Annuity Frequently Asked Questions

Browse by category, search keywords, or expand questions below. Updated to help you quickly find clear, unbiased annuity answers.

An annuity is a contract with an insurance company where you exchange a premium (single lump sum or series of payments) for guarantees: tax-deferred growth, income you cannot outlive, principal protection, or a combination of these depending on the annuity type.

Think of it as a retirement efficiency tool: convert assets into predictable, optionally lifetime, cash flow while managing sequence-of-returns risk and longevity risk.

- Lifetime income to hedge longevity risk

- Principal protection (fixed, MYGA, fixed indexed)

- Tax deferral on non-qualified money

- Market participation with downside protection (indexed annuities)

- Interest rate diversification vs CDs / bonds

- Legacy planning with beneficiary designations

You earn either fixed interest, index-linked credits, or income payments. The insurer earns a spread: they invest premiums in a conservative, diversified general account and allocate a portion to options (for indexed annuities) while retaining a margin to cover guarantees, expenses, and profit.

A Fixed Indexed Annuity credits interest based on the performance of an external index (e.g., S&P 500) subject to limits (caps, participation rates, spreads) while guaranteeing that your account will not lose value due to negative index performance (excluding optional rider fees, if any).

- Cap: Maximum interest credit for a period.

- Participation Rate: Percentage of index gain credited (e.g., 50% of a 10% gain = 5%).

- Spread/Margin: Amount subtracted from the index gain (e.g., 10% gain - 2% spread = 8% credit).

These pricing levers are how insurers control cost of option budgets and guarantee principal protection.

Market declines do not reduce your accumulation value (floor is 0% credited). However, you could see a decline in surrender value if you withdraw during the surrender period and charges apply, or if rider fees exceed interest in a given year.

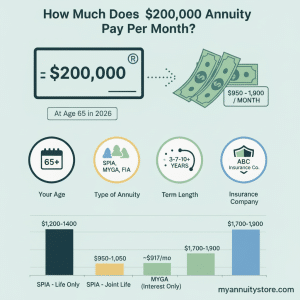

A MYGA is the insurance industry’s version of a multi-year CD: a guaranteed fixed interest rate for a specified term (e.g., 3, 5, 7 years) with tax deferral on non-qualified money. At the end of the term you can renew, 1035 exchange, annuitize, or withdraw (subject to contract provisions).

- Taxation: MYGA grows tax-deferred; CD interest is typically taxed annually (unless in an IRA).

- Liquidity: CDs often allow early withdrawals with an interest penalty; MYGAs may have limited free withdrawal provisions (e.g., 10%) with surrender charges otherwise.

- Guarantees: CD covered by FDIC (up to limits); MYGA backed by insurer financial strength and state guaranty association (varies by state). Not FDIC.

A Single Premium Immediate Annuity converts a lump sum into a guaranteed income stream that begins within 12 months. Payments can be life-only, period certain, joint life, or life with refund features.

A SPIA starts income now (within 12 months); a DIA defers income for several years, allowing a higher payout later due to mortality credits and deferral. DIA is useful for future income planning (e.g., longevity hedge starting at age 80).

An income rider is an attached benefit (often for a fee) that guarantees a future lifetime withdrawal amount based on a separate "benefit base" that may grow at a stated roll-up rate or via performance. The benefit base is not a cash value—it’s a calculation figure for income.

Typical annual fees range from 0.85% to 1.5% of the benefit base (or accumulation value, depending on contract). Evaluate whether the guaranteed income improvement justifies the drag on accumulation value if you do not ultimately use the rider.

Most annual point-to-point strategies credit once at the end of the strategy term (e.g., 12 months). Some have monthly or multi-year terms. Changes to caps/participation apply on strategy anniversaries—not retroactively.

Diversify among strategies with different mechanics (point-to-point, volatility-controlled, monthly sum) to smooth outcomes. Compare implied option budget (higher participation or cap often indicates more budget) and avoid chasing only last year’s hypothetical back-test.

Growth is tax-deferred. Withdrawals are taxed on a last-in, first-out (LIFO) basis: gains out first taxed as ordinary income. After all gain is withdrawn, remaining principal is a non-taxable return of basis.

