tax if there’s a change in ownership.

Annuity gains are usually taxed as ordinary income. This means they are subject to higher tax rates than capital gains. It’s important to recognize these potential financial burdens.

Tax treatment can vary based on state laws. Be sure to investigate state-specific regulations that could affect your annuity transfer.

Considering these factors is vital. A misstep could increase your tax burden or alter the planned benefits of the transfer. Here’s what to keep in mind:

- Ordinary income tax on annuity gains.

- State-specific tax variations.

- Potential capital gains tax with ownership changes.

Seeking professional guidance can aid in navigating these complex issues. A tax advisor can offer tailored strategies for your circumstances.

by Jakub Żerdzicki (https://unsplash.com/@jakubzerdzicki)

by Jakub Żerdzicki (https://unsplash.com/@jakubzerdzicki)

Knowing the tax implications helps ensure that your financial goals are met while minimizing unnecessary costs. Planning with accuracy and clarity can greatly assist in managing your financial future.

Trust as Beneficiary of Annuity: Tax Consequences

Designating a trust as the beneficiary of an annuity can affect tax responsibilities. Trusts often face unique tax treatments, different from individuals.

Tax rules for trusts can be complex. They require careful analysis to understand potential implications. Unlike individual beneficiaries, trusts are taxed at different rates, often higher.

Income received by the trust may be subject to taxation. The trust itself could be responsible for paying taxes on annuity distributions. This might impact the net benefits received by beneficiaries.

There are benefits and downsides. Some trusts allow for the deferral of tax, providing time to strategize. Here are a few key considerations:

- Higher tax rates for trust income.

- Tax responsibilities could fall on the trust.

- Potential for deferred tax liability.

Consulting a tax professional is crucial for accurate planning. They can guide you through the specific rules and help optimize outcomes. Properly managing taxes can maximize the annuity’s benefits for all involved.

Annuity Ownership Change: Tax Consequences and Pitfalls

Changing the ownership of an annuity can bring unwanted tax consequences. It’s a process that needs careful consideration and planning. Tax liabilities may be triggered by seemingly simple ownership adjustments.

The Internal Revenue Service (IRS) may treat an ownership change as a taxable event. This could result in immediate taxation of any gains within the annuity. Even well-intentioned ownership changes can bring unexpected tax bills.

There are key pitfalls to avoid:

- Triggering taxable events unknowingly.

- Forgetting to account for surrender charges.

- Overlooking potential changes in future income stream.

It’s crucial to understand the terms of the annuity. Some contracts have specific clauses affecting ownership transitions. Before making any moves, consult with both legal and financial advisors. They can help navigate potential tax issues, saving time and money. Informed decisions can help maintain the annuity’s value for all parties involved.

Can You Transfer an Annuity to an Irrevocable Trust?

Transferring an annuity to an irrevocable trust is possible, but it involves complexities. Once placed in an irrevocable trust, control over the annuity is greatly limited. This act can provide strong asset protection but comes with trade-offs.

The main benefit of using an irrevocable trust is asset shielding from creditors. However, it also means you lose direct control and decision-making power. The decision to transfer should consider long-term financial implications and objectives.

Before proceeding, it’s vital to understand any possible tax consequences and restrictions from the annuity company. Awareness of these factors can protect against unforeseen complications. Here are key points to assess:

- Loss of control over assets.

- Potential tax consequences.

- Asset protection benefits.

Consulting with professional advisors can help you weigh the benefits and drawbacks. Legal guidance ensures compliance and understanding of all obligations.

Annuity vs Trust Fund: Key Differences and When to Use Each

Annuities and trust funds both offer financial planning solutions, but they serve different purposes. An annuity is a contract with an insurance company providing regular payments. It’s often used for retirement income.

Conversely, a trust fund can hold various assets, offering flexibility in managing wealth. Trusts can include real estate, cash, stocks, and more. They allow for controlled distribution according to specific wishes.

Choosing between an annuity and a trust fund depends on individual goals. Annuities offer the predictability of a steady income stream. In contrast, trust funds cater to those needing diverse asset management and distribution options.

Consider the following when choosing between an annuity and trust fund:

- Income needs and stability.

- Desired asset control.

- Long-term financial objectives.

Ultimately, the decision should align with personal financial strategies, risk tolerance, and estate planning ambitions. Seeking advice from a financial advisor can help clarify which option best fits your scenario.

Common Scenarios and Case Studies

Individuals often transfer annuities to trusts to achieve specific goals in estate planning. For instance, a parent may want to ensure a steady income for a child with special needs. Placing an annuity in a trust can secure that income.

Another scenario involves planning for Medicaid eligibility. Transferring an annuity to an irrevocable trust can help meet requirements while protecting assets. However, this needs careful consideration of timing and legal guidelines.

Consider these common uses for annuities in trusts:

- Providing for special needs family members.

- Planning for Medicaid and other eligibility.

- Managing financial assets for minors.

Each scenario presents unique challenges and benefits. Reviewing case studies and consulting professionals can provide insights into the best approach for your situation. Tailoring the trust structure to your specific needs can maximize benefits.

Frequently Asked Questions

Can you transfer an annuity to any type of trust?

Not all annuities can be transferred to any trust. Some annuities have restrictions that limit transfer options. Always check your contract terms.

What are some tax implications to consider?

Transferring an annuity can trigger taxes on accrued gains. It’s vital to assess the financial impact beforehand.

Is legal advice necessary for transferring an annuity to a trust?

Yes, involving legal professionals ensures compliance and optimizes benefits. They can guide you through complex legal requirements.

Some frequently asked questions include:

- Can I transfer an annuity without penalties?

- How do annuities in trusts affect probate?

- What documentation is needed for the transfer?

Exploring these questions provides clarity on common concerns. Addressing them thoroughly ensures informed decisions.

Final Thoughts: Is Transferring an Annuity to a Trust Right for You?

Transferring an annuity to a trust can be a smart move. It offers asset protection and estate planning advantages. But, every financial situation is unique.

Consider your long-term goals. Are you looking to secure income for your beneficiaries? Or perhaps you want to simplify estate settlement? A thorough evaluation of your financial landscape is vital.

Engaging with professional advisors is crucial. They can help navigate complex legal and financial considerations. With proper guidance, you can determine if this strategy aligns with your objectives. Ultimately, the decision should support your future and your family’s needs.