What Is an Income Annuity and How Does It Turn Savings Into Guaranteed Income?

An income annuity is a contract with an insurance company that converts a lump sum of savings into a stream of guaranteed payments, either for life, a fixed period, or both. Unlike a savings account or investment portfolio, the income cannot run out. The insurance company is legally obligated to pay you for as long as the contract specifies, regardless of how long you live or what happens in financial markets.

There are four main types: the Single Premium Immediate Annuity (SPIA), the Deferred Income Annuity (DIA), the Fixed Index Annuity with a Guaranteed Lifetime Withdrawal Benefit rider (FIA/GLWB), and the Qualified Longevity Annuity Contract (QLAC). Each one solves a slightly different retirement income problem. This guide explains how each works, who benefits from each, and how to compare them before buying.

The Four Types of Income Annuities at a Glance

| Type | When Income Starts | Access to Principal? | Best For |

|---|---|---|---|

| SPIA | Within 30 days | No (irrevocable) | Replacing a paycheck; immediate income floor |

| DIA | 2 to 40 years later | No (irrevocable) | Locking in future income at today’s rates; longevity insurance |

| FIA with GLWB | When you choose (typically 5-15 years) | Yes (subject to surrender charges) | Growth phase plus guaranteed income; flexibility before income starts |

| QLAC | Up to age 85 | No (irrevocable) | Reducing RMDs; insuring against outliving savings in late retirement |

Single Premium Immediate Annuity (SPIA)

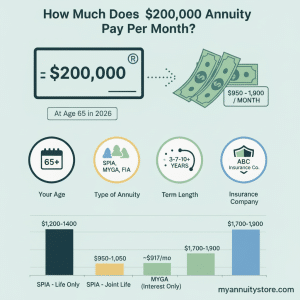

A SPIA is the simplest income annuity. You deposit a lump sum, typically $50,000 to $500,000, and payments begin within 30 days. The insurance company calculates your monthly payment based on your age, gender, the payout option you select, and prevailing interest rates. Once set, the payment amount never changes unless you add an inflation rider.

How Much Does a SPIA Pay?

Payouts depend primarily on age and current interest rates. As a general range based on today’s market:

- A 65-year-old man depositing $200,000 into a life-only SPIA can expect roughly $1,300-$1,500 per month.

- A 65-year-old woman on the same deposit receives approximately $1,100-$1,300 per month. Women have longer life expectancies, so the carrier pays less per month to account for a longer payment period.

- At age 70, those same deposits produce roughly 15-20% more income per month.

- At age 75, payouts are roughly 30-40% higher than at 65.

Use our immediate annuity income calculator to get a personalized estimate based on your age, gender, and deposit amount.

The Mortality Credit Advantage

SPIAs consistently pay more income per dollar than safe alternatives like bond ladders or CDs. The reason is the mortality credit. When thousands of people pool their money with an insurer, those who die early effectively subsidize the payments of those who live longer. A 70-year-old who buys a life-only SPIA and dies at 72 has received far less than she deposited. Her remaining principal stays with the carrier and helps fund payments to policyholders who live to 95. This pooling of longevity risk is why a SPIA can generate $1,400 per month from $200,000 when a bond paying 5% would generate only about $833 per month.

Who Should Buy a SPIA?

SPIAs work best for retirees who need income now, do not prioritize leaving the purchase amount to heirs, and want the simplicity of a fixed monthly payment they cannot outlive. The ideal buyer is someone whose fixed monthly expenses exceed what Social Security and any pension provide. The SPIA bridges that gap permanently.

Deferred Income Annuity (DIA)

A DIA works like a SPIA except income starts in the future. Income can begin anywhere from 2 to 40 years after purchase. You pay a premium today and lock in a future income amount. Because the insurance company holds your money longer, a given deposit buys significantly more future income than the same deposit into a SPIA starting immediately.

Example

Carol is 60 years old and retiring at 65. She deposits $100,000 into a DIA today with income starting at age 65. Because the carrier will hold the funds for 5 years, the same $100,000 might generate $900-$1,000 per month starting at 65, compared to perhaps $640-$700 per month if she bought a SPIA right now at age 60. The 5-year deferral substantially increases the payout.

If she deferred to age 70 instead, the same $100,000 might generate $1,400-$1,600 per month, because the carrier holds the money for 10 years before the first payment.

The Rate Lock Advantage

DIAs allow you to lock in today’s interest rates for future income. If you believe rates will fall over the next several years, buying a DIA now secures current yields for income that starts later. This is a meaningful planning tool in a rate environment where the trajectory is downward.

