Income Annuities

Turn savings into a dependable paycheck you can’t outlive. Start now (SPIA) or later (DIA)—with options for spouse and beneficiaries.

Get an Income Annuity QuoteCompare today’s annuity options and find the right fit for your retirement—lifetime income, guaranteed growth, or index-linked potential with principal protection.

Turn savings into a dependable paycheck you can’t outlive. Start now (SPIA) or later (DIA)—with options for spouse and beneficiaries.

Get an Income Annuity QuotePrefer a safe, steady path? Fixed annuities lock in a guaranteed interest rate so your money grows predictably without market risk.

See Fixed RatesSeek more upside while protecting your principal. Index-linked growth with a 0% floor and optional income riders.

Indexed Annuity RatesGuaranteed lifetime income designed to cover essentials and reduce sequence-of-returns risk. Choose single or joint life, with options for period certain or cash refund.

Quick ballpark estimate of lifetime income from a single-premium immediate annuity (SPIA). Actual quotes vary by carrier, rate date, and state.

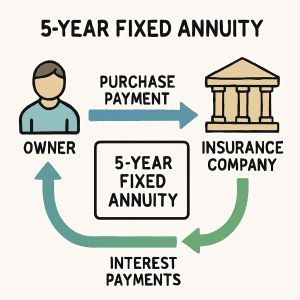

Lock in a guaranteed rate for 2–10 years. No market risk, predictable growth, and optional liquidity via free withdrawals.

Participate in index-linked growth with a 0% downside floor. Pick among caps, participation rates, or spreads, and add income riders if desired.

No-pressure guidance to compare annuity rates and make a confident decision.

Prefer email? Reach us at info@myannuitystore.com.

A quick checklist to evaluate annuity rates beyond the headline number.

Both offer guaranteed interest. The right choice depends on taxes, time horizon, and liquidity needs.

Rule of thumb: If you’re in a higher tax bracket and can commit for 3–7 years, MYGA annuity rates often compare favorably after taxes. For short-term liquidity, CDs may be more convenient.

What could drive annuity rates over the next 12 months?

Quick answers to the most common questions we get from clients.

Fixed annuity (MYGA) rates can change weekly. FIA crediting terms typically update monthly or quarterly. Income annuity payouts depend on interest rates and age, and are quote-specific at the time you apply.

They offer principal protection and guaranteed interest backed by the insurer’s claims-paying ability. State guaranty associations provide additional protection subject to limits. Review company strength ratings before you buy.

MYGAs generally have no explicit annual fees. FIAs may have optional rider fees. Income annuities build costs into the payout structure—there’s no separate annual fee. Surrender charges apply if you exit early.

Interest grows tax-deferred. Withdrawals are taxed as ordinary income. Non-qualified contracts use LIFO for gains. Consult your tax advisor for your specific situation.

Answer a few short questions and we'll guide you to the annuities that best meet your goals.

How much are you looking to invest?

Your comfort level helps determine the right product

Understanding your priorities helps us match you perfectly

Based on your answers, here's the best annuity type for you

Tip: Check spam/promotions if you don’t see our email on time.

Need help sooner or have a quick question?

What happens next

Tip: Check your spam or promotions folder if you don’t see our email within the time window.