Written by Jason Caudill, MBA

· Edited by My Annuity Store Editorial Team

Updated March 28, 2026 |

11 min read

What is a MYGA?

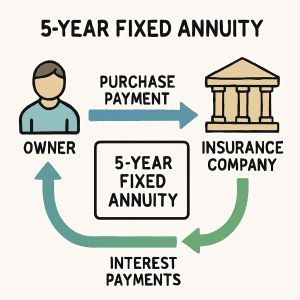

A multi-year guaranteed annuity (MYGA) is one of the safest, most predictable ways to grow retirement savings tax-deferred. You deposit a lump sum with an insurance company, they lock in a guaranteed interest rate for a set term — typically 3, 5, or 7 years — and your money grows without any market risk whatsoever.

In 2026, top MYGA rates from A-rated carriers are running 5.00%–5.75%, depending on term length and deposit amount. If you have money sitting in a bank CD earning 3.5%–4%, the math strongly favors a MYGA.

This guide covers everything you need to know: how MYGAs work, what you can earn in 2026, how they compare to CDs, tax rules, surrender charge schedules, and how to find the right one for your retirement plan.

What Is a MYGA (Multi-Year Guaranteed Annuity)?

A MYGA is a fixed annuity that locks in a specific interest rate for a predetermined number of years — and that rate never changes during the term. There are no market sub-accounts, no annual management fees, and no possibility of losing principal to investment losses.

Think of it as a CD's cousin. Same low-risk concept, but with meaningfully better interest rates and a major tax advantage: MYGA interest grows tax-deferred until you withdraw.

Feature

MYGA

Bank CD

Guaranteed interest rate

Yes — fixed for entire term

Yes — fixed for term

Tax-deferred growth

Yes — pay taxes only at withdrawal

No — taxed annually

FDIC insured

No — state guaranty association

Yes — up to $250,000

Early withdrawal penalty

Surrender charges apply

Interest penalty

Convert to lifetime income

Yes — annuitize at maturity

No

Typical rate (2026, A-rated)

4.80%–5.75%

3.50%–4.50%

How Does a MYGA Work?

You deposit a lump sum — usually $10,000 minimum, often $50,000–$250,000 — with an insurance carrier. They credit a fixed interest rate to your account every year. At the end of the term, your original deposit plus all accumulated interest is yours. No fees taken out. No market fluctuations.

Here's a real example: Robert, age 62, deposits $200,000 into a 5-year MYGA at 5.50%. At the end of five years, his account has grown to approximately $262,000 — a gain of $62,000, all tax-deferred. He paid no annual fees, and his $200,000 was never at risk.

MYGA Growth: $200,000 at 5.50% Over 5 Years

Year

Opening Balance

Interest Earned

Ending Balance

1

$200,000

$11,000

$211,000

2

$211,000

$11,605

$222,605

3

$222,605

$12,243

$234,848

4

$234,848

$12,917

$247,765

5

$247,765

$13,627

$261,392

At maturity, Robert has four choices:

Withdraw everything — pays income tax on the $61,392 gain

Roll into a new MYGA — continues tax-deferred growth at whatever rates are available in 2031

fixed annuity vs. CD comparison into another annuity product without triggering taxes

Annuitize — convert to guaranteed monthly income payments for life or a fixed period

MYGA Rates in 2026: What Can You Earn?

MYGA rates closely track the 10-year Treasury yield. With the Federal Reserve keeping benchmark rates elevated into 2026, MYGA rates remain near multi-year highs. Here's what competitive A-rated carriers are offering:

Term

Top Rate (2026)

Typical Range (A-rated)

3-Year MYGA

5.30%

4.60%–5.30%

5-Year MYGA

5.60%

4.80%–5.60%

7-Year MYGA

5.75%

4.90%–5.75%

10-Year MYGA

5.65%

4.85%–5.65%

Rates also vary by deposit size. Many carriers offer an additional 0.10%–0.20% for deposits of $100,000 or more. Check our current fixed annuity rate table for live data from top A-rated carriers — updated daily.

MYGA vs. CD: Which Pays More?

On a pure rate basis, MYGAs beat CDs by 1%–1.5% per year in 2026. But the tax advantage multiplies the difference significantly.

With a CD, you owe income taxes on interest every year — even if you don't withdraw it. With a MYGA, taxes are deferred until withdrawal. On a $200,000 deposit over 5 years, this difference can easily add $8,000–$15,000 to your net return, depending on your tax bracket.

The key trade-off is insurance: CDs are FDIC insured up to $250,000. MYGAs are backed by state insurance guaranty associations, which provide coverage of $100,000–$300,000 per carrier (varies by state). To spread risk, many buyers purchase from two separate carriers.

See our full side-by-side breakdown in our.

MYGA vs. Fixed Annuity: What's the Difference?

Every MYGA is a fixed annuity, but not every fixed annuity is a MYGA. Here's how the main types stack up:

MYGA: Same fixed rate locked in for the full term (3–10 years). The simplest, most predictable option.

