The honest version: most “best places to buy an annuity online” lists are written by lead-gen sites scoring their own competitors. We’re a licensed annuity store reviewing the same field. Some of them beat us at things, and we’ll say so.

Nine platforms cover the practical universe of buying an annuity online in 2026. They split into four business models: independent brokerages (My Annuity Store, Blueprint Income, AnnuityAdvantage, ImmediateAnnuities.com, Stan the Annuity Man), carrier-direct (Gainbridge, Canvas), education and lead generation (Annuity.org, AnnuityExpertAdvice.com), and brokerage marketplaces inside a larger custodian (Fidelity, Schwab). The right one for you depends on what you want to do: shop rates across many carriers, work with a single licensed producer, buy directly from an insurer with no intermediary, or just learn before you talk to anyone.

Quick Picks: Best Annuity Platform Based on Goals

| If you want to… | Top pick | Why |

|---|---|---|

| Compare rates across the most carriers | My Annuity Store | 90+ top annuity companies, live rate tools by term and state. |

| Apply on paper by mail, not online | AnnuityAdvantage or My Annuity Store | Both work primarily by phone and overnight applications. AnnuityAdvantage has been doing it that way since 1999. |

| Meet someone face to face | None of the online platforms do this well | For a local in-person meeting, use a local independent agent or a Fidelity/Schwab branch. My Annuity Store does Zoom video meetings, which is the closest of the online platforms. |

| Buy directly from the insurance company | Gainbridge or Canvas | No intermediary. Limited to that one carrier’s products. |

| Get the best lifetime income quote | ImmediateAnnuities.com | Income annuities only, but they pull rates from more than 150 carriers and have been quoting income annuities since 1999. |

| Work with a guided digital experience | Blueprint Income | The cleanest UX in the category. Owned by MassMutual since 2021, panel of about 30 carriers. |

| Read deep educational content before deciding | Annuity.org (with a caveat) | Best content library and the highest domain authority in the category. Filling out their quote form sells your information to outside agents and call centers. |

| Work with one well-known national expert | Stan the Annuity Man | Licensed in all 50 states. Fixed annuities only (no variable, no life, no LTC). |

Independent Annuity Brokerages

An independent brokerage holds appointments with many insurance companies and can quote across all of them. Five platforms on this list work that way: My Annuity Store, Blueprint Income, AnnuityAdvantage, ImmediateAnnuities.com, and Stan the Annuity Man.

The practical differences between them come down to carrier count, product range, and who handles the application. My Annuity Store quotes across 90+ top annuity companies and covers MYGA, FIA, and SPIA contracts. Blueprint Income runs a curated panel of roughly 30 carriers with the strongest guided experience in the category. ImmediateAnnuities.com quotes income annuities only, drawing rates from more than 150 carriers. AnnuityAdvantage has brokered fixed annuities since 1999 and works primarily by phone and overnight application. Stan the Annuity Man is licensed in all 50 states and sells fixed annuities only.

Which one depends on the product. For the broadest fixed annuity rate comparison, My Annuity Store. For lifetime income quotes specifically, ImmediateAnnuities.com. For a guided digital walkthrough, Blueprint Income.

Carrier-Direct Annuity Platforms

Carrier-direct means buying from the insurance company itself, with no broker in between. Two platforms on this list do that: Gainbridge and Canvas Annuity.

The trade is speed against choice. Both let you complete a purchase online in minutes without speaking to anyone, which none of the brokerages on this list match. Both are also limited to a single carrier’s lineup, so no rate comparison is happening on the page you are buying from. If that carrier is competitive for your term and state, that is a fast and clean way to buy. If it is not, nothing inside their site will tell you.

When carrier-direct makes sense: you have already compared rates elsewhere, you know the product you want, and you would rather not talk to anyone to get it issued.

Lead Generation Annuity Websites

Annuity.org and RetireGuide.com show up at or near the top of almost every annuity search on Google. Both are owned by Launch That LLC, a digital marketing company based in Orlando, Florida. Launch That is a search engine optimization firm with a portfolio of content sites in legal, financial, and medical verticals.