Who Should Buy a DIA?

DIAs suit people who are still working or who have enough near-term income from Social Security and other sources but want to guarantee income starting at a specific future date. They are also used as bridge income for people who want to delay claiming Social Security to maximize their benefit. A retiree at 62 might buy a DIA with income starting at 70, use other savings for the interim years, then receive maximized Social Security plus DIA income from 70 onward.

Fixed Index Annuity with a Guaranteed Lifetime Withdrawal Benefit (FIA/GLWB)

A Fixed Index Annuity with a GLWB rider is the most flexible of the income annuity types. It combines a growth phase with a guaranteed income phase, and keeps the principal accessible during the deferral period.

How the Two-Phase Structure Works

During the accumulation phase, typically 5-15 years, your premium earns interest linked to a stock market index like the S&P 500, with a 0% floor so you cannot lose principal due to market losses. Many contracts also credit a separate “income account” or “benefit base” at a guaranteed rollup rate, commonly 5-8% per year. This benefit base is used only to calculate future income, not the account value you can withdraw as a lump sum.

During the income phase, you activate the rider and begin receiving a guaranteed lifetime withdrawal. The withdrawal amount is typically a percentage of the benefit base, and that percentage increases with age. The older you are when you start income, the higher the payout rate the carrier offers.

Example

Robert, age 58, deposits $200,000 into an FIA with a GLWB rider offering a 6% annual rollup on the benefit base. After 10 years, his income account has grown to approximately $358,000. At age 68, the carrier’s payout rate is 5.5% of the benefit base. His guaranteed annual income is $358,000 x 5.5% = $19,690, or about $1,641 per month, for life, regardless of what happens to the contract’s actual account value. If markets perform well, his actual account value may be higher, giving him the option to take lump-sum withdrawals on top of the guaranteed income.

The Key Difference from a SPIA

Unlike a SPIA, Robert still has access to his account value during the accumulation phase, subject to surrender charges in early years. If he needs emergency funds in year 3, he can take a partial withdrawal. This flexibility comes at a cost: the income per dollar is typically lower than what a SPIA purchased at the same age would pay, because the carrier is taking on both the growth-phase costs and the lifetime income guarantee.

Read our full guide to GLWB income riders for detailed comparisons across carriers.

Who Should Buy an FIA with GLWB?

The FIA/GLWB structure suits people who are 5-15 years from retirement, want to grow their savings during that period, and want a guaranteed income floor starting later, while also keeping the option to access principal if needed. It is also a strong choice for people who are uncomfortable with the irrevocable commitment that a SPIA or DIA requires.

Qualified Longevity Annuity Contract (QLAC)

A QLAC is a specialized DIA funded with qualified retirement funds from a traditional IRA, 401k, or similar account. Congress created the QLAC specifically to allow retirees to use pre-tax retirement money to purchase guaranteed late-life income without being forced to take required minimum distributions on that portion of their IRA balance. Read the full QLAC guide for more detail.

QLAC Rules (2026)

- Maximum premium: $200,000 lifetime limit across all qualified accounts.

- Maximum income start date: Age 85.

- RMD exclusion: The QLAC premium is excluded from the IRA balance used to calculate RMDs. On a $1,000,000 IRA, moving $200,000 into a QLAC reduces the RMD base to $800,000.

- Income taxation: All QLAC payments are fully taxable as ordinary income, since the money was never taxed going in.

Example

Margaret is 72 with a $900,000 traditional IRA generating RMDs she does not need. She purchases a $200,000 QLAC with income starting at age 85. Her current RMD base drops to $700,000, reducing her annual RMD by roughly $5,000-$7,000 per year and the associated tax bill for over a decade. At 85, she begins receiving guaranteed monthly income, insurance against an era of retirement when other savings may be depleted and healthcare costs are often highest.

Who Should Buy a QLAC?

QLACs are best for retirees in their 70s who have substantial IRA assets, do not need their full RMD for living expenses, and want to protect against the financial risk of living past age 85. The QLAC does double duty: it reduces the current tax burden from unwanted RMDs and creates a guaranteed income floor in the final decades of retirement.

How Annuitization Works

Annuitization is the process of converting a deferred annuity’s accumulated value into a guaranteed stream of income payments. It is the mechanism behind SPIAs and DIAs, and it is also available as an option on most deferred annuities once the surrender period has ended.

