- The best annuity for retirement depends on the job you need it to do, not the product label. We map five real retirement use cases to a specific top pick for each.

- For a Social Security bridge, a 5-year period-certain SPIA on $100,000 pays roughly $1,849 a month for 60 months, more than three times what a CD ladder produces.

- For couples who want guaranteed income that lasts until both spouses pass, the Athene Ascent Pro 10 Bonus with joint income rider pays $11,730 a year on $100,000 starting at 70 (a 5-year deferral), and never reduces when one spouse dies.

- For QLACs, MassMutual (A++) consistently leads payouts for male annuitants, with $100,000 deferred 15 years producing $32,564 in annual lifetime income beginning at 75.

The Best Annuity Depends on the Job You Need It to Do

"Best annuity" is the wrong question. The right question is best annuity for what. A 62-year-old who wants to delay Social Security to 70 needs a totally different product than a 70-year-old looking to defer required minimum distributions, and both need something different than a couple who wants joint lifetime income that does not stop when one spouse dies. This guide breaks the decision down into the five real retirement use cases we see most often at My Annuity Store, and names the specific top pick for each, with current 2026 rates and a $100,000 example so you can see exactly what the income looks like.Find the right

annuity for you.

Six quick questions. We'll rank the three annuity types best matched to your goals, time horizon, and risk tolerance, with a side-by-side comparison.

Side-by-side comparison

Top 3 picksEducational tool. Final recommendations require a personalized consultation.

How We Picked the Best Annuities for Each Goal

We compare 90+ top annuity companies through our independent broker platform. For this guide, every product had to clear three filters: an A- or better financial strength rating from AM Best, current 2026 pricing competitive within the top decile of its category, and contract terms a fiduciary would recommend without flinching. We do not get paid to feature specific carriers. The picks below are the products we actually quote and place for clients with these exact retirement goals. Rate data is pulled from AnnuityRateWatch for MYGAs, CANNEX for SPIAs, and direct carrier illustrations for income riders.Best Annuities for Retirement at a Glance

| Retirement Goal | Best Annuity Type | Top Pick | $100K Income / Rate |

|---|---|---|---|

| Social Security bridge (early retirement) | 5-year period-certain SPIA | Top A+ carrier | $1,849 / month for 60 months |

| Joint lifetime income for couples | FIA with joint income rider (5-yr deferral) | Athene Ascent Pro 10 Bonus | $11,730 / year for both lives starting at 70 |

| Live on interest, preserve principal | 5-year MYGA | Top MYGA | 5.40% guaranteed for 5 years |

| Market upside with no losses | Fixed index annuity (accumulation) | Allianz Benefit Control | 30% participation, 0% floor |

| Defer RMDs past age 73 | QLAC | MassMutual (A++) | $18,297 / yr at age 70 (10-yr defer) |

Best Annuity for an Early Retirement Social Security Bridge

If you retire at 62 but want to wait until 67 or 70 to claim Social Security, you have a problem and an opportunity. Every year you delay benefits past full retirement age, your monthly check grows about 8%. But you still need to eat, pay the mortgage, and cover health insurance during that gap. This is what a Social Security bridge annuity solves. The right product here is a 5-year period-certain SPIA, also called a 5-year fixed-period income annuity. You hand the insurance company a lump sum, and it pays you a check every month for exactly 60 months, then stops. By the time the payments end, your Social Security has grown to its maximum and takes over.$100,000 Example: 5-Year SPIA Bridge

- Premium: $100,000

- Monthly income: $1,849

- Total payments over 5 years: $110,940

- Effective yield: roughly 4.2% net of return of principal

Best Annuity for Joint Lifetime Income (Couples)

For a married couple, the worst-case retirement scenario is not running out of money at 80. It is running out at 90, after one spouse has already passed and the survivor is alone. A joint lifetime income annuity removes that risk by guaranteeing income for as long as either spouse is alive. The top pick here is the Athene Ascent Pro 10 Bonus fixed indexed annuity with the Athene Ascent Income Rider, configured for joint payouts. Athene is one of the largest fixed annuity carriers in the United States, rated A+ by AM Best, and the Ascent Pro 10 Bonus is the contract that consistently produces the best joint income figures in our independent comparisons across 90+ top annuity companies.$100,000 Joint Life Example: M65 / F63, Income Starts at 70

- Premium: $100,000

- 10% premium bonus added to account value at issue (vesting over 10 years)

- 20% income base bonus, plus 10% simple interest roll-up for years 1 through 20

- Income base at age 70 (year 6): $170,000

- Joint lifetime withdrawal rate at 70: 6.90%

- Joint annual income starting at 70: $11,730 for both lives

- Income continues until both spouses pass, even if account value reaches zero

- Account value remains accessible; no annuitization required

- Rider charge: 1.00% of benefit base annually

- 10% annual free withdrawal on top of income

- Enhanced income benefit pays 1.5x if either spouse cannot perform 2 of 6 activities of daily living (60-month benefit period)