Credit where it’s due. Annuity.org has more glossary entries, more long-form guides, and more domain authority than this site or any of the other independent brokerages on this list. The content is well organized and well written. Their job is to capture organic search traffic at the top of the funnel, and they are very good at it.

The trade-off shows up when you submit a quote form. Annuity.org does not directly sell annuities. According to Trustpilot reviews, the form submission triggers outbound contact from multiple unaffiliated insurance agents and call centers. Several reviewers describe being contacted repeatedly by people they did not ask to hear from. Annuity.org is BBB accredited on the publishing entity, which is not the same thing as being an accredited insurance agency.

RetireGuide.com follows the same model. The site is categorized by the Better Business Bureau as “Senior Services, Retirement Planning Services, Information Bureaus, Sales Lead Generation.” Its lead pipeline is filled, in part, through partnerships with Senior Market Sales and GoHealth.

None of this makes those sites bad places to learn. It does mean that if your goal is to actually buy an annuity, you are probably better off starting with a licensed insurance entity that handles the policy end to end. That is the distinction this list is built around.

Custodian and Brokerage Annuity Marketplaces

The fourth business model is the annuity desk sitting inside a brokerage you may already use for investing. Fidelity and Charles Schwab both run one. Neither is ranked in the nine below, because both are annuity desks attached to a much larger custodian rather than standalone online annuity platforms.

Fidelity sells income, fixed, and variable annuities through a curated panel of insurers it calls the Fidelity Insurance Network, rather than shopping the open market. The process starts by scheduling a conversation with their team.

Schwab offers variable, fixed deferred, indexed, and income annuities. The constraint that matters most is stated plainly on Schwab’s own annuity page: there is a $100,000 minimum for all annuity contracts offered through Schwab. Carriers on the open market issue MYGA contracts for far less, some at $2,500 to $5,000, so that floor removes Schwab from consideration for a large share of buyers before rates ever enter the conversation.

When a custodian makes sense: you already hold your retirement assets there, you are placing $100,000 or more, and keeping the contract alongside the rest of your portfolio is worth more to you than shopping the full carrier market.

Top 9 Online Annuity Platforms Ranked

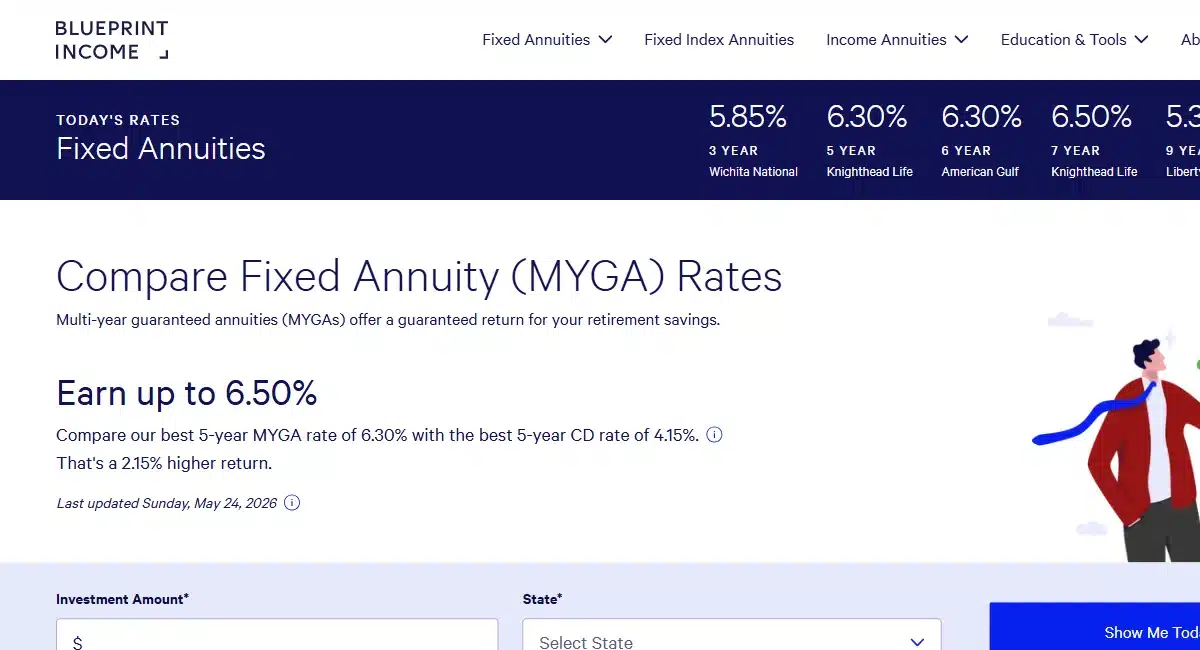

1. Blueprint Income

Best for: consumers who want a polished, calculator-driven online experience with a curated carrier panel and human backup.

