When evaluating fixed index annuity rates, it’s crucial to compare the different options available to maximize your retirement income. Fixed Index Annuities credit interest based on the performance of an external stock market index, such as the S & P 500 or the Nasdaq. Interest is credited to the annuity when the value of the market index goes up. When the market index goes down, no interest is credited.

If you are looking for fixed annuity rates, you can find them here instead.

| Product Name | Company Name | AM Best | Max Age | Minimum | Years | Income Rider | Free withdrawals | Pt-to-Pt Cap | Premium Bonus | Fixed Rate | Learn More |

|---|

Many investors are currently interested in fixed index annuity rates for their potential benefits.

The table below lists the fixed index annuity rates and crediting strategies for the top fixed index annuities available today. Click the compare button to compare up to 3 annuities side by side.

When comparing different options, take note of the fixed index annuity rates available to you.

| Compare | Carrier | AM Best / S&P | Product | Indexing Strategies (Highlights) | Current Caps & Rates | Surrender Schedule | Min Guarantee | State Availability | Min Premium | Issue Ages | Notable Features |

|---|---|---|---|---|---|---|---|---|---|---|---|

| MassMutual Ascend | A++ / A+ | WealthChoice 7 (Single) | Fixed Rate 1-Year S&P 500 Annual Pt-to-Pt Cap Horizon Ascent 5% Index Pt-to-Pt Participation 1-Year S&P 500 Performance Trigger Additional strategies available • FireLight eligible | Fixed: 8.00% S&P 500 Pt-to-Pt Cap: 10.25% Horizon Ascent 5% Par: 165.00% Perf Trigger: 7.10% | 9, 8, 7, 6, 5, 4, 3 (7 yrs) | 87.5% of premium @ 1.00% | Except: AK, HI, ME, NY | $20,000 | 0–90 | Cap Bailout (S&P 500) 6.75%; 10% free W/D yr 1; TI/NH waivers; Income rider (with cost, max issue age 75 with GLBR); Non-MVA in AK, PA, UT (lower caps/rates); CA higher caps/rates, no MVA; E-Application only; Rate/Cap decrease noted 10/27. | |

| Nationwide Life Ins. Co. of America | A+ / A+ | American Legend 7 (Flexible) | Fixed Rate S&P 500 Annual Pt-to-Pt Cap S&P 500 7-Year Cap Lock Pt-to-Pt S&P 500 RC Pt-to-Pt Participation Additional strategies available • FireLight eligible | <$100k / $100k+ Fixed: 4.05% / 4.25% S&P 500 Cap: 9.50% / 10.00% 7-Yr Cap Lock: 7.00% / 7.25% RC Participation: 70.00% / 75.00% | 9, 8, 7, 6, 5, 4, 3 (7 yrs) | 87.5% of premium @ 3.00% | Except: NY | $10,000 (NQ / Q); add-ins $2,000 | 0–85 (NQ/Q) | 10% free W/D yr 1; LTC/Confinement & TI waivers (varies by state); Additional premium in 1st year only; CA surrender/rate variations. | |

| Delaware Life | A- / A- | Peak 10 (Single) | Fixed S&P 500 Avg DRC Ann Pt-to-Pt Cap AB Growth & Value Bal Par (2-Year) J.P. Morgan Cycle Par (2-Year) S&P 500 Avg DRC Par (2-Year) Additional strategies available | <$100k / $100k+ Fixed: 3.70% / 3.95% Avg DRC Cap: 8.50% / 9.50% AB G&V Par (2-Yr): 220% / 240% JPM Cycle Par (2-Yr): 235% / 250% Avg DRC Par (2-Yr): 195% / 205% | 10, 10, 9, 8, 7, 6, 5, 4, 3, 2 (10 yrs) | 1.00% on 87.5% of premium | Except: CA, DE, NY | $25,000 | 0–85 | Guaranteed Income Solution included (no fee); Bonus Income+ Rider (with fee); State variations for surrender & rates/caps; LTC/Confinement & TI waivers (varies). | |

| MassMutual Ascend | A++ / A+ | WealthChoice 5 (Single) | Fixed Rate 1-Year S&P 500 Annual Pt-to-Pt Cap Horizon Ascent 5% Index Pt-to-Pt Participation 1-Year S&P 500 Performance Trigger Additional strategies available • FireLight eligible | Fixed: 7.00% S&P 500 Pt-to-Pt Cap: 10.25% Horizon Ascent 5% Par: 160.00% Perf Trigger: 7.00% | 9, 8, 7, 6, 5 (5 yrs) ± MVA | 90.8% of premium @ 3.85% | Except: NY | $25,000 | 0–90 | Cap Bailout (S&P 500) 6.50%; 10% free W/D yr 1; TI/NH waivers; Flexible premium in year 1; E-Application only; Rate/Cap decrease noted 10/27. | |

