Last updated: March 30, 2026

An annuitant is the person whose life an annuity contract is based on. Their age, gender, and life expectancy determine how much the annuity pays out and when payments stop. In most cases, the annuitant and the contract owner are the same person, but they don’t have to be.

If you’ve ever looked at an annuity application and seen “owner,” “annuitant,” and “beneficiary” listed separately, you’re not alone in wondering what the difference is. This guide breaks it down in plain English.

What Does an Annuitant Do?

The annuitant is the measuring life of the contract. The insurance company uses the annuitant’s age and life expectancy to calculate income payments. When the annuitant dies, the contract typically pays out a death benefit to the named beneficiary and the contract ends.

The annuitant does not control the contract. They can’t make withdrawals, change beneficiaries, or surrender the policy unless they are also the owner.

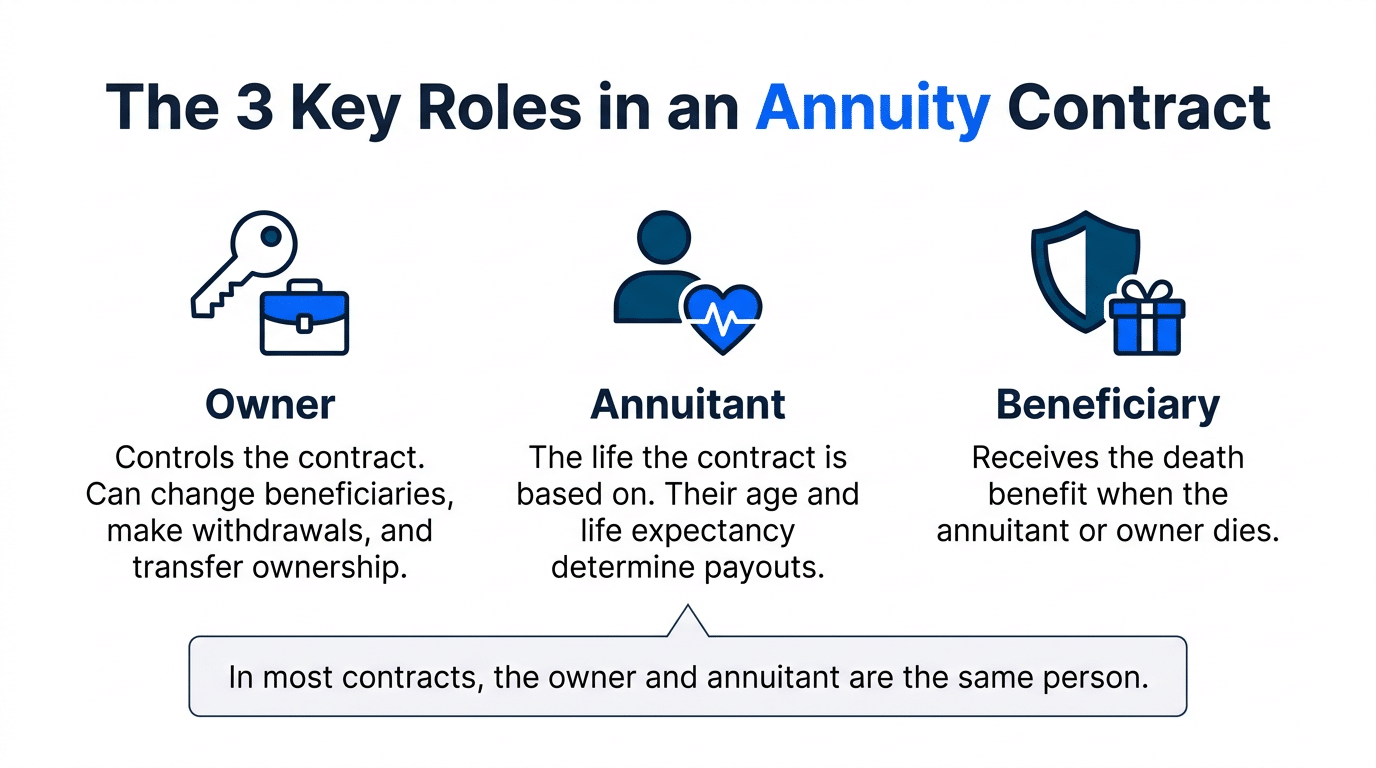

Annuitant vs. Owner vs. Beneficiary

There are three distinct roles in every annuity contract. Understanding who fills each role matters for taxes, death benefits, and estate planning.