Blueprint Income is the cleanest online annuity experience in the category, hands down. The site walks you through scenarios with clear language and shows estimated income before you talk to a human. The platform is an independent annuity marketplace that joined MassMutual as a subsidiary in February 2021 and works with roughly 30 carriers, ranging from B+ to A++ ratings. Reps are FINRA-registered.

Trade-off: a curated 30-carrier panel is smaller than the independent broker panels at My Annuity Store, AnnuityAdvantage, or ImmediateAnnuities.com. If you want the broadest possible MYGA rate comparison, that 30-carrier ceiling matters.

Full comparison: Blueprint Income vs. My Annuity Store

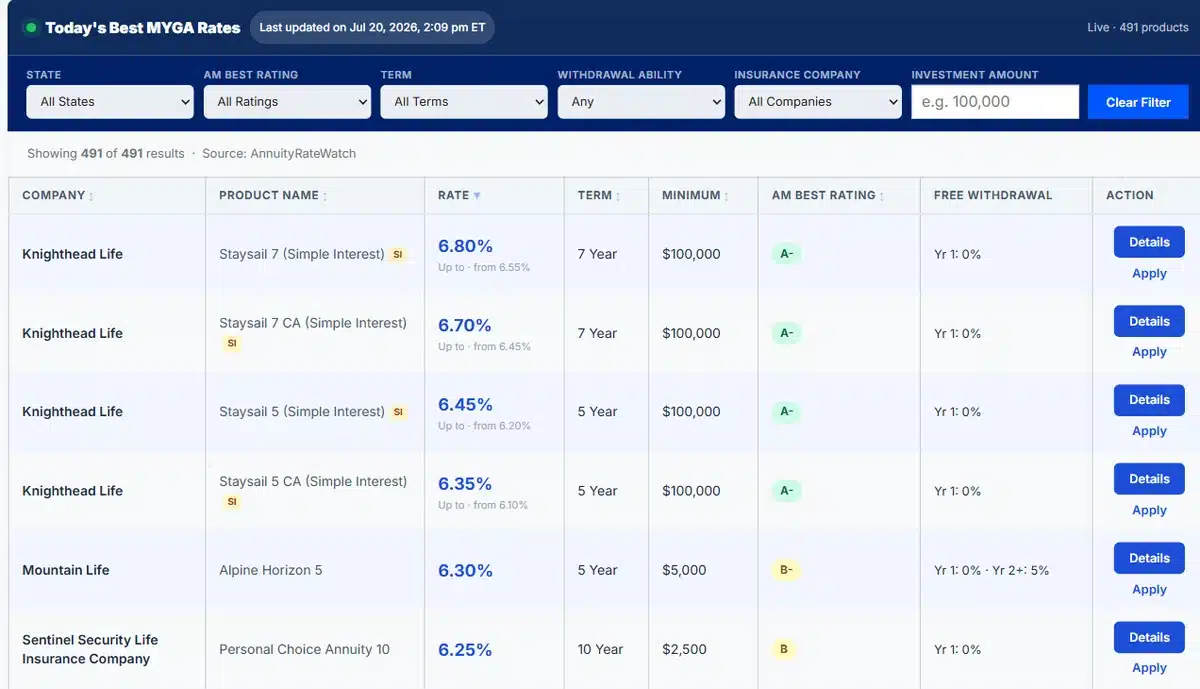

2. My Annuity Store

Best for: buyers who want to compare the broadest set of carriers themselves before speaking with anyone, and who want the same licensed producer from quote through issue.