Traditional fixed annuity: Rate set for an initial period (often 1–2 years), then resets annually. More flexible, but you don't know what rate year 3 brings.

Fixed index annuity (FIA): Returns tied to a market index like the S&P 500, with a 0% floor — you can't lose principal to market drops. More growth potential than a MYGA, but returns vary. Read our complete FIA guide for a full comparison.

Bottom line: if you want to know your exact balance on the last day of the term, a MYGA delivers. If you want a chance at higher returns while keeping principal protected, a fixed index annuity is worth evaluating.

Who Should Buy a MYGA?

MYGAs are not the right tool for every situation. Here's an honest look at who benefits most — and who should look elsewhere.

A MYGA makes strong sense if you:

Have $50,000–$500,000 in CDs, money markets, or savings accounts earning below-market rates

Won't need all your principal for 3–10 years

Want guaranteed, predictable growth without market exposure

Are in a higher tax bracket now and expect lower income in retirement

Have maxed out IRAs and 401(k)s and need another tax-deferred vehicle

Are between ages 55–75 and within the retirement planning window

A MYGA may not be right if you:

Need access to the full balance during the term (most MYGAs limit penalty-free withdrawals to 10% per year)

Are under age 50 with a long time horizon that argues for growth assets

Are primarily focused on maximizing estate value for heirs (life insurance typically serves that goal better)

The clearest case for a MYGA: You're 63 years old with $300,000 sitting in bank CDs rolling over at 4.0%. You don't need the money for 5 years. Moving it into a 5-year MYGA at 5.50% grows your balance by approximately $50,000 more than the CD over the same period — all tax-deferred.

How MYGAs Are Taxed

Tax treatment is one of the biggest advantages MYGAs hold over CDs. MYGA interest compounds tax-deferred — you don't pay any income tax until you take a withdrawal.

Non-qualified MYGA (funded with after-tax money):

Only the interest/gain is taxed at withdrawal — your original premium comes back tax-free

Taxed as ordinary income (not capital gains rates)

LIFO (last-in, first-out) treatment: gains come out first, then principal

Qualified MYGA (funded with IRA or 401(k) rollover):

All withdrawals are taxed as ordinary income — principal and gains — because the money was never taxed going in

Required Minimum Distributions (RMDs) apply at age 73

Early withdrawal penalty: Withdrawing before age 59½ triggers a 10% IRS penalty on top of ordinary income tax on the gain. Plan your term length accordingly.

Strategy: If you're in the 22%–24% bracket now and expect to drop to 12%–15% in retirement, deferring MYGA gains to later years can save real money. The right MYGA term often lines up with when your income drops.

Surrender Charges and Free Withdrawal Rules

MYGAs have surrender charges — fees for withdrawing more than the allowed amount before the term ends. These protect the carrier's ability to invest your premium in long-term bonds at guaranteed rates.

Typical 5-year MYGA surrender charge schedule:

Contract Year

Typical Surrender Charge

Year 1

8%–10%

Year 2

7%–8%

Year 3

6%–7%

Year 4

4%–5%

Year 5

0%

Most MYGAs include a 10% free withdrawal provision — you can take up to 10% of the account value each year without surrender charges. Many contracts also waive surrender charges for nursing home confinement, terminal illness, or required minimum distributions.

Learn more about how these charges work and how to evaluate them in our guide to annuity surrender charges.

Best MYGA Companies in 2026

The carrier matters as much as the rate. Only purchase MYGAs from insurance companies with an AM Best rating of A- or better — that rating reflects their ability to pay claims decades from now.

Buying a MYGA is simpler than most financial products. Here's what the process looks like start to finish:

Determine your investment amount. Most carriers require $5,000–$25,000 minimum. The best rates typically kick in at $100,000+. Decide how much of your savings to commit.

Choose your term. Match the term to your timeline. A 3-year MYGA gives you flexibility to reassess in 2029. A 7-year locks in today's higher rates longer. Don't commit money you might need before the term ends.

Compare rates from A-rated carriers. Use our live rate table to compare current offerings. Don't automatically choose the highest rate — verify the carrier's AM Best rating is A- or better.

Decide: qualified or non-qualified? Funding with IRA money (qualified) or personal savings (non-qualified) affects your tax picture at withdrawal. Consider your current vs. future tax bracket.

Apply through a licensed agent. Most MYGAs require a licensed insurance agent. My Annuity Store can connect you with a fiduciary advisor who will shop your rate across multiple carriers at no additional cost.

Fund the contract. Wire funds from your bank or roll over from an IRA/CD. The carrier issues your contract within a few business days.

Use your free-look period. Most states require a 10–30 day free-look period. If you change your mind, you can cancel for a full refund.

Ready to compare rates? Get a free MYGA quote — we'll shop your rate across 30+ carriers and show you the best available options for your situation.

Frequently Asked Questions About MYGAs

What is the minimum investment for a MYGA?

Most MYGA carriers require a minimum deposit of $5,000 to $25,000. Premium carriers and those offering the best rates often set minimums at $50,000 or $100,000. Deposits above $100,000 frequently qualify for a rate bump of 0.10%–0.20%.

