Annuity rates vary by state. We suggest using the filters to find the best fixed annuity rates in your state. Choose your age, liquidity features, and investment amount. The annuity rates shown below are sourced through Annuity Rate Watch and updated automatically every 6 hours via API.

Key Takeaways

- Top MYGA rate today: up to 6.50% for 7 years from top annuity companies, updated daily.

- Fixed annuities beat 5-year CDs by 1.0%-1.5% and all interest grows tax-deferred.

- Minimum deposits start at $2,500; most buyers invest $50,000-$250,000.

- Your money is protected by state guaranty associations up to $250,000 per insurer.

Fixed Annuities vs CDs

Fixed annuities and CDs both appeal to savers who want predictable, guaranteed growth, but they work differently beyond the headline rate. A CD is issued by a bank and is FDIC-insured; a fixed annuity is issued by an insurance company, is backed by the insurer’s claims-paying ability and state guaranty association, and grows tax-deferred, which materially changes your after-tax return.

| Term | MYGA Rate | Top CD Rate | Tax-Equivalent Yield* |

Annuity | CD | Annuity Edge |

|---|---|---|---|---|---|---|

| 2-Year | 5.15% CL Life | 4.30% National Best | 6.78% | $110,565 | $108,785 | +$1,780 |

| 3-Year | 5.65% Farmers Life Insurance Company | 4.20% National Best | 7.43% | $117,926 | $113,137 | +$4,789 |

| 4-Year | 5.20% Oceanview Life and Annuity | 4.10% National Best | 6.84% | $122,479 | $117,436 | +$5,043 |

| 5-Year | 6.30% American Gulf | 4.25% National Best | 8.29% | $135,727 | $123,135 | +$12,592 |

*Tax-Equivalent Yield shows the pre-tax CD rate a saver in the 24% federal bracket would need to match the annuity rate on a tax-deferred basis (formula: annuity rate ÷ (1 − bracket)). Actual after-tax results depend on your full tax situation, state tax, and timing of withdrawals.

Sources: Annuity rates: May 13, 2026 · AnnuityRateWatch. CD rates: May 1, 2026 · Bankrate.com. Annuity values use compound interest at the stated rate; products marked SI use simple interest. Rates subject to change without notice. Availability & features vary by state and insurer. Guarantees are backed by the claims‑paying ability of the issuing insurance company. Not a bank product. Not FDIC insured. State guaranty association limits apply (vary by state).

Why the tax-equivalent column matters. A CD pays interest every year and the IRS taxes it every year. A MYGA compounds untouched until you withdraw. That’s why a 5.65% MYGA is worth roughly 7.43% to a saver in the 24% bracket, because a taxable CD would need to yield 7.43% to match it on an after-tax basis. The higher your bracket, the wider the gap. Run your own numbers with our fixed annuity vs. CD calculator or see the full fixed annuity vs. CD comparison guide.

Caveat: If you withdraw annuity earnings before age 59½, you may owe a 10% IRS penalty plus ordinary income tax. Fixed annuities are best suited for money you do not need until retirement. See IRS Publication 575 for full tax treatment.

