What Is a Fixed Annuity?

A fixed annuity is a contract with an insurance company that guarantees a set interest rate and protects your principal from market losses. Your money grows tax-deferred, and you can later turn the balance into income you cannot outlive. The insurer takes the market risk, not you, so your account value never drops because of a bad year on Wall Street.

“Fixed annuity” is a category, not a single product. Some fixed annuities grow a lump sum at a guaranteed rate; others convert savings into a lifetime paycheck; one type even links your interest to a market index while still protecting principal. Choosing the right type is the first decision, and this guide walks through all five.

Fixed annuity at a glance

- Principal is protected. You cannot lose money to a market downturn.

- Growth is tax-deferred. No 1099-INT every year, unlike a bank CD.

- Five main types. Traditional fixed, MYGA, fixed index (FIA), SPIA, and DIA.

- Backed by the insurer, plus your state guaranty association. Not FDIC insured.

- Top 5-year rates run about 5.00% to 5.65% today, roughly 0.50% to 0.75% above the best bank CDs.

The best fixed annuity for you is rarely the one with the single highest rate. Term length, surrender schedule, liquidity, and the insurer’s financial strength all matter as much as the headline number.

What Are Today’s Best Fixed Annuity Rates?

The table below shows the single highest fixed annuity (MYGA) rate available right now for each term, from 2 years to 10. Rates update daily from the carriers we work with.

| Term | Carrier | Product | Rate | AM Best | |

|---|---|---|---|---|---|

| 2-Year | CL Life | CL Sundance 2 | 5.15% | Get Quote | |

| 3-Year | Knighthead Life | Staysail 3 (Simple Interest) SI | 6.10% | Get Quote | |

| 4-Year | Oceanview Life and Annuity | Harbourview 4 | 5.60% | Get Quote | |

| 5-Year | Knighthead Life | Staysail 5 (Simple Interest) SI | 6.80% | Get Quote | |

| 6-Year | American Gulf | Anchor MYGA 6 | 6.00% | Get Quote | |

| 7-Year | Knighthead Life | Staysail 7 (Simple Interest) SI | 7.20% | Get Quote | |

| 8-Year | EquiTrust Life Insurance Company | Certainty Select 8 | 5.50% | Get Quote | |

| 9-Year | Royal Neighbors of America | MYGA 9 Year CA | 5.45% | Get Quote | |

| 10-Year | Revol One Financial | DirectGrowth 10 | 6.25% | Get Quote |

Rates subject to change without notice. Availability & features vary by state and insurer. Guarantees are backed by the claims‑paying ability of the issuing insurance company. Not a bank product. Not FDIC insured. State guaranty association limits apply (vary by state). Logos are property of their respective insurers; shown for educational platform availability only and do not imply endorsement.

Fixed annuity rates are tied to the broader interest rate environment. Insurers invest your premium mostly in bonds, so when Treasury yields rise, annuity rates rise with them. After bottoming near historic lows in 2021, rates climbed sharply and have held near 15-year highs for three years running. For savers who want guaranteed growth, this remains one of the most favorable windows in recent memory.

Because a fixed annuity locks your rate in for the full term, buying while rates are strong means you keep that yield even if rates fall later. Use our fixed annuity calculator to see what a given rate and term grow to, then compare current offers on our fixed annuity rates page.

Best Fixed Annuity Companies by 2025 Sales

A handful of carriers dominate the fixed annuity market. The ten below sold a combined $92.2 billion in 2025, roughly 56% of the record $165.3 billion fixed annuity market, according to LIMRA. Athene led for the third straight year, while New York Life and MassMutual carry the strongest financial-strength ratings.