When you annuitize, you give up access to the lump sum in exchange for guaranteed lifetime income. The insurance company uses the accumulated value, your age, and the payout option you select to calculate a fixed payment. The exclusion ratio then determines how much of each payment is taxable and how much is a tax-free return of your cost basis.

Annuitization is irrevocable in most cases. Once payments begin, you cannot reverse the decision or access the remaining principal. This is why many people prefer the GLWB rider approach on an FIA. It delivers guaranteed lifetime income without requiring full annuitization, preserving some access to the account value.

Single Life vs. Joint Life Payouts

Every income annuity requires you to choose between a single life payout and a joint life payout. This decision is irreversible once income begins and has a significant impact on both the monthly payment amount and the financial security of a surviving spouse.

Single Life

Payments continue for one person’s lifetime and stop at death. This option always pays the most income per month because the insurance company’s risk ends when you die. It is appropriate when the annuity owner has no spouse, when the surviving spouse has ample other income sources, or when the couple has deliberately decided to use other assets for the survivor.

Joint Life

Payments continue over two lifetimes, typically a married couple. When the first person dies, the surviving spouse continues receiving payments. The percentage that continues can be 100%, 75%, or 50% of the original payment:

- 100% joint survivor: Survivor receives the full original payment. Reduces initial monthly income by 8-15% compared to single life, depending on both ages.

- 75% joint survivor: Survivor receives 75% of the original payment. Moderate income reduction of 5-10%.

- 50% joint survivor: Survivor receives half the original payment. Smallest reduction, typically 3-7%.

The right choice depends on the surviving spouse’s other income sources. If Social Security, a pension, or other investments would adequately support the survivor, a 50% survivor payout may be appropriate, and the higher initial income funds a better retirement for both while both are living. If the survivor would struggle without the full annuity income, a 100% joint survivor payout provides the most protection.

Income Annuity Payout Options Explained

Beyond single vs. joint life, you choose a payout structure that determines what happens if you die early.

Life Only

The highest monthly payment. Stops at death with no benefit to heirs. Best when maximizing income is the priority and legacy is handled through other assets.

Life with Period Certain

Payments continue for your life, but if you die before the guarantee period ends (10 or 20 years are most common), payments continue to your named beneficiary for the remainder of that period. The income reduction vs. life only is modest, typically 2-5%. This is the most popular option for buyers who want downside protection without sacrificing much income.

Life with Cash Refund

If you die before receiving total payments equal to your original deposit, the insurance company pays the difference to your beneficiary in a lump sum. This eliminates the fear of losing principal on an early death. Typical income reduction of 3-8% vs. life only.

Life with Installment Refund

Same protection as cash refund, but the remaining principal is paid as continued monthly payments rather than a lump sum. Often produces slightly more monthly income than cash refund because the carrier retains use of the money a bit longer.

Period Certain Only

Payments for a fixed term regardless of survival, typically 10, 15, or 20 years. If you die during the term, payments continue to your beneficiary for the remainder. This option is used for specific income-planning purposes, like bridging to Social Security, and is not a lifetime income strategy.

Income Annuity vs. Bond Ladder vs. 4% Rule

| Strategy | Guaranteed for Life? | Inflation Protection? | Principal Access? | Approx. Monthly Income on $300k |

|---|---|---|---|---|

| SPIA, life only, age 68 | Yes | Optional rider | No | $2,100-$2,400 |

| Bond ladder, 20-year, 5% yield | No (runs out) | TIPS bonds only | Yes | $1,250-$1,400 |

| 4% rule, balanced portfolio | No (sequence risk) | Yes (equities) | Yes | $1,000 ($12,000/year) |

| FIA with GLWB, activated at 68 | Yes | Limited (via index) | Yes (account value) | $1,600-$1,900 |

The income annuity advantage is largest for older buyers and those most concerned about longevity. A bond ladder or 4% rule can run out of money. An income annuity cannot. For retirees who already have Social Security covering essential expenses, the flexibility and growth potential of a portfolio may be preferred. For those who need guaranteed income to cover non-negotiable monthly expenses, an income annuity is the most dependable tool available.

Tax Treatment of Income Annuity Payments

How your income annuity payments are taxed depends on how you funded it.

Non-Qualified Money (After-Tax Savings)

If you funded the annuity with savings from a bank account, brokerage, or CD, you already paid income taxes on that money. The IRS uses the exclusion ratio to split each payment between a tax-free return of your investment and taxable earnings. A 68-year-old with a $200,000 SPIA might find that 65-75% of each payment is tax-free. Only the earnings portion is taxable as ordinary income. See our exclusion ratio guide for a detailed walkthrough with examples.