For annuities held in qualified accounts (IRA), the contract’s value counts toward your RMD. Many contracts allow RMD withdrawals without surrender charges. Lifetime income payments from an annuitized contract may fully or partially satisfy the RMD (verify each year).

Base fixed, MYGA, and fixed indexed annuities typically do not have an explicit annual fee. Fees arise when optional benefits (income riders, enhanced death benefits) are added. Variable annuities commonly have M&E, subaccount, and rider fees.

A declining percentage applied to withdrawals above contractual free-liquidity during the surrender period (e.g., 9%, 8%, 7% …). It compensates the insurer for up-front acquisition and hedging costs.

Most deferred annuities allow an annual penalty-free withdrawal (often 10% of the prior anniversary value). Exceeding that amount early can trigger surrender charges or market value adjustment (if applicable).

Safety depends on insurer financial strength and product type. Fixed and indexed annuities are backed by the insurer’s general account. State guaranty associations provide additional protection (limits vary; not FDIC; cannot be used as a selling point in all states).

Ratings reflect an independent view of claims-paying ability. Higher-rated carriers may offer slightly lower credited rates but provide perceived stability. Diversifying among strong carriers can mitigate concentration risk.

Annuitization converts the contract to an irrevocable income stream (limited liquidity). A lifetime withdrawal rider preserves control of remaining account value (subject to depletion if withdrawals exceed growth) and may allow beneficiary payout of remaining value.

The “best” time aligns with a planning trigger: securing future income, locking in current interest rates, reallocating a maturing CD, mitigating sequence-of-returns risk near retirement, or improving longevity coverage. Trying to time short-term interest movements often introduces more delay than benefit.

- Personal info (name, address, SSN for suitability & anti-money laundering)

- Beneficiary designations

- Funding source (check, transfer, 1035 exchange, IRA rollover)

- Financial profile & objectives (income need, risk tolerance)

- Replacement forms if moving from another contract

Primary agencies: AM Best, S&P, Moody’s, Fitch, KBRA, plus COMDEX (composite). We aggregate ratings on our carrier pages for quick comparison.

Yes, distributions of taxable amounts from tax-qualified or non-qualified deferred annuities before age 59½ may incur a 10% federal penalty unless an exception applies (e.g., death, disability, certain periodic payments). Consult a tax professional.

Each state maintains a guaranty association that may protect policy owners if a licensed insurer becomes insolvent, subject to statutory limits. These protections vary and cannot be used as a primary selling point in many states. Always evaluate insurer strength first.

Disclaimer: Information is educational, not individualized tax, legal, or investment advice. Guarantees are backed by the claims-paying ability of the issuing insurer. Always review the actual contract and disclosure documents.

Frequently Asked Questions About Multi-Year Guaranteed Annuities (MYGAs)

Below are the questions real clients ask us before (and after) purchasing a Multi-Year Guaranteed Annuity. Expand any topic. Nothing here is personalized advice—always evaluate your own liquidity needs, time horizon, tax situation, and overall plan.

Basics

1. What is a MYGA?

2. How is a MYGA different from a CD?

- Taxation: CDs typically generate annual 1099-INT; MYGA interest defers until withdrawal (non-qualified money).

- Insurance Backing: CDs = FDIC (up to limits). MYGAs rely on the insurer’s claims‑paying ability plus state guaranty association coverage (limits vary by state—not FDIC).

- Liquidity: Both can penalize early withdrawals; MYGAs use surrender charges & possibly a Market Value Adjustment (MVA).

- Minimums: MYGAs often higher ($5k–$100k typical minimum) vs low CD minimums.