| Rank | Company | 2025 Sales | Market Share | AM Best |

|---|---|---|---|---|

| 1 | Athene Annuity & Life | $17.55 billion | 10.62% | A (Excellent) |

| 2 | New York Life | $16.97 billion | 10.26% | A++ (Superior) |

| 3 | MassMutual | $12.21 billion | 7.39% | A++ (Superior) |

| 4 | Corebridge Financial | $10.49 billion | 6.35% | A (Excellent) |

| 5 | USAA Life | $7.63 billion | 4.61% | A++ (Superior) |

| 6 | Nationwide | $7.18 billion | 4.34% | A+ (Superior) |

| 7 | Pacific Life | $5.42 billion | 3.28% | A+ (Superior) |

| 8 | Western & Southern Group | $5.41 billion | 3.27% | A+ (Superior) |

| 9 | American National (ANICO) | $5.15 billion | 3.12% | A (Excellent) |

| 10 | Symetra Financial | $5.09 billion | 3.08% | A (Excellent) |

Sales figures reflect full-year 2025 fixed-rate deferred annuity (MYGA) sales reported by LIMRA. The other 44% of the market is spread across dozens of smaller carriers, many of which pay the highest rates at any given moment, which is why we compare 90+ top annuity companies, not just the household names. See our full best fixed annuity companies guide for ratings, reviews, and who each carrier is best for, or browse the complete annuity company directory.

Compare quotes from 90+ top annuity companies, or see what your money could grow to.

What Are the Types of Fixed Annuities?

There are five main types, split into two jobs: accumulation (growing money) and distribution (turning money into income).

| Type | Primary Job | How Interest Works | Rate Guarantee | Best For |

|---|---|---|---|---|

| Traditional fixed | Accumulation | Declared rate, resets yearly | Year 1, then annual renewals | Flexible savers adding money over time |

| MYGA | Accumulation | Fixed rate, locked | Full term (3 to 10 years) | CD-like savers who want rate certainty |

| Fixed index (FIA) | Accumulation | Linked to an index, 0% floor | Caps/rates reset annually | Growth seekers wanting downside protection |

| SPIA | Immediate income | Built into payments | Fixed payout for life or term | Retirees needing income now |

| DIA | Future income | Built into payments | Fixed once income starts | Pre-retirees planning future income |

Deferred fixed annuities (accumulation)

These grow your money at a guaranteed rate while you save. All three protect principal and grow tax-deferred.

Traditional fixed annuity. Guarantees a rate for an initial period, usually one to three years, then the carrier declares a new rate each year. Every contract has a guaranteed minimum interest rate the insurer can never go below. Many are flexible-premium, so you can add money over time.

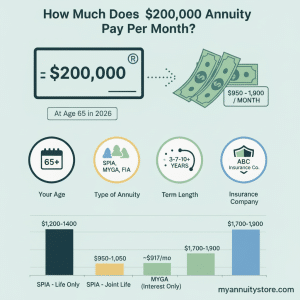

MYGA (multi-year guaranteed annuity). Locks one rate for a set term of 3, 5, 7, or 10 years. No changes during the term. It is the closest annuity to a bank CD, with higher rates and tax-deferred compounding, and it is the most popular fixed annuity sold today. See our complete MYGA guide.

Fixed index annuity (FIA). Credits interest based on a market index such as the S&P 500, with a 0% floor so you never lose principal to the market. Upside is capped by participation rates or spreads. In a strong year an FIA may credit 4% to 8%; in a down year you earn 0% rather than a loss. See our fixed index annuity guide.

Fixed income annuities (distribution)

These convert a lump sum into guaranteed income you cannot outlive.

SPIA (single premium immediate annuity). You hand the insurer a lump sum and income begins within 12 months, often within 30 days. Ideal for retirees who need predictable monthly income for essential expenses. The tradeoff: the decision is generally irrevocable. See our income annuity guide.

DIA (deferred income annuity). Works like a SPIA with a delayed start, anywhere from 2 to 40 years out. The longer you defer, the larger each payment. A DIA bought inside an IRA can be structured as a Qualified Longevity Annuity Contract (QLAC), letting you defer up to $200,000 of qualified money past the normal RMD age, as late as age 85, to reduce taxable required distributions in your early retirement years.

For a side-by-side look across every annuity category, see our types of annuities overview.

How Does a Fixed Annuity Work?

Every deferred fixed annuity moves through two phases.

- Accumulation. Your money grows at the guaranteed rate, locked in for the contract term, with no annual taxes on the interest.