| Sagicor | A- | Sage Accumulator 5 (Single) | 1-Year Fixed 1-Year S&P 500 Annual Pt-to-Pt Cap 1-Year Pt-to-Pt MSCI EAFE ETF Par 1-Year Pt-to-Pt MSCI Emerging Market Par Additional strategies available • FireLight eligible | <$75k / $75k+ Fixed: 4.50% / 5.00% S&P 500 Cap: 9.50% / 10.50% MSCI EAFE Par: 60% / 65% MSCI EM Par: 55% / 60% | 9, 8, 7, 6, 5 (5 yrs) ± MVA | 87.5% of premium @ 1.00% | Except: AK, HI, ME, NY | $20,000 | 0–90 | 10% free W/D yr 1; TI/NH waivers; CA different rates & surrender charges. | |

| Sagicor | A- | Sage Accumulator 7 (Single) | 1-Year Fixed 1-Year S&P 500 Annual Pt-to-Pt Cap 1-Year Pt-to-Pt MSCI EAFE ETF Par 1-Year Pt-to-Pt MSCI Emerging Market Par Additional strategies available • FireLight eligible | <$75k / $75k+ Fixed: 4.50% / 5.00% S&P 500 Cap: 9.50% / 10.50% MSCI EAFE Par: 60% / 65% MSCI EM Par: 55% / 60% | 9, 8, 7, 6, 5, 4, 3 (7 yrs) ± MVA | 90.8% of premium @ 3.85% | Except: NY | $250,000 | 0–90 | 10% free W/D yr 1; TI/NH waivers; CA different rates & surrender charges. | |

| Delaware Life | A- / A- | True Path Income (Single) | 1-Year S&P 500 Annual Pt-to-Pt Cap 1-Year S&P 500 Pt-to-Pt w/ Performance Trigger Fixed Rate Additional strategies available • FireLight eligible | <$100k / $100k+ S&P 500 Cap: 5.00% / 5.50% Perf Trigger: 4.50% / 5.00% Fixed: 3.10% / 3.35% | 10, 9, 8, 7, 6, 5, 4, 3, 2, 1 (10 yrs) ± MVA | 87.5% of premium (less w/d & related charges, excl. MVA) @ 2.65% | Except: NY | $25,000 (add-ins $500 NQ) | 45–85 | 30-day free withdrawal/surrender window at end (or prior, if applicable) of guarantee period. |

Investors should carefully consider fixed index annuity rates when choosing a strategy that fits their financial goals.

Fixed index annuity rates are influenced by various factors including market conditions and contract terms. The variety of fixed index annuity rates available today allows for tailored investment strategies.

Market trends can influence fixed index annuity rates, making research essential.

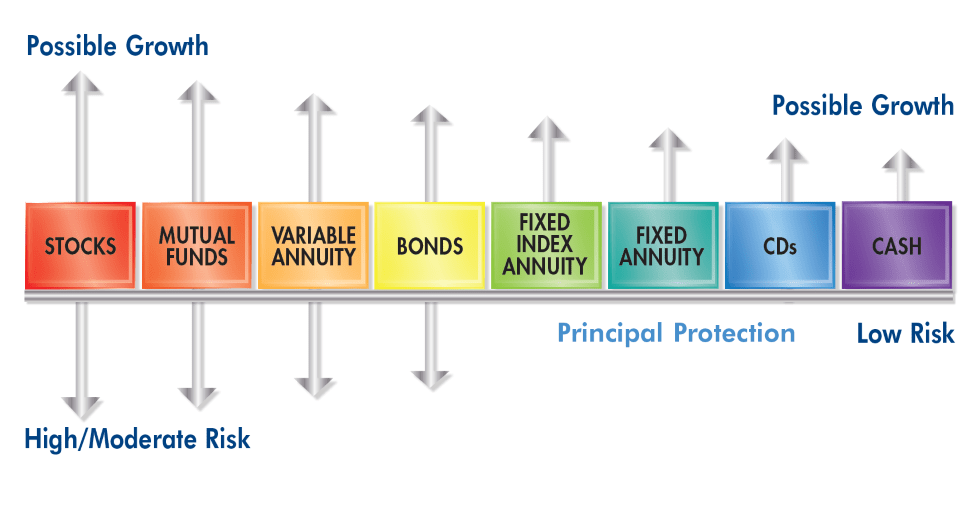

Principal protection linked to fixed index annuity rates provides peace of mind for investors.

