Rolling an IRA into a fixed annuity means transferring your existing IRA funds to an insurance company, which then guarantees a fixed interest rate for a set period, typically 3 to 10 years. The money stays inside the IRA wrapper, so no taxes are due at the time of the transfer.

This is one of the most common uses of a multi-year guaranteed annuity (MYGA). The annuity earns a fixed rate while your money grows tax-deferred, the same as it did in your previous IRA account.

What Is a Fixed Annuity IRA Rollover?

A fixed annuity IRA rollover is a transfer of funds from an existing IRA to a fixed annuity contract that is set up as an IRA. The annuity becomes the new IRA, replacing whatever account held the money before.

The most common version is a traditional IRA rolling into a MYGA. You get a guaranteed interest rate for a specific number of years, and all growth remains tax-deferred until you withdraw. If you hold a Roth IRA, the same process applies, and qualified withdrawals remain tax-free.

Why Do People Roll IRAs Into Fixed Annuities?

The main reason is rate. As of May 2026, the best MYGA rates range from around 5.20% to 6.50% depending on the term, which is well above what most money market IRAs and bank savings accounts pay. Locking in a guaranteed rate for 3 to 7 years appeals to people who want predictable growth without stock market risk.

A second reason is simplicity. Once the money is in a MYGA, you do not need to monitor it or make investment decisions. The rate is locked, the principal is protected, and the account grows on a set schedule.

Many people also use a MYGA IRA rollover as part of a broader income strategy. They lock a portion of their savings into a guaranteed rate now, then reassess when the term ends. If rates are still attractive, they roll into another MYGA. If income is needed, they move to an income annuity or begin systematic withdrawals.

Which IRAs Can Be Rolled Into a Fixed Annuity?

The following IRA types can be rolled into a fixed annuity without triggering taxes:

- Traditional IRA – The most common rollover. Money moves from one tax-deferred account to another. No taxes owed at the time of transfer.

- Roth IRA – Funds move from a Roth IRA to a Roth annuity IRA. Growth remains tax-free, and qualified withdrawals are not taxed.

- SEP IRA – Self-employed individuals and small business owners can roll SEP IRA funds into a fixed annuity without tax consequences.

- SIMPLE IRA – Eligible after a 2-year participation period. Rollovers before that window may trigger a 25% penalty rather than the standard 10%.

- Rollover IRA – Funds previously rolled from a 401(k) or 403(b) can move into a fixed annuity IRA without tax consequences.

You cannot roll a 401(k) directly into a fixed annuity without first moving the funds to a traditional IRA, unless the plan permits in-service distributions. For most people, the correct sequence is: 401(k) to rollover IRA, then rollover IRA to MYGA. Read our 401(k) rollover guide for the full process on that first step.

Direct Rollover vs. 60-Day Rollover: Which Should You Use?

A direct rollover, also called a trustee-to-trustee transfer, is almost always the right choice. The funds move directly from your current IRA custodian to the new annuity company. You never receive a check, so there is no risk of missing the 60-day deadline and no withholding issue.

A 60-day rollover puts a check in your hands. You have 60 days to deposit the full amount into the new IRA. If you miss the deadline, the IRS treats the distribution as taxable income and, if you are under age 59.5, adds a 10% early withdrawal penalty. You are also limited to one 60-day rollover per 12-month period across all your IRAs combined.

There is no good reason to use the 60-day method for a planned rollover. The direct transfer is simpler, safer, and does not count toward the once-per-year rollover limit.