- Payout. At the end of the term you can take a lump sum, renew with the same carrier, move the money tax-free to a better contract via a 1035 exchange, or annuitize for lifetime income.

Most fixed annuities pay compound interest, meaning you earn interest on your interest. A few pay simple interest, crediting only your original deposit. Compounding usually wins over the full term, but if you plan to withdraw your interest each year, a higher simple rate can pay more. Our simple vs compound interest calculator compares them side by side.

Single-premium vs flexible-premium

- Single-premium: funded with one lump sum. MYGAs, SPIAs, and DIAs are almost always single-premium. Natural fit if you are rolling over a CD, IRA, or 401(k).

- Flexible-premium: make an initial deposit and add more over time. Common on traditional fixed annuities. Better if you want to build savings gradually from income.

How Are Fixed Annuities Taxed?

Inside the contract, interest compounds tax-deferred. You owe tax only when you withdraw. How the money is taxed depends on how it was funded.

Non-qualified (after-tax money). You pay tax only on the earnings, not your original premium. Withdrawals from a deferred annuity come out earnings-first (LIFO) and are fully taxable until gains are exhausted. After annuitization, each income payment is split into a taxable earnings portion and a tax-free return of principal using the exclusion ratio. Withdrawing gains before age 59½ adds a 10% IRS penalty.

Qualified (IRA or 401(k) rollover). The entire withdrawal is taxable as ordinary income because the contribution was pre-tax. The tax deferral is redundant inside an IRA, so the reason to use a fixed annuity there is the guaranteed rate, principal protection, and lifetime income options. RMDs apply at age 73.

The tax-deferral advantage in dollars

Carol, age 58, rolls $150,000 from a maturing CD into a 5-year MYGA at 5.30% (24% federal bracket). In a taxable CD at the same rate, annual taxes drag her effective return down to about 4.03%, growing to roughly $183,100. In the MYGA, interest compounds untaxed to about $194,700, netting roughly $184,100 after she pays tax on the gains, and more if she spreads withdrawals across lower-bracket years.

Are Fixed Annuities Safe?

Fixed annuities are not FDIC insured because they are issued by insurance companies, not banks. They are protected by a different system with a strong track record.

- State guaranty association. Every state has one that steps in if an insurer fails, typically covering $100,000 to $500,000 per person, per carrier.

- Carrier financial strength. AM Best ratings are the standard. We recommend A- or better. For deposits above your state limit, splitting across two carriers from different parent companies is prudent.

No annuity holder at a top-rated carrier has lost guaranteed principal in modern U.S. insurance history. For a full breakdown, read our guide to whether annuities are safe.

Understanding Surrender Charges

Surrender charges are the tradeoff for the higher rates fixed annuities pay. The carrier guarantees your rate for the full term and expects the money to stay put. A typical 5-year schedule:

| Contract Year | Surrender Charge |

|---|---|

| Year 1 | 8% |

| Year 2 | 7% |

| Year 3 | 6% |

| Year 4 | 5% |

| Year 5 | 4% |

| After maturity | 0% |

Charges apply only to withdrawals above the annual free amount, usually 10% of account value. Take your 10% and nothing more and you never pay one. Most contracts also waive charges if you are confined to a nursing home or diagnosed with a terminal illness. See our guide to surrender charges for the full mechanics.

Fixed Annuity vs CD vs Bond

A fixed annuity (MYGA) is often compared to a bank CD because both guarantee a rate and protect principal. The differences are in rate, taxes, and flexibility.

| Feature | Fixed Annuity (MYGA) | Bank CD | Treasury Bond |

|---|---|---|---|

| Typical 5-year rate (2026) | 5.00% to 5.65% | 4.25% to 4.75% | ~4.40% |

| Principal protection | Yes (insurer backed) | Yes (FDIC up to $250K) | Yes (U.S. government) |

| Tax on interest | Deferred until withdrawal | Taxable every year | Federal taxable, state exempt |

| Convert to lifetime income | Yes | No | No |

| 1035 exchange available | Yes | No | No |

The MYGA rate edge over CDs is consistent, usually 0.50% to 0.75% on equal terms. The bigger story is flexibility and taxes: a CD matures and hands you cash and a tax bill; a fixed annuity lets you withdraw, renew, exchange into an income product, or start lifetime payments, often with no taxable event. See our full fixed annuity vs CD comparison.