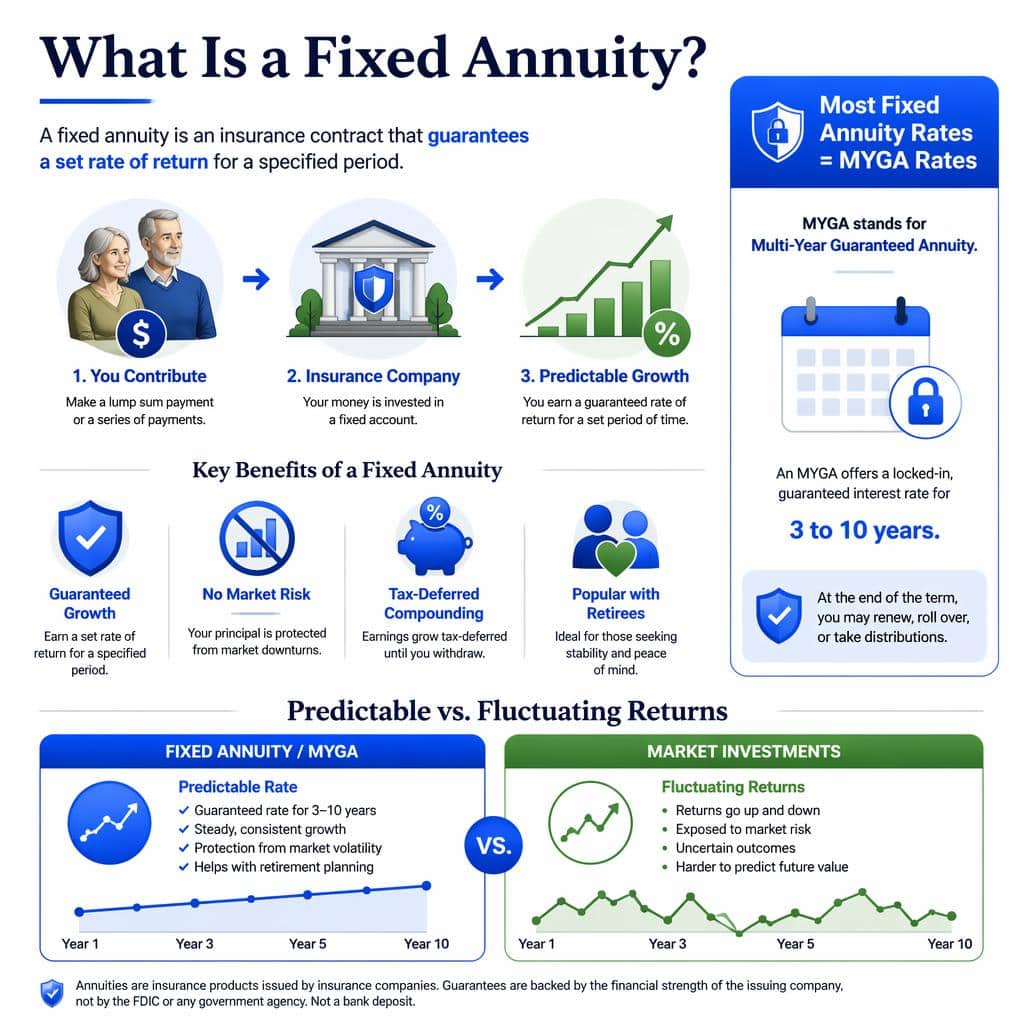

What Is a Fixed Annuity?

A fixed annuity is an insurance contract that guarantees a set rate of return on your contributions over a specified period. You hand over a lump sum (or a series of payments), and in return, the insurer promises predictable, steady growth. Fixed annuities are popular among retirees because they offer a safe way to grow savings with tax-deferred compounding and no market risk.

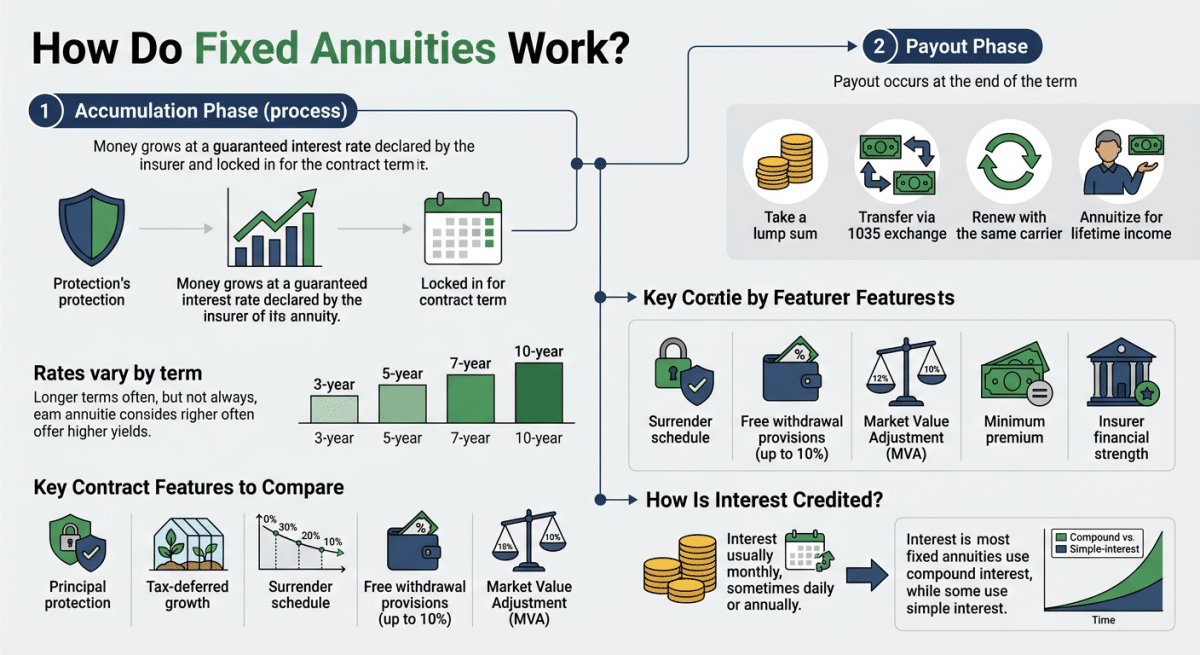

How Do Fixed Annuities Work?