Can I lose money in a MYGA?

You cannot lose principal to market losses — MYGAs carry zero market risk. The only way to receive less than your full deposit is if you withdraw early and surrender charges apply. Hold the contract to maturity and your full principal plus all accumulated interest is returned.

Are MYGAs FDIC insured?

No. MYGAs are insurance products, not bank deposits. They are protected by state insurance guaranty associations, which typically cover $100,000–$300,000 per carrier, per person (coverage limits vary by state). Buyers with large deposits sometimes split their investment between two or three A-rated carriers to stay within guaranty limits.

What happens when my MYGA term ends?

At maturity you typically have a 30-day window to act. Your options: withdraw the full balance (taxable on the gain), roll into a new MYGA to continue deferring taxes, do a 1035 exchange into another annuity, or annuitize for guaranteed income. If you take no action, most carriers renew your contract automatically at the current rate — which may be lower than your original rate.

How is a MYGA different from a fixed index annuity?

A MYGA delivers a fixed, guaranteed rate every year — you know your exact ending balance from day one. A fixed index annuity (FIA) links returns to a market index like the S&P 500, with a 0% floor (no losses from market declines). FIAs offer more potential upside in strong markets, but returns vary year to year. If certainty matters most, a MYGA wins. If you want some upside potential, an FIA is worth comparing.

Can I use IRA money to buy a MYGA?

Yes. MYGAs work well inside Traditional and Roth IRAs. Rolling an IRA into a MYGA (a "qualified" annuity) is a straightforward process — no taxes owed at the time of rollover. Traditional IRA-funded MYGAs will be fully taxed at withdrawal. Roth IRA-funded MYGAs can grow and be withdrawn tax-free if you meet Roth distribution requirements (age 59½ and account open 5+ years).

Editorial Disclosure: Our editorial team independently reviews and rates annuity products. We may earn commissions when you request a quote through our partner links. This content is for informational purposes only and does not constitute financial advice. Learn more.

Disclaimer: This content is for informational and educational purposes only. It does not constitute financial, tax, or legal advice. Annuity products vary by state and carrier. Always consult a licensed financial professional before making any financial decisions. My Annuity Store is an independent marketplace and does not provide investment advice.

Live Data · Updated Daily

Featured Retirement Savings Products for March 31, 2026

Rates updated: March 31, 2026, 8:07 pm ETSource: AnnuityRateWatch

Rates shown are for informational purposes only and subject to change without notice.

Products marked SI use simple interest — effective compound yield is lower than the stated rate.

Minimum premiums shown are for non-qualified (after-tax) funds.

Always verify current rates with a licensed annuity professional before purchasing.

Rates updated: March 31, 2026, 8:07 pm ETSource: AnnuityRateWatch

Rates shown are for informational purposes only and subject to change without notice.

Products marked SI use simple interest — effective compound yield is lower than the stated rate.

Minimum premiums shown are for non-qualified (after-tax) funds.

Always verify current rates with a licensed annuity professional before purchasing.

Rates updated: March 31, 2026, 8:07 pm ETSource: AnnuityRateWatch

Rates shown are for informational purposes only and subject to change without notice.

Products marked SI use simple interest — effective compound yield is lower than the stated rate.

Minimum premiums shown are for non-qualified (after-tax) funds.

Always verify current rates with a licensed annuity professional before purchasing.

Rates updated: March 31, 2026, 8:07 pm ETSource: AnnuityRateWatch

Carrier / ProductAPY

2-Year MYGA Rates

Top 1 carriers

M

Mass Mutual Best Rate

Premier Voyage 2

Term: 2 yrMin: $1,000,000Withdrawal: 10%AM Best A++

Rates shown are for informational purposes only and subject to change without notice.

Products marked SI use simple interest — effective compound yield is lower than the stated rate.

Minimum premiums shown are for non-qualified (after-tax) funds.

Always verify current rates with a licensed annuity professional before purchasing.

Rates updated: March 31, 2026, 8:07 pm ETSource: AnnuityRateWatch

Carrier / ProductAPY

3-Year MYGA Rates

Top 2 carriers

A

Athene IA Best Rate

Athene Max Rate 3

Term: 3 yrMin: $100,000Withdrawal: Interest OnlyAM Best A+

Rates shown are for informational purposes only and subject to change without notice.

Products marked SI use simple interest — effective compound yield is lower than the stated rate.

Minimum premiums shown are for non-qualified (after-tax) funds.

Always verify current rates with a licensed annuity professional before purchasing.

Rates sourced from AnnuityRateWatch. A-rated carriers (AM Best A− or better) only. Not a solicitation. Rates vary by state and deposit size. Verify current rates before purchasing.

Written by

Jason Caudill, MBA

Jason Caudill, MBA is the founder of My Annuity Store and has spent over 15 years helping clients protect retirement savings with annuities from A-rated carriers. He is an independent licensed insurance agent — not affiliated with any single carrier — which means you always get unbiased guidance.