The Athene Agility 10 is one of the best-selling fixed index annuities in the U.S. — and it’s easy to see why. It pairs competitive crediting rates across multiple index strategies with a built-in income rider at no additional cost, a 20% premium bonus to the income benefit base, and 175% annual interest crediting to that base. For someone aged 50-70 looking for both accumulation and future income, it checks a lot of boxes.

But a 10-year surrender period is a serious commitment, and the product isn’t available in New York. Here’s our full breakdown of how the Athene Agility 10 works, who it’s best for, and where it falls short.

Athene Agility 10 at a Glance

| Feature | Details |

|---|---|

| Product Type | Fixed Index Annuity (FIA) |

| Carrier | Athene Annuity and Life Insurance Company |

| Surrender Period | 10 years |

| Issue Ages | 40–80 |

| Minimum Premium | $10,000 ($5,000 in AK, HI, MN, MO, NJ, OR, PA, TX, UT, WA) |

| Maximum Premium | $1,000,000 (higher with home office approval) |

| Annual Fees | None |

| Income Rider | Built-in at no charge (20% bonus + 175% interest crediting to benefit base) |

| AM Best Rating | A (Excellent) |

| Qualified Funds | IRA, IRA Rollover, 401(k), 403(b), Profit Sharing, Non-Qualified, 1035 Exchange |

| State Availability | All states except New York |

Is Athene a Good Annuity Company?

Athene Annuity and Life Insurance Company is one of the largest annuity issuers in the United States. They carry an A (Excellent) rating from AM Best and have consistently ranked among the top sellers of fixed index annuities for several years running.

An annuity’s guarantees are backed by the financial strength of the issuing carrier — not the federal government and not FDIC insurance. So the carrier’s rating matters. Athene’s A rating and massive scale in the annuity market put them firmly in the “strong carrier” category. For a full breakdown of their ratings, product lineup, and company history, see our Athene Annuity Review.

Index Crediting Strategies and Rates

The Athene Agility 10 offers a strong lineup of crediting strategies across multiple indexes. Each strategy uses an annual or biennial point-to-point measurement, meaning performance is measured from one contract anniversary to the next (or over two years for biennial options).

Available Index Options

| Index | Crediting Methods |

|---|---|

| BNP Paribas Multi-Asset Diversified 5 | 1-Year PTP (Participation Rate) · 2-Year PTP (Participation Rate) |

| Nasdaq FC Index (BOFANFCC) | 1-Year PTP (Participation Rate) · 2-Year PTP (Participation Rate) |

| AI Powered US Equity Index | 1-Year PTP (Participation Rate) · 2-Year PTP (Participation Rate) |

| S&P 500 | 1-Year PTP (Cap) · 2-Year PTP (Cap) |

| Fixed Account | Declared fixed interest rate |

The volatility-controlled indexes (BNP Paribas, Nasdaq FC, AI Powered) use participation rates with no cap, meaning you receive a percentage of the total index gain with no ceiling. The S&P 500 strategy uses a cap, which limits the maximum credit you can earn in a given year.

You can split your premium across multiple strategies — and most advisors recommend diversifying across 2-3 indexes rather than concentrating in one. For more on how these crediting methods work, see our FIA cap rates and participation rates page.

Built-In Income Rider (No Additional Cost)

One of the Agility 10’s biggest selling points is its lifetime income rider (GLWB) — included at no extra charge. Many competing annuities charge 0.95% to 1.25% annually for a similar rider, so this is a meaningful cost advantage.

How the Income Rider Works

- 20% Initial Bonus: On day one, your income benefit base is set to 120% of your premium. Put in $100,000 and your benefit base starts at $120,000.

- 175% Annual Interest Crediting: Each year, the benefit base receives 175% of whatever interest is credited to your account value. If your account earns $3,000 in interest, your benefit base grows by $5,250.

- Income continues even after account depletes: Once you turn on lifetime income, Athene guarantees payments for life — even if your account value drops to zero.

- Benefit base continues growing during income phase: Even while you’re receiving income payments, the 175% interest credit continues being applied to the benefit base, which can increase your income over time.

Enhanced Benefits

Enhanced Income Benefit: If the annuitant is confined to a Qualified Care Facility for 180 out of the last 250 days, the lifetime income withdrawal amount doubles — as long as the account value is greater than zero. This isn’t full long-term care coverage, but it provides meaningful additional income if you need extended care. Not available in all states.

