Best Fixed Index Annuity Rates

A fixed index annuity is a type of annuity that credits interest based on the performance of a stock market index and also provides principal protection.

| Insurer | Annuity | Rating | Cap | Term | |

|---|---|---|---|---|---|

| American Equity | FlexShield 10 | A- | 17% | 10 Years |

| SILAC | Denali 14 | B+ | 15.00% | 14 Years |

|

| SILAC | Denali 10 | B+ | 15.00% | 10 Years |

| GILICO | WealthChoice 10 | B+ | 12.00% | 10 Years | |

| Nassau | Growth Annuity 10 | B+ | 11.25% | 10 Yrs | |

|

| SILAC | Denali 7 | B+ | 11.00% | 7 Years |

| AIG | Power 7 Protector | A | 10.75% | 7 Years | |

| Athene | Performance Elite 7 | A | 10.00% | 7 Years |

If you are looking for fixed annuity rates instead you can find them here.

10 Best Fixed Index Annuity Companies of 2025

What is a Fixed Index Annuity?

A fixed index annuity is a type of deferred annuity that offers upside potential when the market performs and downside protection from a potential market downturn.

Rather than guarantee an annual interest rate like a fixed annuity (“CD-Type Annuity“), an indexed annuity credits interest based on the performance of an external market index (such as the S&P 500).

NOTE: You may also hear fixed index annuities referred to as:

- FIA

- Equity Indexed Annuity

- EIA

- Hybrid Annuity

- Indexed Annuity

Fixed Index Annuities have less risk than variable annuities because you can’t lose value due to poor market performance.

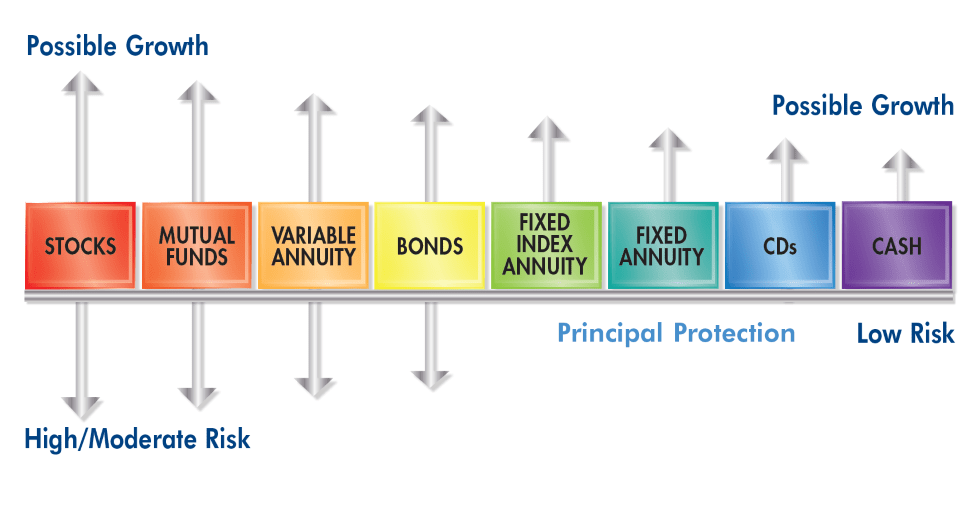

The below chart illustrates where a fixed index annuity fits on the investment continuum. Indexed annuities have increased in popularity largely because they offer the most growth potential of any investment that provides principal protection.

How do Fixed Indexed Annuities Work?

At each annual contract anniversary, the performance of the market index you’ve selected is measured. There are a couple of different index annuity crediting methods but Annual Point to Point is by far the most common.

Crediting Methods

Annual Point-to-Point Index Annuity Crediting Method

Annual point-to-point uses the index value from only two points in time making it simple and straightforward to calculate.

Calculating index performance using the annual point-to-point method:

The beginning index value is subtracted from the ending index value.

The percentage of change is calculated.

If the value at the end of the year is higher than the beginning of the year crediting component is applied to determine your interest.

Fixed Index Annuity Example:

- 107,000(ending value) minus 100,000(beginning value) = 7,000 positive change in index value.

- 7,000 (index value change) divided by 100,000(beginning index value) = 7% index performance.

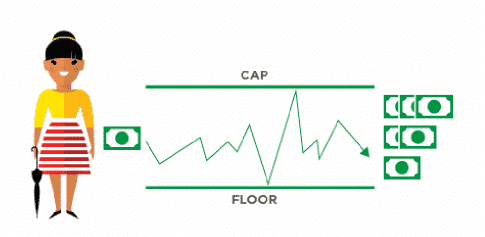

A crediting component, or limiting factor, is then applied to the index performance to determine your credited interest rate for the year.

Index Annuity Crediting Methods

- Spread – The index performance minus the spread.

- Cap – 100% of the index performance up to the cap.

- Participation Rate – The index performance multiplied by the participation rate.

Assuming a 5.00% cap, 2.00% spread and a 75% participation rate let us calculate the amount of annual interest a fixed index annuity would be credited using the 7% index performance in our example above.

Cap = 5% Interest credited (100% of index performance up to the cap)

Spread = 5% Interest credited (index performance minus the spread)

Participation Rate = 5.25% Interest Credited (index performance)

Available Indexes in a Fixed Index Annuity

1035 Exchanges for an Annuity

The Internal Revenue Service (IRS) allows you to exchange an annuity policy that you own for a new annuity policy without paying tax on the investment gains earned on the original contract. This can be a substantial benefit.

This rule is governed by Section 1035 of the Internal Revenue Code which is why these are called “1035 Exchanges.” Below is a direct link to the complete text of the code.