Fixed annuities have two phases:

- Accumulation phase: Your money grows at a guaranteed interest rate declared by the insurer, locked in for the contract term.

- Payout phase: At the end of your term, you can take a lump sum, transfer to another annuity via a 1035 exchange, renew with the same carrier, or annuitize for lifetime income.

Fixed annuity rates are usually tied to the contract term. A 3-year annuity may offer one rate, while a 5-, 7-, or 10-year annuity may offer a different one. Longer terms often (but not always) pay higher yields. The best fixed annuity for you is not always the one with the single highest rate, because two contracts with similar yields can still differ on several dimensions:

Key contract features to compare

- Principal protection: Your original investment is shielded from market downturns.

- Tax-deferred growth: You will not owe taxes on earnings until you withdraw, letting your money compound without annual tax drag.

- Surrender schedule: A surrender charge is a fee for withdrawing more than the annual free amount during the surrender period. Schedules vary by product and can be steep, so think about your cash needs before you buy.

- Free withdrawal provisions: Most MYGAs allow up to 10% of account value each year penalty-free.

- Market Value Adjustment (MVA): Adjusts the surrender value if you withdraw early, reflecting how interest rates have changed since purchase. If current rates are higher, MVA reduces payout; if lower, MVA can increase it.

- Minimum premium: Some products require $2,500; others start at $25,000 or more.

- Insurer financial strength: Your guarantee is only as strong as the insurer standing behind it. See how to evaluate an insurance company below.

How Is Interest Credited?

A fixed annuity usually credits interest to your account monthly, though some insurers credit daily or annually. Similar to a CD, the rate is set when you buy the contract and is guaranteed for the entire term.

Most fixed annuities credit compound interest, meaning the interest earned each year is added to your balance and the following year you earn interest on the larger balance. A smaller number credit simple interest, which only earns interest on the original deposit.

Here is how the two credit methods play out on a $100,000 annuity at 5.90% over 5 years:

| Year | Compound Interest | Simple Interest |

|---|---|---|

| Year 1 | $105,900 | $105,900 |

| Year 2 | $112,148 | $111,800 |

| Year 3 | $118,765 | $117,700 |

| Year 4 | $125,772 | $123,600 |

| Year 5 | $133,193 | $129,500 |

| Total Gain | $33,193 | $29,500 |

Compounding produces $3,693 more over five years on the same deposit and the same rate, a gap that widens significantly over longer terms. Use our fixed annuity calculator to project growth for your own deposit.

What Affects Fixed Annuity Rates?

Rates are driven by a mix of market conditions, insurer strategy, and product design. The seven factors below explain why one contract pays 6.50% while another pays 5.20% on the same term. For a deeper walkthrough, see our guide on how fixed annuity rates are set.

- Interest rates and Treasury yields: Insurers invest premium dollars in bonds, so when yields rise, annuity rates rise. MYGA rates tracked higher after the 2022-2023 Fed hiking cycle for this reason.

- Contract term length: Longer terms usually pay more because the insurer can invest your premium longer. Weigh the extra yield against the longer surrender schedule.

- Insurer pricing strategy: Some carriers compete aggressively on rate to win deposits; others offer slightly lower yields but stronger ratings or better liquidity features.

- Financial strength and risk profile: Lower-rated carriers often lead the rate tables. Check the AM Best rating and other insurance company ratings before you trade strength for yield.

- State availability: Products and rates vary by state filing rules. A contract offered in Florida may not be approved in New York.

- Premium amount: Many insurers offer tiered rates. Deposits of $100,000 or more typically earn higher rates than smaller deposits in the same product.

- Optional features and liquidity: Contracts with enhanced free withdrawals, MVA waivers, or riders typically trade a bit of base rate for added flexibility.

Compare Fixed Annuity Rates by Term

Fixed annuity rates vary significantly by contract length. Today’s top 3-year MYGA yields sit around 5.0%-5.7%, while 10-year MYGAs can reach 6.5% or higher. The right term depends on your liquidity needs, retirement timeline, and whether you plan to ladder across multiple maturities instead of locking everything into one contract. Use the tabs below to compare the top rates for each common term, along with guidance on who each term fits best.

What 3-year annuity rates look like: The shortest MYGA term on this page, typically 5.0%-5.7% from A-rated carriers.

Best for: Savers who want near-term access, buyers using a 3-year as the first rung of a ladder strategy, or anyone uncertain about rate direction and unwilling to lock in longer.