Best Annuity If You Don't Want to Spend Your Principal

Plenty of retirees in their 60s and 70s are not income-poor. They have $500,000 to $1.5 million in savings, Social Security covers their fixed costs, and what they actually want is a place to park money where it earns a guaranteed rate, kicks off interest income they can spend, and leaves the principal intact for heirs. For that, nothing beats a multi-year guaranteed annuity (MYGA). A MYGA works like a CD with three advantages: rates are typically 100 to 200 basis points higher than comparable bank CDs, interest grows tax-deferred until withdrawn, and the entire principal is guaranteed by an A-rated insurer plus state guaranty associations.$250,000 Example: 5-Year MYGA at 5.40%

- Annual interest: $13,500

- Principal at end of year 5: $250,000 (untouched)

- Total interest over 5 years (taken as income): $67,500

- State guaranty coverage: $250,000 in most states

Best Annuity for Market Upside With Downside Protection

If you remember 2008, the appeal of an annuity that captures S&P 500 gains but never loses money to a market crash is obvious. That is what a fixed index annuity (FIA) without an income rider delivers. The trade-off compared to direct stock ownership is real: you give up dividends and you cap your upside, in exchange for a hard 0% floor. The top pick for pure accumulation, where you do not need lifetime income from the contract, is the Allianz Benefit Control Annuity. Allianz is one of the largest annuity carriers in the United States, rated A+ by AM Best, and Benefit Control offers some of the most competitive participation rates in the industry on uncapped index strategies.How the Math Works

- If the S&P 500 gains 20% in a year and your participation rate is 50%, you get a 10% credit

- If the S&P 500 loses 30% in a year, you get 0%, not -30%

- Credits are locked in at the end of each crediting period and cannot be lost in future years

- No annual rider fee on the pure accumulation version

Best Annuity to Defer Required Minimum Distributions (QLAC)

Once you turn 73, the IRS forces you to start taking required minimum distributions from your traditional IRA and 401(k). For retirees with seven-figure IRA balances, those forced withdrawals can push you into a higher tax bracket and bump up Medicare IRMAA surcharges. A Qualified Longevity Annuity Contract (QLAC) is the IRS-blessed workaround. You can move up to $210,000 of IRA money into a QLAC in 2026 (the limit is indexed annually). That money is exempt from RMD calculations, and you defer the income until as late as age 85. When the income finally turns on, it pays for the rest of your life, with payouts that get bigger the longer you defer.$100,000 QLAC Payouts in May 2026

| Deferral Period | Best Carrier (Male) | Annual Income (M) | Best Carrier (Female) | Annual Income (F) |

|---|---|---|---|---|

| 10 years (start age 70) | MassMutual (A++) | $18,297 | Western & Southern (A+) | $16,657 |

| 15 years (start age 75) | MassMutual (A++) | $32,564 | Western & Southern (A+) | $28,219 |

| 20 years (start age 80) | MassMutual (A++) | $65,542 | Western & Southern (A+) | $54,340 |

Life-only QLAC payouts on $100,000 premium for a 60-year-old, May 2026. Source: Blueprint Income.

The math gets remarkable at longer deferrals. A 60-year-old male who puts $100,000 in a MassMutual QLAC and waits 20 years collects $65,542 a year for life starting at 80. By age 90, total payments equal $655,420, more than 6.5 times the original premium. The IRS treats this as a permitted form of longevity insurance, exactly the use case Congress intended when it created QLACs in 2014 and expanded the limit under SECURE Act 2.0. Read more in our QLAC explainer and the IRS RMD rules.How to Decide Which Annuity Fits Your Retirement

If the quiz at the top did not give you a clear answer, work through these three questions in order:- When do you need the money? Now means SPIA. In 5 to 15 years means MYGA, FIA, or QLAC. After 73 with RMD pressure means QLAC.

- Single or joint? If you are married and want both lives covered, your shortlist narrows to joint SPIAs, joint income riders on FIAs, or joint-life QLACs. Single-life products pay more per dollar but stop at one death.

- Do you need access to principal? If yes, MYGA or FIA. If you are willing to give up principal in exchange for a higher monthly check, SPIA.

Annuities to Avoid in 2026

Not every annuity belongs in a retirement plan. Three categories to skip outright:- Variable annuities with M&E fees above 1.5% combined with rider charges above 1.25%. Total fee drag of 2.75% to 3.25% per year is hard to overcome, and the 2022 bear market exposed how fragile some of the income-base guarantees actually are.

- Anything from a B-rated or unrated carrier. Reach for yield by going down the credit-quality ladder is exactly how retirees lost money in the 1990s with Executive Life and again in 2008 with smaller carriers. Stick to A- or better from AM Best.

- Deferred annuities sold to buyers over 80 with surrender periods longer than 5 years. If a producer is putting an 82-year-old into a 10-year surrender contract, that is a suitability violation. Walk away.

Common Annuity Mistakes Retirees Make

- Putting too much in one product. Most clients should not have more than 30 to 50% of liquid retirement assets in annuities. The rest should stay in market-based investments for growth and flexibility.