U.S. Code > Title 26 > Subtitle A > Chapter 1 > Subchapter O > Part III > Section 1035

1035 Exchange Rules

There are a couple of important rules that must be followed in order to receive the benefits of a 1035 Exchange.

- The tax code says that the old annuity policy must be exchanged for a new policy – you cannot receive a check and apply the proceeds to the purchase of a new insurance policy.

- You can 1035 exchange from a life insurance policy to an annuity

- You can 1035 exchange from an annuity to a long-term care policy under the Pension Protection Act of 2006

- You can not 1035 exchange from an annuity to a life insurance policy

Here is an example of an actual 1035 Exchange form you would need to complete to move from one annuity to another via a 1035 Exchange.

Advantages of a 1035 Exchange

The primary advantage of using a 1035 exchange to change your life insurance policy or annuity choices is to avoid triggering taxes on those transactions. There are different scenarios where exchanging policies or annuity contracts might make sense. For example, the advantages of a 1035 exchange include:

- You need more life insurance coverage than you currently have

- Do you want to change the type of life insurance policy you have

- You’re looking for an annuity contract with lower fees

- Do you want to restructure your annuity payments

- You currently own a variable annuity, and your risk tolerance has changed

As long as you’re exchanging contracts within the guidelines set by the IRS all of the above events will be tax-free to you.

How are Fixed Index Annuities Taxed?

The interest you earn in a fixed index annuity is typically not taxable until you withdraw it from your annuity. This tax-deferred treatment is one of the benefits of an index annuity because you don’t have to pay taxes in the year in which the interest is earned.

The deciding factor on how your annuity will ultimately be taxed depends ultimately on the money you used to buy it.

Roth IRA Annuity Taxation

If you purchase an annuity with funds from a Roth (IRA) or Roth 401(k) it is very likely you won’t have to pay federal income tax at all on the money when you withdraw it from your annuity. That includes the principal and interest.

How are Qualified Annuities Taxed?

If an annuity is purchased with qualified funds is considered a qualified annuity. Qualified funds are monies that you have never paid taxes on such as a traditional IRA or a traditional 401(k).

When you begin to make withdraws from a qualified annuity you will pay normal federal income taxes. Meaning, 100% of your annuity is treated as ordinary income and 100% of the funds will be taxed when they are taken.

Non-Qualified Annuity Taxation

A non-qualified annuity is an annuity purchased with after tax-dollars such as money from a taxable personal savings or checking account or a personal brokerage account.

If you own a non-qualified annuity, you will only pay income tax on the gain in your contract but not the money you used to purchase the annuity.

Fixed Indexed Annuity Buyers Guide

Available Indexes: The stock market indexes available in the index annuity. We have a list of available stock market indexes available at each insurance carrier for simplicity.

Duration: Typically, the longer contract you purchase the higher your guaranteed interest rate will be. But that is not the case, especially given the current inverted yield curve.

Liquidity: Most all fixed annuities have some type of annual free withdrawals, but the amount available varies by product. You’ll see most of the fixed annuities at our marketplace provide interest-only withdrawals annually. Others allow for 10% Free Withdrawals (10% of the previous year’s account value) annually.

Insurance Company’s Financial Rating: It is very important to consider an insurance company’s financial rating because it is an indicator of its ability to fulfill financial commitments to its policyholders. Usually, a lesser-rated insurance company will offer higher fixed annuity rates, but that is not always the case.

Indexed Annuity Pros and Cons

Pros

#1 Gain Compounded Earnings While Deferring Income Taxes

Earnings within an annuity contract are tax-deferred. This means you do not pay income taxes on the earnings until you withdraw gains from your account. Therefore, there are no annual 1099 forms to file or earned interest entries to make on your 1040. Tax deferral also means that annuity earnings do not offset Social Security benefits as with earnings from bonds, CDs, and other investments.

#2. Earn Higher Interest Rates

Fixed index annuities may credit higher interest rates than bank CDs or fixed interest rate deferred annuities.

#3. Make Contributions to Your Tax-Deferred Account

Investors who have maximized contributions to their qualified retirement plans (i.e. 401k, IRAs, and pensions) are permitted to contribute without limit to a tax-deferred annuity.

#4. Protect Your Principal from Downturns in the Credit Markets

When interest rates go up, annuity accounts are insulated from loss of principal; increasing interest rates often negatively impact government bonds and bond mutual funds. Unlike bonds that lose principal value during periods of rising interest rates, the account value of a fixed index annuity is guaranteed.

#5. Retire Early Without Penalty

Annuities can offer valuable tax savings for employees under the age of 59½ who receive large, lump-sum distributions from their 401(k) profit-sharing plans as part of an early retirement or severance package. Such amounts can be “rolled over” into an annuity policy without having to recognize taxable income.

#6. Satisfy Required Minimum Distributions (RMDs)

Retirees over the age of 70½ are required to begin taking withdrawals from their IRA or Pension plans, known as Required Minimum Distributions (RMDs). The IRS penalty for not doing so is a substantial 50% of any amount that falls short of the Required Minimum Distribution.

#7. Retire with a Lifetime Income

By “annuitizing” your IRA or fixed index annuity, you can exchange its value for an “immediate annuity” income stream in any of several forms (see earlier discussion on “Immediate Annuities”).

#8. Lifetime Income More Flexible Than Annuitization

Cons

Pre 591/2 10% IRS penalty.

Fixed annuities are really meant to be used for retirement savings. The IRS issues a 10% penalty on gains withdrawn from a fixed annuity for account holders under the age of 59½.

Highly Customizable

FIAs are highly customizable with a lot of moving parts which can sometimes scare people away or make it hard to select the index annuity that best meets your objectives.