Rates updated: May 13, 2026, 6:56 pm ET · Source: AnnuityRateWatch. Rates shown are for informational purposes only and subject to change without notice. Products marked SI use simple interest, effective compound yield is lower than the stated rate. Minimum premiums shown are for non-qualified (after-tax) funds. Always verify current rates with a licensed annuity professional before purchasing.

What 5-year annuity rates look like: The most popular term for a reason. Yields currently sit around 5.5%-6.3% and pair a competitive rate with a surrender schedule most buyers can commit to.

Best for: The sweet spot for typical retirement savers aged 55-70. Long enough to earn a meaningful yield premium over a 3-year, short enough that your money frees up before most retirement income plans start.

Rates updated: May 13, 2026, 6:56 pm ET · Source: AnnuityRateWatch. Rates shown are for informational purposes only and subject to change without notice. Products marked SI use simple interest, effective compound yield is lower than the stated rate. Minimum premiums shown are for non-qualified (after-tax) funds. Always verify current rates with a licensed annuity professional before purchasing.

What 7-year annuity rates look like: Often carries a 0.20%-0.40% premium over 5-year offers. Today’s top 7-year MYGA sits around 6.0%-6.5% from A-rated carriers.

Best for: Buyers 5-8 years from retirement who want to lock in current rates before their income phase begins. Also fits the middle rung of a 3/7/10 ladder.

Rates updated: May 13, 2026, 6:56 pm ET · Source: AnnuityRateWatch. Rates shown are for informational purposes only and subject to change without notice. Products marked SI use simple interest, effective compound yield is lower than the stated rate. Minimum premiums shown are for non-qualified (after-tax) funds. Always verify current rates with a licensed annuity professional before purchasing.

What 10-year annuity rates look like: The longest common MYGA term, and usually the highest headline yields on the board. Currently 6.3%-6.8% from select A- to A-rated carriers.

Best for: Pre-retirees and early retirees who can leave the money untouched for a decade and want the strongest guaranteed yield available. Works best when you won’t need principal access beyond the annual free withdrawal.

Rates updated: May 13, 2026, 6:56 pm ET · Source: AnnuityRateWatch. Rates shown are for informational purposes only and subject to change without notice. Products marked SI use simple interest, effective compound yield is lower than the stated rate. Minimum premiums shown are for non-qualified (after-tax) funds. Always verify current rates with a licensed annuity professional before purchasing.

Want to see how a specific investment grows? See our payout estimates: $200,000 | $250,000 | $300,000 | $400,000 | $750,000 | $1,000,000

Fixed Annuity Laddering Strategy

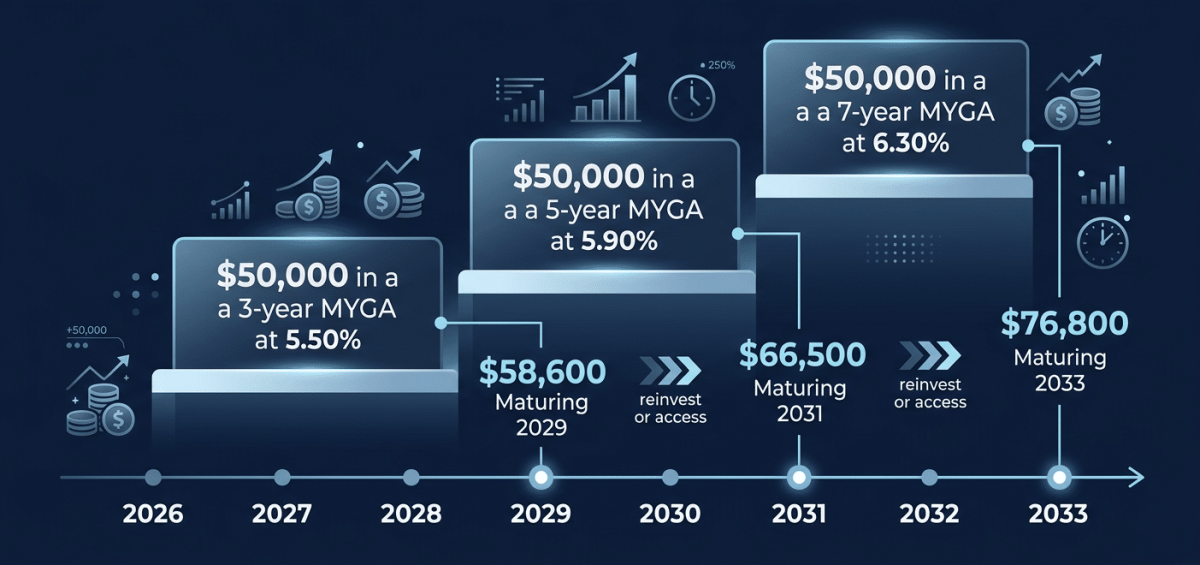

One of the smartest ways to maximize your fixed annuity returns while keeping flexibility is through a laddering strategy. Instead of buying a single annuity with one term length, annuity laddering involves splitting your investment across multiple fixed annuities with staggered maturity dates.