Qualified Money (Pre-Tax IRA, 401k, or 403b)

If you funded the annuity through a rollover from a traditional IRA or 401k, 100% of every payment is taxable as ordinary income. Your cost basis is $0 because you received a tax deduction when the money went in. There is no exclusion ratio advantage on qualified money.

What to Look for When Comparing Income Annuities

- Carrier financial strength. Your income depends on the carrier’s ability to pay for decades. Stick with insurers rated A- or better by AM Best. Higher ratings indicate a lower probability of insolvency.

- Payout rate. For SPIAs and DIAs, compare the monthly income per $100,000 deposited across at least 3-5 carriers. Differences of 5-10% are common. On a $300,000 purchase, a 7% payout difference is $150+ per month, or $36,000 over 20 years.

- Rollup rate and payout percentage (GLWB). For FIA income riders, evaluate the rollup rate during deferral and the payout percentage at your anticipated activation age. A 7% rollup with a 5% payout rate at 68 may produce more or less income than a 6% rollup with a 5.5% payout rate, depending on your deferral period.

- Surrender charges (FIA). FIAs typically have surrender periods of 5-10 years. Withdrawals exceeding the free withdrawal amount during this period incur a surrender charge. Make sure the contract aligns with your timeline.

- State guaranty association limits. Each state protects policyholders up to a limit, typically $250,000, if the carrier fails. If your purchase exceeds that limit, consider spreading across two or more A-rated carriers.

Frequently Asked Questions

What is the difference between a SPIA and a DIA?

A SPIA starts paying income within 30 days of purchase. A DIA defers income to a future date, anywhere from 2 to 40 years. Because the carrier holds DIA funds longer before paying, the same deposit buys significantly more future income. Both are irrevocable once purchased.

Can I get inflation protection on an income annuity?

Yes. Most carriers offer cost-of-living adjustment riders that increase payments by 1-3% per year. The trade-off: initial payments start 20-35% lower than a flat-payment annuity, and it takes 8-12 years for the difference to close. For buyers already receiving Social Security, which has CPI adjustments, a flat SPIA covering fixed expenses may provide sufficient inflation coverage without the rider’s income reduction.

Can I lose money in an income annuity?

On a life-only SPIA or DIA, yes, if you die early. The carrier retains any remaining principal beyond payments already made. On a period certain or refund option contract, your beneficiary receives the unpaid balance. For FIAs with a GLWB, your actual account value is accessible subject to surrender charges, so the main scenario of financial loss is a large surrender in the early years. The real risk of a life-only annuity is dying early. The benefit is living longer than expected.

How does an income rider differ from annuitization?

Annuitization is a one-way door. You surrender the lump sum and receive payments, with no going back. A GLWB income rider on an FIA lets you receive guaranteed lifetime income while keeping the actual account value accessible, subject to surrender charges. With a GLWB rider, you own the account value and activate the income stream separately. The trade-off: income riders typically pay less per dollar than full annuitization at the same age.

What happens to my income annuity when I die?

It depends on the payout option. Life only: payments stop immediately, nothing to heirs. Period certain: remaining payments continue to your beneficiary. Cash or installment refund: beneficiary receives any unpaid principal. Joint life: surviving spouse continues receiving payments at the agreed percentage. Always name a beneficiary at purchase and review it whenever your family situation changes.

Are income annuity payments safe if the insurance company fails?

Payments are not federally insured like bank deposits. Every state has a guaranty association that steps in if an insurer fails, with coverage typically up to $250,000 per policyholder per company. Choosing A-rated carriers and staying within guaranty limits significantly reduces this risk. You can look up your state’s specific limits at the National Organization of Life and Health Insurance Guaranty Associations (NOLHGA).

Related Resources

- Single Premium Immediate Annuity (SPIA) Guide

- GLWB Income Rider Guide

- Qualified Longevity Annuity Contract (QLAC) Guide

- Income Annuity Calculator

- How Income Annuity Payments Are Taxed

- Get a Free Income Annuity Quote

Sources

- IRS Publication 575 — Pension and Annuity Income

- IRS — Qualified Longevity Annuity Contracts (QLAC)

- National Association of Insurance Commissioners — Annuity Buyer’s Guide

- National Organization of Life and Health Insurance Guaranty Associations (NOLHGA)

- Society of Actuaries — RP-2014 Mortality Tables