My Annuity Store is an independent annuity store licensed in 47 states, founded in 2020 by Jason Caudill, MBA, who has distributed more than $1 Billion in annuities since 2005. The rate marketplace publishes live MYGA, FIA, and SPIA rates drawn from 90+ top annuity companies, filterable by state, term, AM Best rating, withdrawal ability, carrier, and investment amount. Rates are visible without a form fill, and each product page discloses the commission percentage paid on the contract. Quote requests are handled in-house by licensed producers rather than sold to a lead network.

Trade-off: the content library is thinner than Annuity.org’s, and the interface is more utilitarian than Blueprint Income’s. Buyers who want a guided, design-led walkthrough will prefer Blueprint Income.

Try it: My Annuity Store’s annuity rate comparison tool

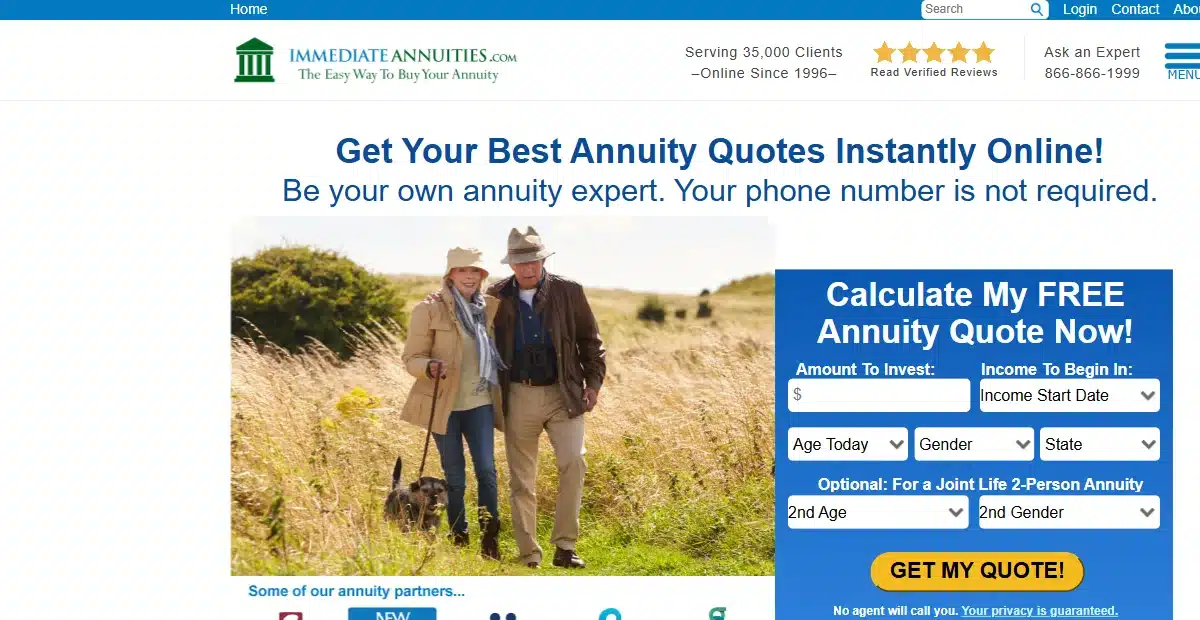

3. ImmediateAnnuities.com

Best for: retirees specifically shopping for guaranteed lifetime income.

Operated by WebAnnuities Insurance Agency, Inc., founded 1999 by Hersh Stern. The platform shows real-time income payouts from more than 150 carriers. Trustpilot ratings are near 4.9 out of 5. BBB-accredited as an insurance agency.

Strict scope: this is an immediate and deferred income annuity platform. If you want a 5-year MYGA, an indexed annuity with an income rider, or a variable annuity, look elsewhere.