- Annuitizing when you do not have to. Modern income riders give you guaranteed lifetime income without ever giving up your account value. Annuitization (true annuitization) is rarely the right answer outside of SPIA situations.

- Ignoring tax location. Putting a tax-deferred annuity inside a traditional IRA gives you no extra tax benefit and adds fees. Annuities work best in non-qualified money or in a deliberate QLAC strategy.

- Buying from one carrier. Always compare at least three carriers before signing. Rates and rider terms vary widely, and a 0.50% difference on a 10-year MYGA is worth $5,000+ on a $100,000 deposit.

- Forgetting beneficiaries. Update beneficiaries every time there is a major life event. An annuity passes outside probate, but only if the beneficiary form is current.

Sources & Citations

- AM Best for carrier financial strength ratings

- IRS Required Minimum Distribution rules and SECURE Act 2.0 QLAC limits

- LIMRA Secure Retirement Institute for industry sales and product trends

- NAIC for state guaranty association coverage

- Blueprint Income for current QLAC payout benchmarks

- Athene Ascent Pro 10 Bonus illustration prepared April 28, 2026 for Male 65 / Female 63 joint, $100,000 premium, AZ, income activation age 70

Frequently Asked Questions

What is the best type of annuity for retirement?

It depends on your goal. MYGAs are best for guaranteed capital preservation at a locked-in rate. FIAs are best for growth potential without downside risk. SPIAs are best for converting savings into a guaranteed monthly paycheck for life. Most retirees benefit from a combination of two types rather than committing everything to one product. A licensed independent agent can model the right allocation for your specific income gap and timeline.

How much does a $100,000 annuity pay per month in retirement?

A $100,000 SPIA purchased by a 65-year-old male pays roughly $585 to $640 per month for life, based on recent carrier payouts. A $100,000 MYGA instead earns tax-deferred interest at the current fixed rate; see our live rate tables for today's MYGA rates and the interest that produces.

What are the best MYGA rates right now?

Top MYGA rates from our 90+ top annuity companies change frequently, sometimes week to week, so a number quoted here would go stale fast. We publish live MYGA rate tables updated daily instead. See our fixed annuity rates page for today's best 3-, 5-, and 7-year rates.

Is it better to buy an annuity before or after retirement?

Buying within five years of your planned retirement date is often ideal. You lock in current rates, protect the principal you will need soon, and can time income to start when you stop working. Buying too early ties up money you may need. Buying too late means fewer years of tax-deferred growth.

Are fixed annuities safe for retirees?

Fixed annuities (MYGAs) are among the most conservative retirement products available. They are backed by the issuing insurance carrier and protected by state guaranty associations, typically up to $250,000 per carrier. They are not FDIC insured, but are regulated by state insurance departments and required to maintain sufficient reserves. Look for carriers with an AM Best rating in the A range (A-, A, A+, or A++) for maximum security.

Are annuities a good option in 2026?

For retirees and pre-retirees seeking guaranteed income or principal protection, annuities are among the strongest options available in 2026. Current MYGA rates are historically attractive relative to CD alternatives, and SPIA payouts remain competitive. The key is matching the right product type to your specific timeline.

What is the safest annuity to buy?

A MYGA from a financially strong, highly rated carrier (AM Best A- or higher) is the safest annuity type. Your principal is fully guaranteed, the interest rate is locked in for the entire term, there are no annual fees, and your money is protected by state guaranty associations. There is zero market risk. For an extra layer of safety with larger deposits, spread the money across two carriers to stay within state guaranty limits.

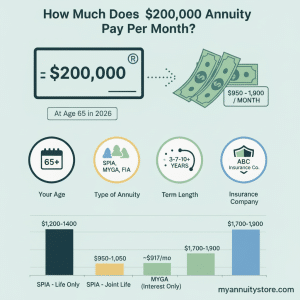

How much does a $200,000 annuity pay per month?

A $200,000 SPIA for a 65-year-old male pays roughly $1,170 to $1,280 per month for life, depending on the carrier. A $200,000 MYGA instead earns tax-deferred interest at the current fixed rate. The exact figures depend on your age, gender, state, and the specific carrier.

Can you lose money in a fixed annuity?

No, as long as you hold the contract through the surrender period. Fixed annuities (MYGAs) and fixed indexed annuities (FIAs) guarantee your principal. The only scenario where you would receive less than your deposit is if you withdraw more than the annual free withdrawal allowance (typically 10%) before the surrender period ends, triggering surrender charges. Those charges decline each year and disappear entirely when the term is complete.

What happens to my annuity when I die?

It depends on the product and payout option you selected. Most annuities pass the remaining account value directly to your named beneficiaries, bypassing probate entirely. SPIAs with a life-only payout end at death with no remaining value to heirs. SPIAs with a period-certain or cash refund option guarantee that your beneficiaries receive any unpaid balance. FIAs and MYGAs pass the full account value to named beneficiaries.