Choosing the right index can affect your fixed index annuity rates and overall returns.

Consider how fixed index annuity rates will impact your long-term financial strategy.

Fixed index annuity rates can provide a safety net while allowing for potential growth.

Understanding surrender charges can help investors navigate fixed index annuity rates more effectively.

The fixed index annuity rates determine your potential earnings over the investment period. The choice between caps, participation, and spreads is crucial when analyzing fixed index annuity rates.

Fixed index annuity rates vary by provider, so it’s important to compare options.

Monitoring your fixed index annuity rates can lead to better financial outcomes.

Fixed index annuity rates can provide a balanced approach to growth and security.

Pro tip: Often, volatility-control indexes pair with higher participation rates, which can be attractive in today’s rate environment.

Read our Comprehensive Best Fixed Index Annuity Companies of 2026 Guide to learn more about the product offerings from top rated insurance companies.

No. Fixed index annuity (FIA) crediting terms—caps, participation rates, and spreads—are declared by the carrier and can change at each renewal period. Once a term is completed, that credit is locked in and cannot be retroactively changed.

Your principal and credited interest are protected from market losses. However, your contract value can decrease if you take withdrawals above the free-allowance, surrender early (surrender charges/MVA may apply), or if you pay optional rider fees.

We aim to refresh this page monthly and whenever carriers release significant rate changes. For the most current carrier-approved rate sheets, call 855-583-1104 or email info@myannuitystore.com.

Example: If the index returns 12% and your cap is 7%, your credit is 7%. If par is 45%, credit would be 5.4% before any spreads. If spread is 3% and the index returns 10%, credit is 7%.

Many accumulation-focused FIAs have no explicit annual policy fee. Optional riders (e.g., lifetime income, enhanced death benefit) may carry fees that reduce your contract value. Always review the product disclosure for details.

Most FIAs include free withdrawals (often up to 10% of the account value annually) after the first contract year. Withdrawals above the free amount during the surrender period may incur surrender charges and a market value adjustment (MVA), if applicable.

Common choices include the S&P 500 and proprietary volatility-control indexes from major banks. Popular strategies include Annual Point-to-Point with a cap, participation rate (no cap), or spread, plus occasional 2-year strategies that may offer different terms.

It depends on your goals. MYGAs offer a guaranteed multi-year fixed rate and simplicity. FIAs provide principal protection with index-linked growth potential, but credits vary by terms and index performance. If guaranteed rate is the priority, a MYGA may fit; if growth potential above a fixed rate appeals—with protection—consider an FIA.

Match the surrender period to your time horizon, confirm liquidity needs, and select a mix of strategies and indexes that align with your risk tolerance. If lifetime income is a goal, compare rider fees, roll-up rates, and payout factors in addition to accumulation terms.

Call 855-583-1104 or email info@myannuitystore.com. We’ll confirm your state, objectives, and liquidity needs, then share carrier-approved rate sheets and best-fit products.

When comparing products, fixed index annuity rates should be a key consideration.

Fixed index annuity rates may offer attractive options compared to traditional products.

There are many aspects to consider regarding fixed index annuity rates that could impact your decision.

Available Indexes: The stock market indexes available in the index annuity. We have a list of available stock market indexes available at each insurance carrier for simplicity.

Duration: Typically, the longer contract you purchase the higher your guaranteed interest rate will be. But that is not the case, especially given the current inverted yield curve.

Liquidity: Most all fixed annuities have some type of annual free withdrawals available, but the amount available varies by product. You’ll see most of the fixed annuities at our marketplace provide interest-only withdrawals annually. Others allow for 10% Free Withdrawals (10% of the previous year’s account value) annually.

Insurance Company’s Financial Rating: It is very important to consider an insurance company’s financial rating because it is an indicator of its ability to fulfill financial commitments to its policyholders. Usually, a lesser-rated insurance company will offer higher fixed annuity rates, but that is not always the case.

Tip: Check spam/promotions if you don’t see our email on time.

Need help sooner or have a quick question?

What happens next

Tip: Check your spam or promotions folder if you don’t see our email within the time window.