Who Should Buy a Fixed Annuity?

A fixed annuity tends to fit if you:

- Cannot afford to lose principal within 5 to 10 years of retirement.

- Hold a maturing CD and want a higher guaranteed rate with tax deferral.

- Need guaranteed income a SPIA or DIA can provide for life.

- Are in a higher tax bracket and want to control when you pay taxes.

- Have more than $250,000 at one bank and want to diversify beyond the FDIC limit.

It is a poorer fit if you may need the full balance before maturity, are decades from retirement with a high risk tolerance, or would be tying up your only liquid savings. Keep 6 to 12 months of expenses liquid first.

How to Buy a Fixed Annuity

The process takes about 15 to 30 minutes:

- Compare live rates for the term that matches when you will need the money.

- Check the carrier’s ratings (AM Best, S&P, Moody’s). Aim for A- or better.

- Complete the application, usually by e-application with ID and beneficiary info.

- Fund the contract from a bank, another annuity (1035 exchange), or an IRA rollover.

- Use your free-look period, 10 to 30 days to review the issued contract and cancel penalty-free.

My Annuity Store works with 90+ top annuity companies and charges no fee for our service. You work directly with a licensed agent, never a call center. Our guide to buying an annuity walks through each step.

Fixed Annuity FAQ

What is the difference between a fixed annuity and a MYGA?

Is a fixed index annuity a type of fixed annuity?

Can I lose money in a fixed annuity?

How much does a $100,000 fixed annuity earn?

Can I put a fixed annuity inside my IRA?

What happens to a fixed annuity when you die?

What happens if the insurance company fails?

Sources

- Internal Revenue Service. Publication 575: Pension and Annuity Income. Tax rules for annuity distributions, the exclusion ratio, and early-withdrawal penalties.

- U.S. Federal Register. Required Minimum Distributions, Final Rule (2024). Finalized SECURE 2.0 rules, including the $200,000 QLAC limit.

- National Organization of Life and Health Insurance Guaranty Associations. NOLHGA.com. State guaranty-association coverage limits and policyholder protections.

- AM Best. Understanding Best’s Credit Ratings. The rating scale used to gauge insurer financial strength.

- LIMRA. Individual Annuity Sales Results. Industry sales data by product type, including record MYGA sales.

- National Association of Insurance Commissioners. NAIC Annuity Resources. Consumer guidance on annuity regulation and state oversight.

Keep Reading

- MYGA Guide: rates, terms, carriers, and how to buy.

- Today’s Fixed Annuity Rates: live rates across all terms, updated daily.

- Fixed Index Annuity Guide: crediting methods, caps, and who they fit.

- Fixed Annuity Calculator: model your amount, term, and rate.

- Income Annuities | Fixed Annuity vs CD | Types of Annuities | Annuity Fees & Commissions

Ready to lock in a guaranteed rate? Compare quotes from 90+ top annuity companies, or run your numbers first.

My Annuity Store independently researches annuity products. We may earn a commission when you purchase through our licensed agents, at no cost to you. Information here is educational and not individualized tax or investment advice.

Pros and Cons

Pros

- Guaranteed interest rate locked for full term

- Principal is 100% protected from market losses

- Tax-deferred growth (no taxes until withdrawal)

- No contribution limits on non-qualified contracts

- Bypasses probate - passes directly to beneficiaries

- Option to convert to guaranteed lifetime income

- Simple to understand compared to other annuity types

- Rates currently near decade-plus highs (2026)

Cons

- Limited liquidity - surrender charges for early withdrawal

- Not FDIC insured (backed by state guaranty associations)

- Inflation risk - fixed rate may lag rising costs over time

- 10% IRS penalty on earnings withdrawn before age 59½

- Opportunity cost vs. higher-return investments like equities