| Role | What They Do | Key Rights |

|---|---|---|

| Owner | Controls the contract and makes all decisions | Withdrawals, beneficiary changes, surrenders, transfers |

| Annuitant | The measuring life the contract is based on | None (unless also the owner). Their age determines payouts |

| Beneficiary | Receives the death benefit when the contract ends | Death benefit claim. No control during contract |

In roughly 90% of annuity contracts, the owner and annuitant are the same person. But when they’re different, the distinction has real consequences for how the contract pays out and how it’s taxed.

When Would the Owner and Annuitant Be Different People?

There are a few common scenarios where the owner and annuitant are not the same person:

- A parent buys an annuity for a child. The parent is the owner (they control the money), while the child is the annuitant (their life expectancy determines payouts).

- A spouse names the other spouse as annuitant. This can be useful for estate planning or when one spouse is significantly younger.

- A trust owns the annuity. The trust is the owner, and a living person must be named as the annuitant since the insurance company needs a measuring life.

- Business-owned annuities. A business entity may own the contract while a key employee serves as the annuitant.

Annuitant-Driven vs. Owner-Driven Contracts

This is where it gets important. Annuity contracts fall into two categories, and the type determines what happens when someone dies.

Annuitant-driven contracts: The death benefit pays out when the annuitant dies, regardless of who owns the contract. Most older contracts and many traditional carriers use this structure.

Owner-driven contracts: The death benefit pays out when the owner dies. If the annuitant dies first, the contract continues with a new annuitant. Most modern contracts use this structure.

Why does it matter? If you’re 70 years old and you name your 45-year-old child as the annuitant on an annuitant-driven contract, the death benefit won’t trigger when you die. The contract keeps going based on your child’s life. That could create unintended tax consequences and estate planning headaches.

For a deeper comparison, see our guide on annuitant-driven vs. owner-driven contracts.

Can You Change the Annuitant?

It depends on the contract type:

- Owner-driven contracts: Yes, the owner can typically change the annuitant at any time without tax consequences.

- Annuitant-driven contracts: Usually no. Changing the annuitant may be treated as a taxable event or may not be allowed at all.

Always check the specific contract language or call the carrier before making changes. The rules vary significantly between insurance companies.

Tax Implications of the Annuitant Designation

The annuitant designation affects taxes in several ways:

- Annuity payments are calculated based on the annuitant’s life expectancy. A younger annuitant means smaller annual payments spread over more years, which can change the taxable portion of each payment (the exclusion ratio).

- Death benefit taxation depends on whether the owner or annuitant dies first, and whether the contract is owner-driven or annuitant-driven.

- Non-natural owner rules: When a trust or entity owns an annuity, the contract may lose its tax-deferred status under IRC Section 72(u) unless an exception applies.

Frequently Asked Questions

Can the annuitant and the owner be the same person?

Yes. In most annuity contracts, the owner and annuitant are the same person. This is the simplest structure and avoids the complications that come with split ownership.

What happens when the annuitant dies?

In an annuitant-driven contract, the death benefit pays out to the named beneficiary and the contract ends. In an owner-driven contract, the owner can name a new annuitant and the contract continues.

Can a trust be named as the annuitant?

No. The annuitant must be a natural person (a living human being) because the insurance company needs a life expectancy to base the contract on. A trust can be the owner, but not the annuitant.

Does the annuitant receive the annuity payments?

Not necessarily. The owner receives the payments and controls the contract. The annuitant’s role is limited to being the measuring life. However, since most people serve as both owner and annuitant, this distinction rarely comes up in practice.

Is the annuitant the same as the insured?

Similar concept, different product. In life insurance, the “insured” is the person whose life the policy covers. In an annuity, the “annuitant” serves the same function. Both are the measuring life of the contract.