How It Works: A Real-Dollar Example

Say Jim, age 63, has $150,000 he wants to protect and grow in retirement. Instead of locking the entire amount into one 10-year annuity, he splits it into three equal contracts:

| Contract | Amount | Rate | Term | Matures |

|---|---|---|---|---|

| MYGA #1 | $50,000 | 5.50% | 3 years | 2029 |

| MYGA #2 | $50,000 | 5.90% | 5 years | 2031 |

| MYGA #3 | $50,000 | 6.30% | 7 years | 2033 |

When Jim’s first annuity becomes liquid in 2029, it will have grown to roughly $58,600. He can access this money penalty-free and reinvest, or roll it into a new annuity at whatever rates are available then. His other two contracts continue compounding tax-deferred, untouched.

Why It Makes Sense

The primary benefit of laddering is liquidity. Fixed annuities typically impose surrender charges if you withdraw funds before the contract term ends. By staggering your terms, you ensure that a portion of your money becomes accessible every few years.

Laddering also helps you manage interest rate risk. Buying a single long-term contract means you could miss out if rates rise significantly. With a ladder, your shorter-term contracts renew more often, allowing you to capture higher rates as they become available.

Who It’s Best For

This strategy works particularly well for retirees or near-retirees who want the safety and guaranteed growth of fixed annuities but don’t want their entire nest egg locked up for a decade or more. It balances the higher rates that come with longer terms against the peace of mind that comes with regular access to your money. For more side-by-side approaches, see our fixed annuity strategy comparisons.

How to Pick the Right Annuity Company

Fixed annuities are not FDIC insured. Your guarantee is only as strong as the insurance company behind it, which makes evaluating the carrier just as important as comparing rates. The three checks below cover what matters most.

1. Check the AM Best rating

AM Best is the gold standard for insurer financial strength. Sticking with carriers rated A- (Excellent) or better is a reasonable rule for the majority of your annuity allocation. B++ carriers often lead the rate tables, so know what premium you’re earning for the lower rating.

| AM Best Rating | What It Means | Typical Rate Premium vs. A-Rated |

|---|---|---|

| A+ / A++ (Superior) | Strongest financial position; long track record | Baseline (lowest rates) |

| A / A- (Excellent) | Very strong; broad product lines; well capitalized | +0.10% to +0.30% |

| B++ (Good) | Solid but less seasoned or smaller reserves; still investment grade | +0.40% to +0.80% |

| B+ or below | Adequate but carries more risk; proceed with caution | +0.80% or more |

Cross-check with S&P Global, Moody’s, or Fitch for confirmation. If one agency rates a carrier significantly lower than the others, dig into why.

2. Understand state guaranty association coverage

Every state has a guaranty association that covers policyholders if an insurer becomes insolvent. Coverage limits typically run $250,000-$500,000 per person, per carrier. If you’re investing more than your state’s limit with a single carrier, consider splitting between two companies. Check your state’s limit at NOLHGA.com.

3. Look past the headline rate

The highest rate means nothing if the contract has punishing surrender charges, a harsh MVA formula, or restrictive withdrawal provisions. See Understanding Surrender Charges below for how to read those terms.

For in-depth reviews of the top carriers, see our Best Fixed Annuity Companies rankings and individual carrier review pages.