Enhanced Death Benefit: The benefit base (not just the account value) is paid out to beneficiaries in equal payments over the currently declared Death Benefit Payout Period (currently 5 years, guaranteed not to exceed 10 years). In AK, HI, NJ, PA, and WA, the enhanced death benefit is capped at 125% of cash surrender value or 250% of net premium.

Hypothetical Income Illustration

To show how the income rider works in practice, here’s a hypothetical scenario: a 55-year-old puts $100,000 into the Athene Agility 10, splits the premium across the 2-Year Nasdaq FC (62% participation) and 2-Year BNP Paribas Multi-Asset (90% participation), and defers income for 10 years.

| Age | Annual Payment | Account Value | Interest | Income Base |

|---|---|---|---|---|

| 65–66 | $12,381 | $162,061 | 0% | $237,156 |

| 68–69 | $13,233 | $159,576 | 19.96% | $182,697 |

| 70–71 | $15,874 | $131,314 | 2.7% | $146,349 |

This is a hypothetical illustration using current participation rates applied to historical index performance. Actual results will vary. Interest shown is based on the most recent 10-year period of actual index data, then repeated. This is not a guarantee of future performance.

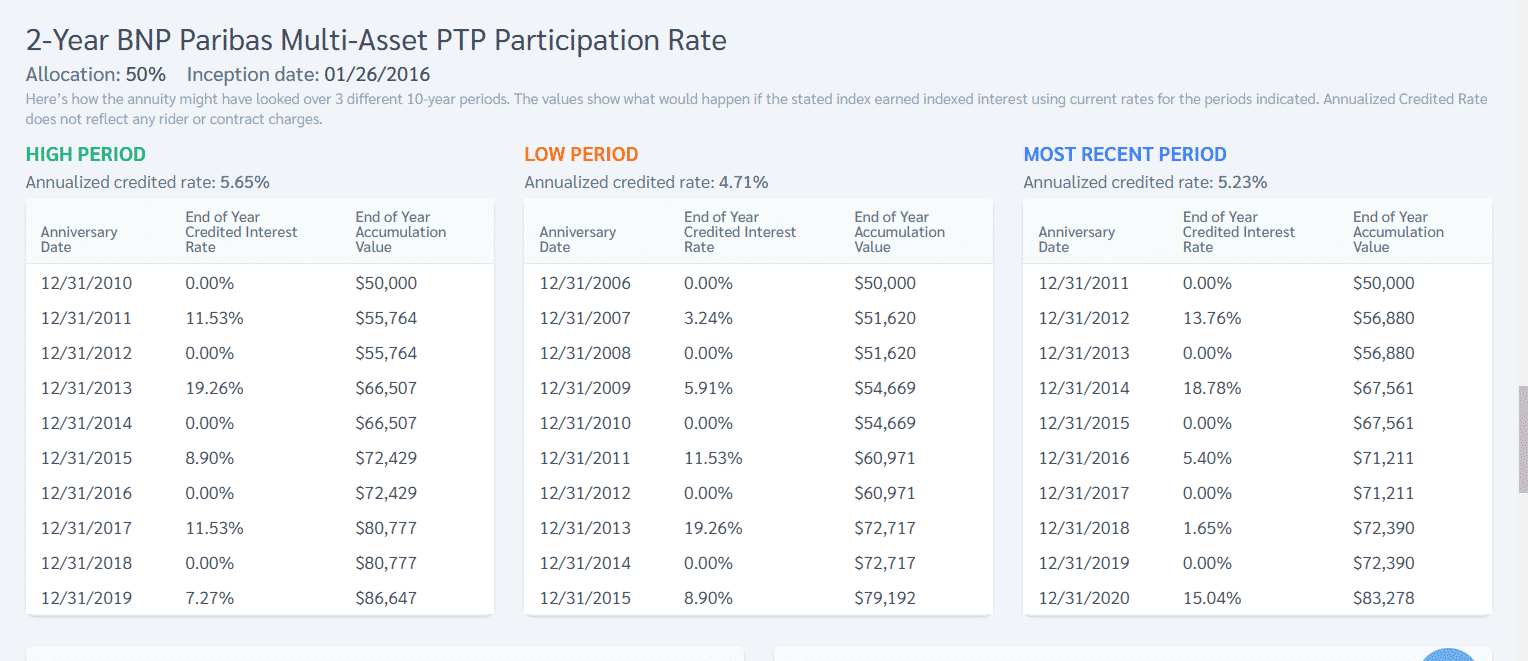

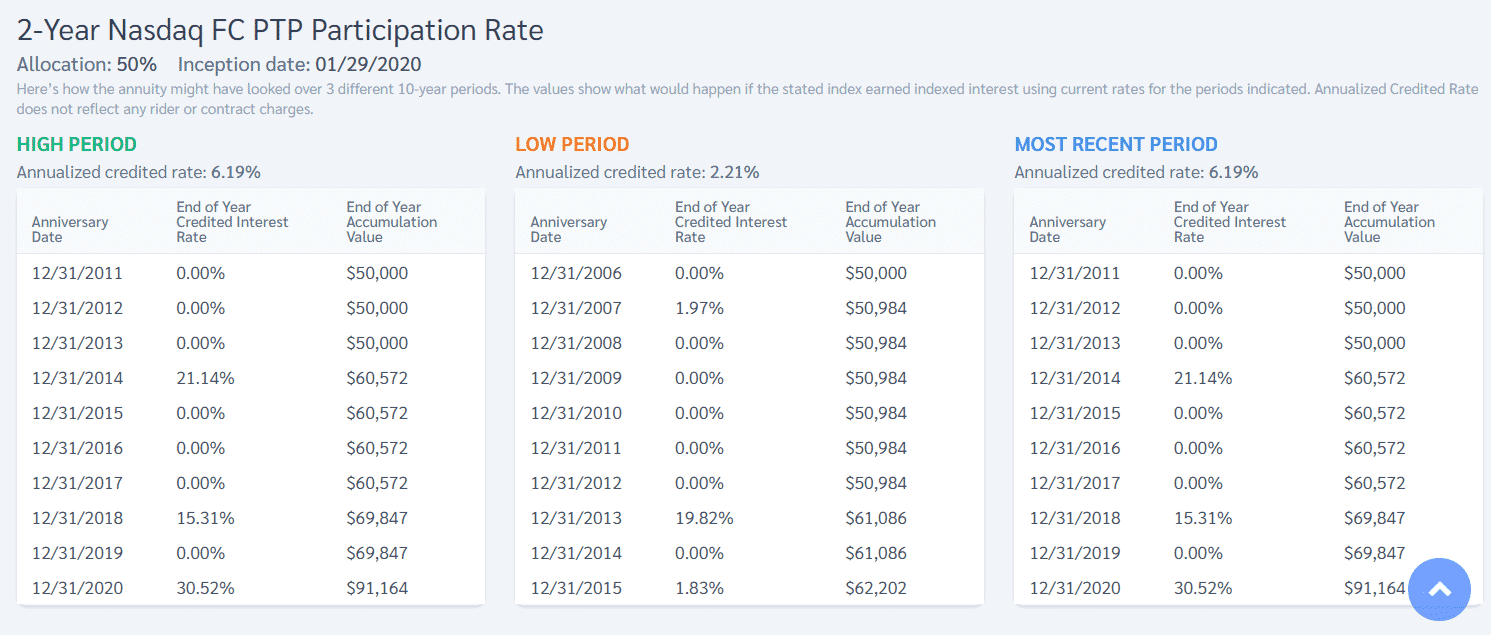

Historical Performance by Index Strategy

The charts below show hypothetical 10-year backtested returns for a $50,000 allocation inside the Athene Agility 10 using two of its most popular crediting strategies.

2-Year BNP Paribas Multi-Asset PTP (90% Participation)

- 5.23% annualized for the most recent 10-year period

- 5.65% annualized for the highest 10-year period

- 4.71% annualized for the lowest 10-year period

2-Year Nasdaq FC PTP (62% Participation)

- 6.19% annualized for the most recent 10-year period

- 6.19% annualized for the highest 10-year period

- 2.21% annualized for the lowest 10-year period

All backtested performance is hypothetical and based on current participation rates/caps applied retroactively. The annuity was not available during the full period shown. Past results do not guarantee future performance.

Surrender Charge Schedule

The Agility 10 has a 10-year declining surrender charge schedule. This is longer than average — most FIAs have 7-year terms — so make sure you’re comfortable with the commitment before buying.

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | Year 7 | Year 8 | Year 9 | Year 10 |

|---|---|---|---|---|---|---|---|---|---|

| 9% | 9% | 8% | 7% | 6% | 5% | 4% | 3% | 2% | 1% |

After year 10, there are no surrender charges. You also get penalty-free access to a portion of your account value each year (typically 10% of the accumulated value) without triggering surrender charges.