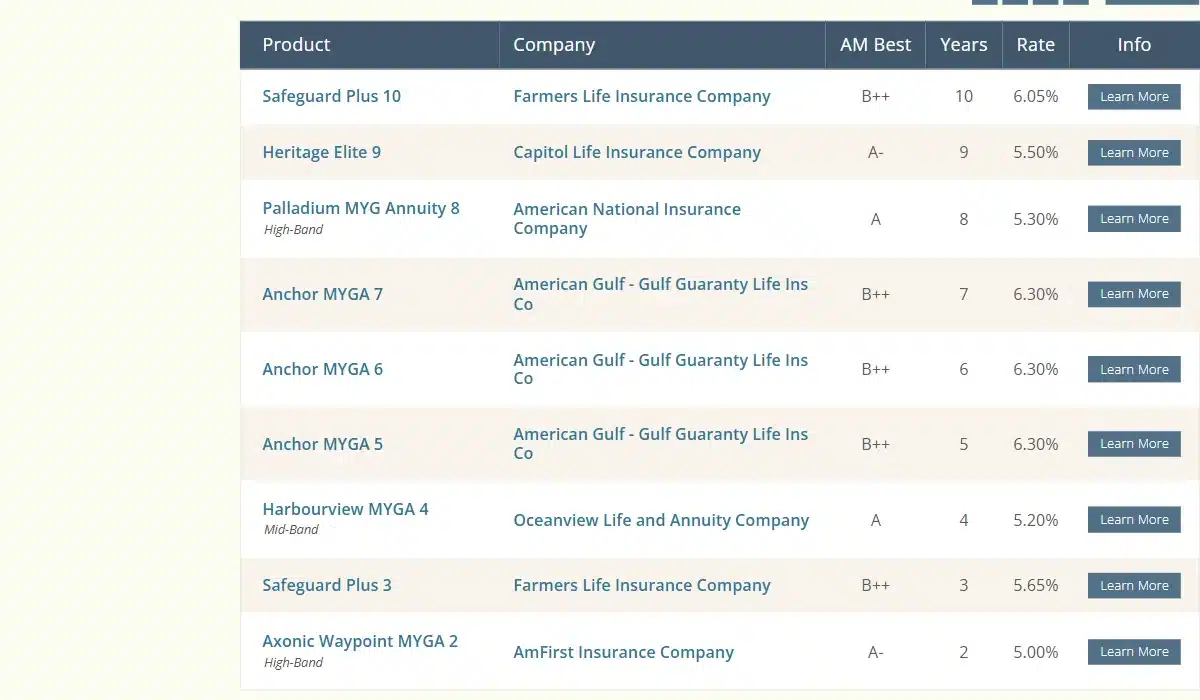

4. AnnuityAdvantage

Best for: buyers who prefer phone and paper to online applications.

Founded in 1999 by Ken Nuss in Medford, Oregon. One of the longest-running independent annuity brokerages on the internet. Offers fixed, MYGA, fixed indexed, and immediate income annuities through dozens of carriers, with a publicly listed carrier directory. Phone-first workflow; applications can be mailed or completed electronically.

Trade-off: the site UX is dated by current standards and rates are not all visible upfront. Strength: deep institutional knowledge of the annuity market and a clear phone-and-mail process for buyers who do not want to do everything online.

Full comparison: AnnuityAdvantage vs. My Annuity Store

5. Stan the Annuity Man

Best for: consumers who want a nationally recognized expert as their single point of contact.

Stan Haithcock and his team are licensed in all 50 states. The business is fixed annuities only: MYGAs, fixed indexed annuities, and lifetime income annuities. No variable annuities, no life insurance, no long-term care. Personality-driven brand built on YouTube videos, books, and plain-language explanations of contractual guarantees.

Trade-off: smaller operation than the bigger independent brokerages, so scheduling can take longer. If you want a high-volume rate-shopping experience, this is not it. If you want one named expert who works your case personally, this is a strong fit.

Full comparison: Stan the Annuity Man vs. My Annuity Store

6. Gainbridge

Best for: buyers who want to skip the middleman and buy directly from an insurance company online.

A digital-first carrier-direct platform. Gainbridge sells fixed and fixed indexed annuities issued by its parent insurer. No independent agent involved, no commission paid, no rate shopping across competitors. The trade-off is real: simplified pricing and a single-carrier experience, in exchange for no comparison shopping. If the Gainbridge contract terms happen to be the best for your situation, fine. If they’re not, you would not know without checking elsewhere.