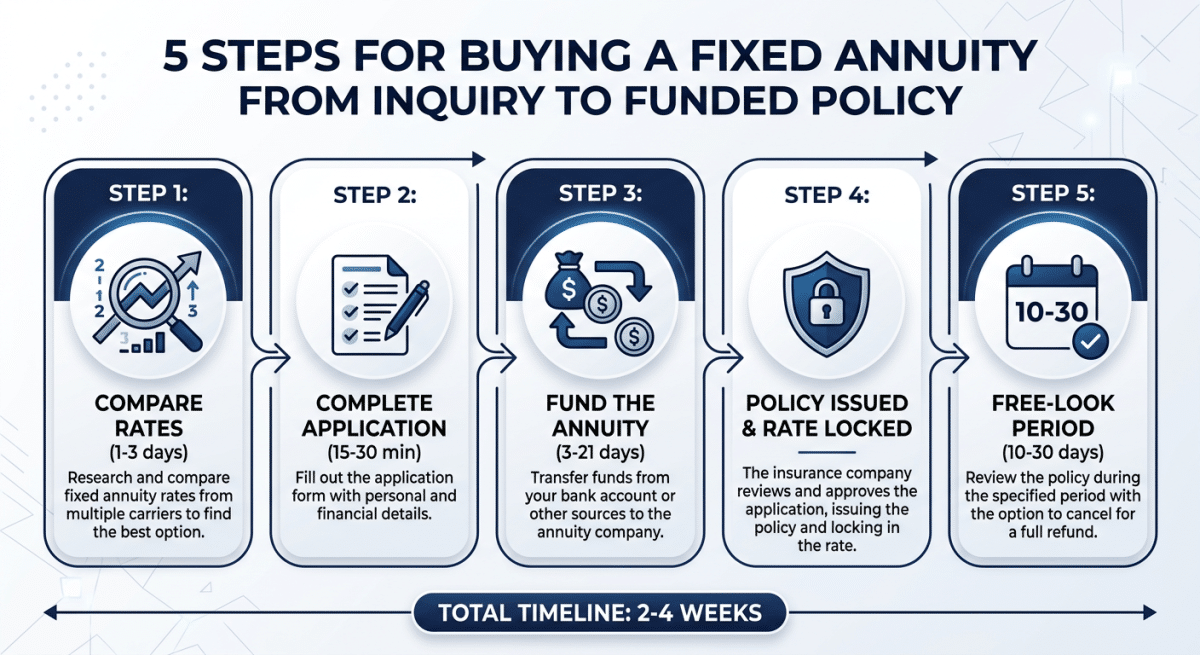

If you’ve never purchased an annuity before, the process can feel opaque. Here’s exactly what happens, step by step, based on thousands of applications we’ve processed:

Step 1: Compare rates and choose a product (1–3 days)

Use the rate table above to compare products. Narrow your options based on rate, term, carrier rating, and features (free withdrawals, MVA, minimum deposit). If you want help, call us or request a personalized rate report. We will match you with products for your situation.

Step 2: Complete the application (15–30 minutes)

Annuity applications are straightforward, typically 4–8 pages. You’ll provide basic personal information, beneficiary designations, and funding details. We pre-fill most of the paperwork and walk you through each section. Many carriers now accept electronic signatures, so you can complete the entire process from home.

Step 3: Fund the annuity

You can fund a fixed annuity with:

- A personal check or wire transfer from a bank account

- A 1035 exchange from an existing annuity or life insurance policy (tax-free)

- A direct rollover from a 401(k), 403(b), or IRA (tax-free if done correctly). See our IRA to fixed annuity rollover guide for the complete transfer process.

Transfers and rollovers typically take 10–21 business days. Direct funding via check or wire is faster, usually 3–5 business days.

Step 4: Policy issue and rate lock

Once the carrier receives your application and funds, they issue the policy. Your guaranteed rate locks in on the date your money is received (not the date you signed the application). Most carriers issue policies within 1–5 business days of receiving funds.

Step 5: Free-look period (10–30 days)

Every state requires a free-look period after your policy is issued, typically 10 to 30 days depending on your state and age. During this time, you can cancel the contract and receive a full refund of your premium, no questions asked. Think of it as a “test drive” period.

Total timeline: From first inquiry to funded policy, most of our clients complete the process in 2–4 weeks. 1035 exchanges and rollovers may take slightly longer due to the releasing company’s processing time. For a deeper walkthrough of each stage, see our how to buy a fixed annuity guide.

What Happens When Your Fixed Annuity Matures?

One of the most common questions we hear from first-time annuity buyers is: “What happens when my term is up?” It’s a fair question, and the answer is more flexible than most people expect.

When your fixed annuity reaches the end of its guarantee period, you typically have four options:

Option 1: Renew with the same carrier

Most insurers will offer a renewal rate for another term. This rate will reflect current market conditions, it could be higher or lower than your original rate. You’ll usually have a 30-day window to decide. If you don’t take action, many contracts automatically renew at a lower “renewal rate” for a 1-year period. Don’t let this happen by default, always review your options before the term expires.

Option 2: Transfer to a new annuity via a 1035 exchange

If another carrier is offering a better rate, you can move your funds tax-free using a 1035 exchange (named after Section 1035 of the Internal Revenue Code). No taxes are triggered on the transfer. This is one of the most common moves at maturity, and we handle the paperwork for our clients at no cost.