Liquidity Waivers

Athene includes two built-in waivers that can give you full access to your account value without surrender charges:

- Terminal Illness Waiver: Available after the first contract anniversary if the annuitant is diagnosed with a terminal illness expected to result in death within one year

- Confinement Waiver: Available after the first contract year if the annuitant is confined to a qualified care facility for 60+ consecutive days

There’s also a Bail-Out provision: if Athene lowers the declared 1-Year S&P 500 PTP Cap Rate below your Bailout Cap Rate, you get full access to your accumulated value free of surrender charges for up to 30 days.

Athene Agility 10 Pros and Cons

Pros

- Free income rider — the built-in GLWB with 20% bonus and 175% interest credit saves 0.95%–1.25% annually compared to competitors that charge for riders

- Multiple index strategies — five different options including both equity-only and volatility-controlled indexes give you real diversification

- No annual fees — zero cost means 100% of your premium goes to work from day one

- Strong carrier — Athene’s A rating from AM Best and position as a top-3 FIA seller provide confidence in the guarantees

- Enhanced care and death benefits — built-in waivers and doubled income for qualifying care needs add real value at no extra cost

- Bail-out provision — provides an exit option if cap rates drop below your locked-in floor

Cons

- 10-year surrender period — longer than the 7-year terms on most competitors; you need to be sure you won’t need the full amount before then

- 9% surrender charge in year 1 — the penalty is steep early on, though the terminal illness and confinement waivers provide safety nets

- Not available in New York — NY residents will need to look at other Athene products or different carriers

- No flexible premiums — this is a single-premium product, so you can’t add money after the initial deposit

- Participation rates can change at renewal — while the excess return structure on some indexes helps stabilize rates, Athene can still adjust caps and participation rates annually

Who Is the Athene Agility 10 Best For?

This annuity fits best for someone who:

- Is between 50 and 70 years old with $50,000 to $500,000 to allocate

- Wants both growth and future income from the same product

- Plans to defer income for at least 10 years to maximize the benefit base

- Values a free income rider over paying 1%+ annually for a similar feature

- Is comfortable with a 10-year commitment and doesn’t need full liquidity

If you need a shorter surrender period, consider the Athene Performance Elite 7 (7-year term) or the Athene Aviator 5 (5-year term). If you want a longer commitment for potentially higher rates, the Athene Ascent Pro 10 is worth comparing.

How to Buy the Athene Agility 10

The Athene Agility 10 is sold through licensed insurance agents and financial advisors — you can’t buy it directly from Athene. Request a free quote and we’ll provide a personalized illustration showing projected income, account growth, and crediting rates based on your age and premium amount. You can also use our annuity calculators to explore scenarios on your own.

Frequently Asked Questions

Does the Athene Agility 10 have any annual fees?

No. The Athene Agility 10 has zero annual fees, and the built-in income rider is included at no additional cost. This is a significant advantage over competing FIAs that charge 0.95%–1.25% per year for a GLWB rider.

What happens if the index goes down?

If the index returns a negative number over your annual crediting period, your account is credited 0% for that year. Your principal and any previously earned interest are protected from market losses — that’s the core guarantee of a fixed index annuity.

Can I access my money before the 10-year surrender period ends?

Yes, partially. You can withdraw up to 10% of your accumulated value each year without surrender charges. Withdrawals above that amount are subject to the surrender charge schedule. The terminal illness and confinement waivers also provide full penalty-free access in qualifying situations.

How does the 20% income bonus work?

When you purchase the annuity, Athene adds 20% to your income benefit base (not your actual account value). So a $100,000 premium creates a $120,000 benefit base. Your future income payments are calculated from this benefit base, not your account value. The benefit base also grows at 175% of any annual interest earned.

Is the Athene Agility 10 available in New York?

No. The Agility 10 is available in all states except New York. If you’re a New York resident, ask us about alternative Athene products or other carriers with similar features.

Other Athene Annuity Reviews

- Athene Performance Elite 7 Review — 7-year FIA with competitive participation rates

- Athene Ascent Pro 10 Review — 10-year FIA with higher rates for longer commitment

- Athene Aviator 5 Review — 5-year FIA for shorter-term needs

- Athene Carrier Review — full company profile, ratings, and product lineup