3. How does a MYGA differ from a Fixed Indexed Annuity (FIA)?

4. Who is a MYGA generally suitable for?

Rates & Growth

5. Are MYGA rates guaranteed for the entire term?

6. How are MYGA rates set?

7. What happens at the end of the term (maturity)?

- Withdraw without surrender charges

- Renew into an available rate term

- Execute a 1035 exchange to another annuity

- Annuitize (convert to an income stream)

Liquidity & Access

8. Can I withdraw money during the term?

9. What is a Market Value Adjustment (MVA)?

10. Can I use a MYGA for short-term cash needs?

Taxes & Accounts

11. How is interest taxed in a non-qualified MYGA?

12. How do Required Minimum Distributions (RMDs) work with MYGAs in IRAs?

13. Does a MYGA issue a 1099 each year?

Safety & Guarantees

14. Are MYGAs FDIC insured?

15. What if the insurance company is downgraded?

Planning & Strategy

16. What is a MYGA ladder and why build one?

- Mitigates reinvestment timing risk

- Creates periodic liquidity points

- Captures potentially higher long-term rates while keeping near-term flexibility

17. Can I convert a MYGA to lifetime income later?

18. When does a 1035 exchange make sense?

Process & Logistics

19. What are the typical minimums and maximums?

20. Are there annual fees?

21. How are agents/commissions paid?

22. How fast can I lock a rate?

23. What documents will I receive?

24. What happens if I withdraw before age 59½ (non-qualified)?

25. Is there any inflation protection?

Disclaimer: This FAQ is general education—not individualized tax, legal, or investment advice. Guarantees are subject to the issuing insurer’s financial strength. State guaranty association protections vary and are not a substitute for FDIC insurance. Review the contract, disclosure documents, and your own financial plan before purchasing or exchanging an annuity.

Compare Annuity Rates

Considering purchasing an annuity? Visit our online annuity marketplace and compare today’s fixed annuity rates in real-time.

Frequently Asked Questions About Multi-Year Guaranteed Annuities (MYGAs)

Below are the questions real clients ask us before (and after) purchasing a Multi-Year Guaranteed Annuity. Expand any topic. Nothing here is personalized advice—always evaluate your own liquidity needs, time horizon, tax situation, and overall plan.

Basics

1. What is a MYGA?

2. How is a MYGA different from a CD?

- Taxation: CDs typically generate annual 1099-INT; MYGA interest defers until withdrawal (non-qualified money).

- Insurance Backing: CDs = FDIC (up to limits). MYGAs rely on the insurer’s claims‑paying ability plus state guaranty association coverage (limits vary by state—not FDIC).

- Liquidity: Both can penalize early withdrawals; MYGAs use surrender charges & possibly a Market Value Adjustment (MVA).

- Minimums: MYGAs often higher ($5k–$100k typical minimum) vs low CD minimums.

3. How does a MYGA differ from a Fixed Indexed Annuity (FIA)?

4. Who is a MYGA generally suitable for?

Rates & Growth

5. Are MYGA rates guaranteed for the entire term?

6. How are MYGA rates set?

7. What happens at the end of the term (maturity)?

- Withdraw without surrender charges

- Renew into an available rate term

- Execute a 1035 exchange to another annuity

- Annuitize (convert to an income stream)

Liquidity & Access

8. Can I withdraw money during the term?

9. What is a Market Value Adjustment (MVA)?

10. Can I use a MYGA for short-term cash needs?

Taxes & Accounts

11. How is interest taxed in a non-qualified MYGA?

12. How do Required Minimum Distributions (RMDs) work with MYGAs in IRAs?

13. Does a MYGA issue a 1099 each year?

Safety & Guarantees

14. Are MYGAs FDIC insured?

15. What if the insurance company is downgraded?

Planning & Strategy

16. What is a MYGA ladder and why build one?

- Mitigates reinvestment timing risk

- Creates periodic liquidity points

- Captures potentially higher long-term rates while keeping near-term flexibility

17. Can I convert a MYGA to lifetime income later?

18. When does a 1035 exchange make sense?

Process & Logistics

19. What are the typical minimums and maximums?

20. Are there annual fees?

21. How are agents/commissions paid?

22. How fast can I lock a rate?

23. What documents will I receive?

24. What happens if I withdraw before age 59½ (non-qualified)?

25. Is there any inflation protection?

Disclaimer: This FAQ is general education—not individualized tax, legal, or investment advice. Guarantees are subject to the issuing insurer’s financial strength. State guaranty association protections vary and are not a substitute for FDIC insurance. Review the contract, disclosure documents, and your own financial plan before purchasing or exchanging an annuity.

Popular Resources

Keep going with the most helpful next steps—compare options, understand costs, and see how buying online works.