Option 3: Take a lump-sum withdrawal

You can withdraw the full account value, your original premium plus all accumulated interest. You’ll owe ordinary income tax on the gains (but not on your original deposit, your cost basis, since that was already taxed). If you’re over 59½, there’s no IRS penalty.

Option 4: Annuitize for guaranteed lifetime income

You can convert your account value into a stream of monthly, quarterly, or annual income payments. The payout depends on your age, gender, account value, and the payment option you choose (life only, life with period certain, joint life, etc.). Once annuitized, you generally can’t change the terms, so this works best for people who want predictable income and don’t need a lump sum.

Our recommendation: Start thinking about your maturity options 60–90 days before your term ends. We send maturity reminders to every client and provide updated rate comparisons so you can make an informed decision. Already own an annuity nearing maturity? Request a free annuity review and we’ll compare your renewal rate against the full market.

Understanding Surrender Charges: What You’ll Pay for Early Access

Surrender charges are the trade-off for the higher rates that fixed annuities offer. The carrier guarantees your rate for the full term, and in return, they expect your money to stay put. If you withdraw more than the free amount during the surrender period, you’ll pay a penalty.

Here’s what typical surrender charge schedules look like across different term lengths:

| Year | 3-Year MYGA | 5-Year MYGA | 7-Year MYGA | 10-Year MYGA |

|---|---|---|---|---|

| Year 1 | 7% | 8% | 9% | 9% |

| Year 2 | 6% | 7% | 8% | 9% |

| Year 3 | 5% | 6% | 7% | 8% |

| Year 4 | 0% | 5% | 6% | 7% |

| Year 5 | – | 0% | 5% | 6% |

| Year 6 | – | – | 4% | 5% |

| Year 7 | – | – | 0% | 4% |

| Year 8–10 | – | – | – | 3% → 0% |

These are representative schedules. Actual charges vary by product. Always review the specific surrender schedule in your contract illustration.

What most people don’t realize: Most MYGAs include a 10% annual free withdrawal provision starting in year one or year two. This means you can pull out up to 10% of your account value each year without triggering any surrender charge. That’s $10,000 on a $100,000 annuity, enough to cover many unexpected expenses.

Some contracts also waive surrender charges entirely for:

- Terminal illness (most carriers)

- Nursing home or long-term care confinement (many carriers, after a waiting period)

- Death, your beneficiary receives the full account value with no surrender charge

- Required Minimum Distributions (RMDs), if the annuity is inside a qualified account like an IRA

Is Now a Good Time to Buy a Fixed Annuity?

The short answer: Fixed annuity rates sit near 15-year highs. The top 5-year MYGA today pays 6.30%, compared to just 2.75% at the 2020 low. Locking in at these levels makes sense for most buyers 5-10 years from retirement.

Rates have tripled from the COVID-era lows. Insurance companies price MYGAs off Treasury yields, so when the Federal Reserve hiked rates aggressively in 2022-2023, MYGA rates followed. That elevated window has held through 2025 and into 2026, but whether it stays open depends on what happens next with the Fed.

Risk of waiting

If the Fed cuts rates or Treasury yields soften, MYGA rates could fall before you act. You’d lock in at a lower rate than today’s.

Risk of buying now

Rates could climb further, leaving early buyers wishing they’d held off a quarter. But rates have held near 15-year highs for 3+ years.

Bottom line:

- Don’t try to time the exact peak. Focus on whether today’s rate fits your plan.

- If you’re 5-10 years from retirement and want guaranteed growth, today’s rates make the decision easier than it was in 2020.

- Worried about rate direction either way? Ladder across 3, 5, and 7-year MYGAs instead of committing everything to one contract.

- What matters isn’t capturing the absolute top. It’s whether the annuity supports your plan with the certainty and liquidity you need.

Who Should Consider a Fixed Annuity?

A fixed annuity may be worth considering for people who want guaranteed growth without market risk. These products tend to appeal most to retirees, pre-retirees, and conservative savers who want to protect principal while earning a predictable return.

You may want to consider a fixed annuity if you:

- Are nearing retirement and want to reduce volatility

- Want a portion of your savings in a guaranteed product

- Are comparing annuities to CDs or bonds

- Want tax-deferred growth

- Do not need immediate access to all of the money

- Value stability over market upside

Fixed annuities are often used to:

- Preserve retirement assets

- Create a safe accumulation bucket

- Diversify away from market exposure

- Position money for future income planning

- Lock in attractive rates when available

They are not the right fit for every dollar you own. But for the right portion of a retirement portfolio, a fixed annuity can offer a level of predictability that is difficult to find elsewhere. If you want some exposure to market upside with downside protection, compare today’s best fixed index annuity rates.