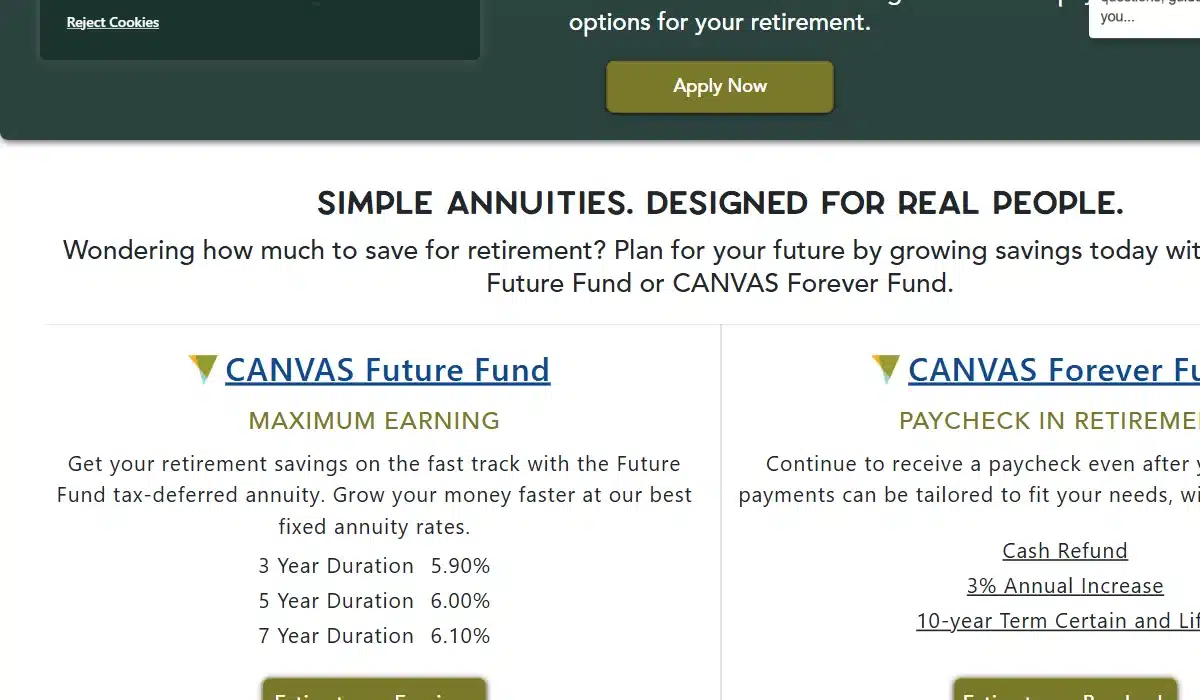

7. Canvas Annuity

Best for: simple fixed annuity purchases from a single insurer, completed online.

Canvas Annuity products are issued by Puritan Life Insurance Company of America. Like Gainbridge, this is carrier-direct. Customers work with insurance company employees, not independent agents. Product scope is limited to Canvas-issued contracts and rate shopping is not possible inside the platform.

8. Annuity.org

Best for: educational research, not buying.

The largest content site in the annuity category, owned by Launch That LLC, an Orlando-based SEO firm. The glossary, calculators, and long-form guides are well written and well organized. BBB accredited since 2019 on the publishing entity. Not a licensed insurance agency for execution: form submissions are routed to outside agents and call centers, which is the source of recurring complaints on Trustpilot about repeated unsolicited calls.

Use the content. Skip the quote form unless you want to be contacted by multiple agents.

Full comparison: Annuity.org vs. My Annuity Store

9. AnnuityExpertAdvice.com

Best for: long-tail educational content and side-by-side platform comparisons.

Education-first site that publishes detailed reviews of other annuity platforms (including critical reviews of Annuity.org and similar lead-gen sites). Operates as a referral broker to outside licensed agents rather than executing policies in-house. Useful as a research stop; not the platform to use for the actual purchase.

Where competitors beat us, and where they don’t

Where they win:

- Annuity.org has more content depth and higher domain authority. They are an SEO machine with a content budget we cannot match. If your goal is to read 40 articles before buying, start there.

- Blueprint Income has a better user experience. Owned by MassMutual, well capitalized, design-led. If polish matters more to you than carrier breadth, they win on that.

- Gainbridge and Canvas are faster for single-carrier purchases. If you already know you want their specific product, you can complete a purchase in minutes without an agent.

Where we win:

- Carrier breadth. 90+ top annuity companies, versus a curated panel of about 30 at Blueprint Income, or a single carrier at Gainbridge and Canvas.

- Live rate tables you can sort and filter yourself. No form-fill required to see the actual rate by term, carrier, and AM Best rating.

- No lead resale. Your information stays in-house with a licensed producer, not with a network of call centers.

- Live carrier illustration before you sign. Every product recommendation comes with a carrier-issued illustration, not a brochure or a hypothetical.

How we ranked the best places to buy an annuity online

Rankings reflect editorial judgment, not annuity rates, performance projections, or insurer guarantees. Those vary by individual circumstances and state availability. The evaluation focuses on how a consumer actually experiences each platform.

Transparency of business model. Each platform was scored on how clearly it discloses whether it is an independent brokerage, a carrier-direct insurer, or an educational lead-generation site.

Access to insurance companies. Independent brokerages were evaluated on the breadth of their carrier panel. Carrier-direct platforms were evaluated on the clarity and competitiveness of their single-carrier offering.

Online tools and rate visibility. Platforms that allow consumers to see actual rates and tools before submitting personal information scored higher.

User experience and accessibility. Site navigation, mobile usability, clarity of explanations, and the logical flow from education to quoting to consultation.

Execution and consumer control. Whether inquiries are handled by in-house licensed professionals or distributed to third parties, and whether the buyer controls the pace of the process.

Credibility signals. Years in operation, named licensed leadership, verifiable third-party reviews, and publicly available BBB and Trustpilot history.

Editorial independence

Inclusion is not an endorsement. My Annuity Store is one of the nine platforms reviewed and is rated by its own criteria alongside competitors. Where publicly available information was limited, that is noted in the review.

The best annuity platform for any individual depends on goals, product preferences, age, state of residence, and comfort with digital or advisory workflows. Use the quick-pick table above as a starting filter, then dig into the individual reviews.

Frequently asked questions about buying an annuity online

Can you buy an annuity entirely online?

Partly. Carrier-direct platforms like Gainbridge and Canvas Annuity let you complete a purchase online in minutes without speaking to anyone. Independent brokerages show you rates online, but a licensed producer has to submit the application, so expect at least one phone or video conversation before the contract is issued.

Is it safe to buy an annuity online?

The website is not what backs your money. An annuity is guaranteed by the claims-paying ability of the issuing insurance company, so the carrier and its rating matter far more than where you bought the contract. What the platform does control is whether your information stays in-house or gets sold to a network of call centers, and whether you see actual contract terms before you sign. Confirm the seller is a licensed insurance entity rather than a publisher earning a referral fee.

Can I buy an annuity through Fidelity or Charles Schwab?

Yes. Both run annuity desks alongside their brokerage business. Fidelity sells income, fixed, and variable annuities through a curated panel of insurers it calls the Fidelity Insurance Network. Schwab offers variable, fixed deferred, indexed, and income annuities, with a $100,000 minimum for all annuity contracts offered through Schwab. Neither one shops the full independent carrier market.

What is the difference between an annuity marketplace and a lead generation site?

A marketplace is a licensed insurance entity that quotes carriers and issues the contract. A lead generation site is a publisher: it ranks well in search, collects your contact details through a quote form, and sells that information to outside agents and call centers. Annuity.org and RetireGuide.com, both owned by Launch That LLC, follow the lead generation model. The tell is whether the site can actually issue you a policy.

Do you pay more for an annuity if you buy it through a broker?

Not as a separate charge. Fixed annuity commissions are paid by the insurance company rather than deducted from your premium, so your full deposit is credited either way. The cost of distribution is built into the rate a carrier offers, which is why the credited rate across a wide carrier panel is the number worth comparing, not the commission itself.

Related buying guides

- How to Buy an Annuity: Complete Guide

- Should I Buy an Annuity?

- Compare Fixed Annuity Rates

- Best Fixed Annuity Companies

- Fixed Annuity vs. CD

- Annuity Fees and Commissions Explained

- What Are Hypothetical Annuity Quotes?

See the rates and income numbers for your situation.

Our licensed team will run live quotes across 90+ top annuity companies for the products in this lesson. No cost, no obligation.