How We Source Our Fixed Annuity Rates

My Annuity Store sources its fixed annuity rates (MYGA rates) through Annuity Rate Watch, a third-party annuity data provider. We connect to Annuity Rate Watch via a secure API. It is this technology that enables us to display annuity rates from so many annuity companies.

How often are annuity rates updated?

Rates on this page are refreshed automatically every 6 hours. Insurance companies can change their rates at any time, and there may be short delays between a carrier’s internal rate change and when it appears here. Before you purchase, we will verify the current rate directly with the carrier.

What we compare

When evaluating products, we look at a range of factors that may include current credited rate, contract term, insurer financial strength, surrender schedule, minimum premium, and product availability. Because annuity rates can change without notice, the rates shown on this page should be treated as current examples rather than a guarantee of future availability.

Availability and limitations

Not all annuity products or rates are available in every state or for every client. Actual rates and product options may vary based on your state of residence, premium amount, issue age, and product selection.

Our role and compensation

My Annuity Store, Inc. is an independent annuity brokerage. If you choose to purchase an annuity through us, we are paid a commission by the issuing insurance company. This compensation does not reduce your credited rate, account value, or annuity guarantees. For a full breakdown of how annuity compensation works, see annuity fees and commissions explained.

Our goal is to make fixed annuity shopping easier by presenting competitive options in a format that helps you compare rates, terms, and insurer quality more clearly. If you want help reviewing current availability or narrowing the list to products that fit your goals, we can help you compare your best options. For full disclosures, please see the Disclosures section at the bottom of this page.

Have Questions? Talk to a Licensed Advisor

Our advisors compare 90+ top annuity companies at no cost to you. No obligation, no pressure.

Frequently Asked Questions

What are fixed annuity rates and how are they determined?

Fixed annuity rates (often called MYGA rates for Multi-Year Guaranteed Annuities) are the guaranteed interest rates insurers credit for a set term (e.g., 3, 5, 7, 10 years). Insurers set these rates based on portfolio yields, prevailing Treasury and corporate bond yields, product features, and capital requirements.

Tip: Higher rates often come with longer terms or stricter liquidity. Always review surrender schedules and any Market Value Adjustment (MVA).

What’s the difference between a fixed annuity and a MYGA?

A fixed annuity is a broad category. A MYGA is a type of fixed annuity that guarantees a level interest rate for a specific multi-year term. Other fixed annuities (like traditional fixed or fixed indexed annuities) have different crediting methods and features.

- MYGA: simple, CD-like guaranteed rate for 3-10 years.

- Traditional fixed: insurer declares rates periodically (may change after first year).

How often do fixed annuity rates change?

Fixed annuity rates can change at any time based on market conditions and insurer pricing. Most carriers update weekly or monthly, but changes can occur intra-month when yields move. We monitor and update rates on business days.

Always confirm the rate on the date your application is signed and received by the carrier.

Are fixed annuities safe?

Fixed annuities are backed by the claims-paying ability of the issuing insurer. Safety is evaluated using independent ratings (A.M. Best, S&P, Moody’s, Fitch). Higher ratings generally indicate stronger financial strength but may correlate with slightly lower headline rates.

- Check A.M. Best rating and Comdex score (e.g., A, A-, B++).

- Review company history, statutory reserves, and recent outlooks.

- Understand state guaranty association protections (limits vary by state; not FDIC).

What is a Market Value Adjustment (MVA)?

An MVA adjusts your surrender value (up or down) if you withdraw more than the free amount during the surrender period. If interest rates have risen since purchase, an MVA can reduce the value; if rates have fallen, it can increase it. MVA does not affect your guaranteed interest if you hold to term and stay within free withdrawal limits.

Can I withdraw money from a fixed annuity without penalty?

Most MYGAs allow annual free withdrawals (often 10% of account value) after the first year. Fixed annuities without free withdrawal options often offer higher fixed annuity rates.

How do fixed annuity rates compare to CD rates?

Guaranteed interest rates offered by fixed annuities are often higher than CD rates, and MYGA interest grows tax-deferred while CD interest is taxable each year. On a 5-year term today, top MYGAs run about 1.0%-1.5% above the best 5-year bank CD rates. See our full comparison at MYGA vs CD: rates, taxes, and growth.

Sources & Citations

We regularly update this page and cite primary sources, carrier filings, and regulator guidance:

- NAIC. “Buyer’s Guide for Deferred Annuities.” naic.org

- FINRA. “Investor Education: Annuities.” finra.org

- FDIC Deposit Insurance: Know Your Risk. FDIC

- IRS Publication 575 (2024), Pension and Annuity Income. IRS Publication 575