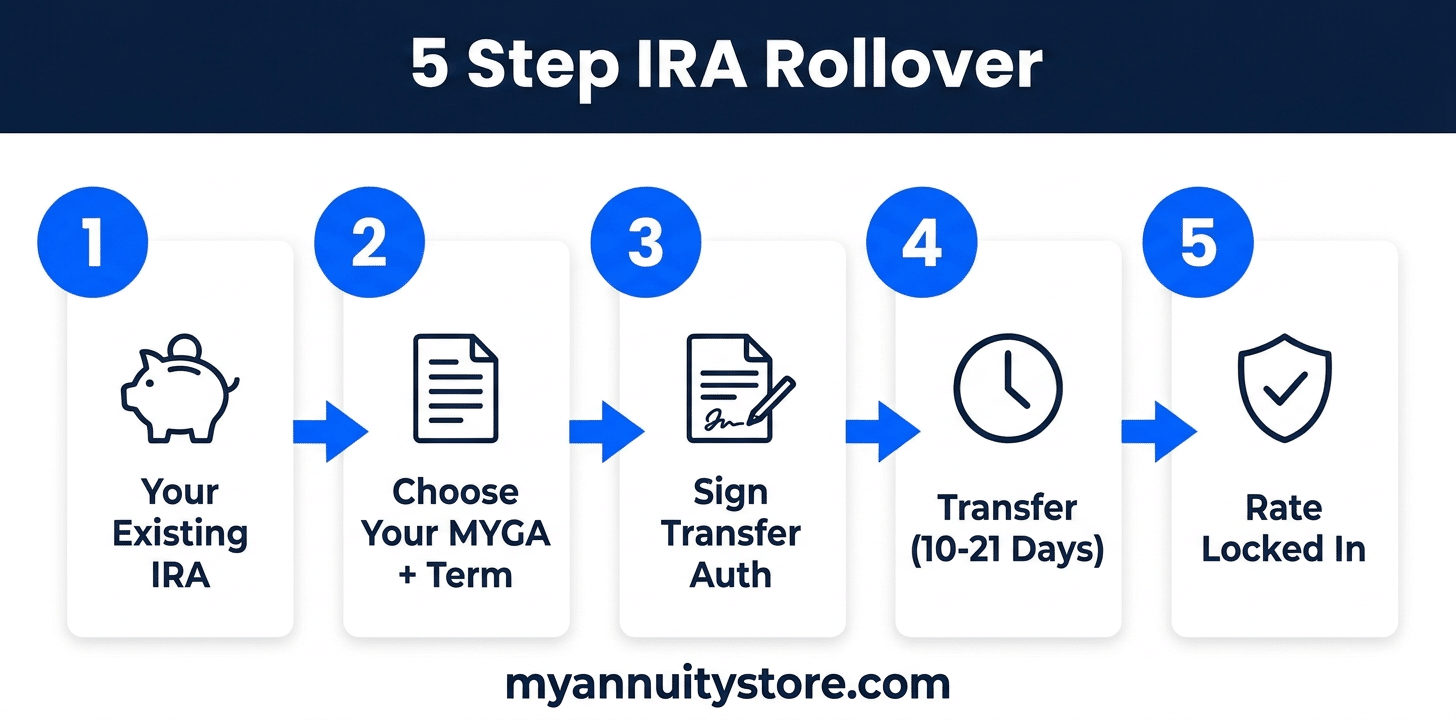

How to Roll an IRA Into a Fixed Annuity: Step by Step

The process is straightforward. Most people complete it in 2 to 4 weeks.

Step 1: Choose your annuity and term. Review current fixed annuity rates and decide on a term that fits your timeline. If you need the money in 5 years, a 5-year MYGA makes sense. A 7-year term often pays a higher rate if you can commit the money longer.

Step 2: Complete the annuity application. The annuity company sets up the contract as a traditional IRA (or Roth IRA, depending on your source account). You designate beneficiaries and provide your current IRA custodian’s account information.

Step 3: Sign the transfer authorization. Most annuity companies send a transfer form directly to your current IRA custodian. This authorizes the release of your funds. You do not receive a check at any point in the process.

Step 4: Wait for the transfer to complete. Most IRA transfers take 10 to 21 business days. Some custodians process faster. Once your funds arrive at the annuity company, your rate locks in and your contract goes into effect.

Step 5: Receive your policy and review it. Your free-look period begins when you receive the contract, typically 10 to 30 days depending on your state. During this window, you can cancel and receive a full refund if the contract does not meet your expectations.

What Are the Tax Rules for an IRA Fixed Annuity Rollover?

When the rollover is done correctly as a direct transfer, there are no taxes due at the time of the move. The funds shift from one IRA to another, and the annuity takes on the same tax status as the account it came from.

With a traditional IRA fixed annuity, growth is tax-deferred. You pay ordinary income tax when you make withdrawals in retirement. Required minimum distributions (RMDs) still apply starting at age 73, the same as with any traditional IRA.

With a Roth IRA fixed annuity, growth is tax-free and qualified withdrawals are not taxed. Roth IRAs do not have RMDs during the owner’s lifetime, which gives you more flexibility on timing.

One point to note: annuities held inside IRAs do not provide extra tax-deferred growth beyond what the IRA already offers. The annuity’s value in this context is the guaranteed rate, the principal protection, and the structured term. That said, there is no downside to holding a MYGA inside an IRA if the rate is competitive.

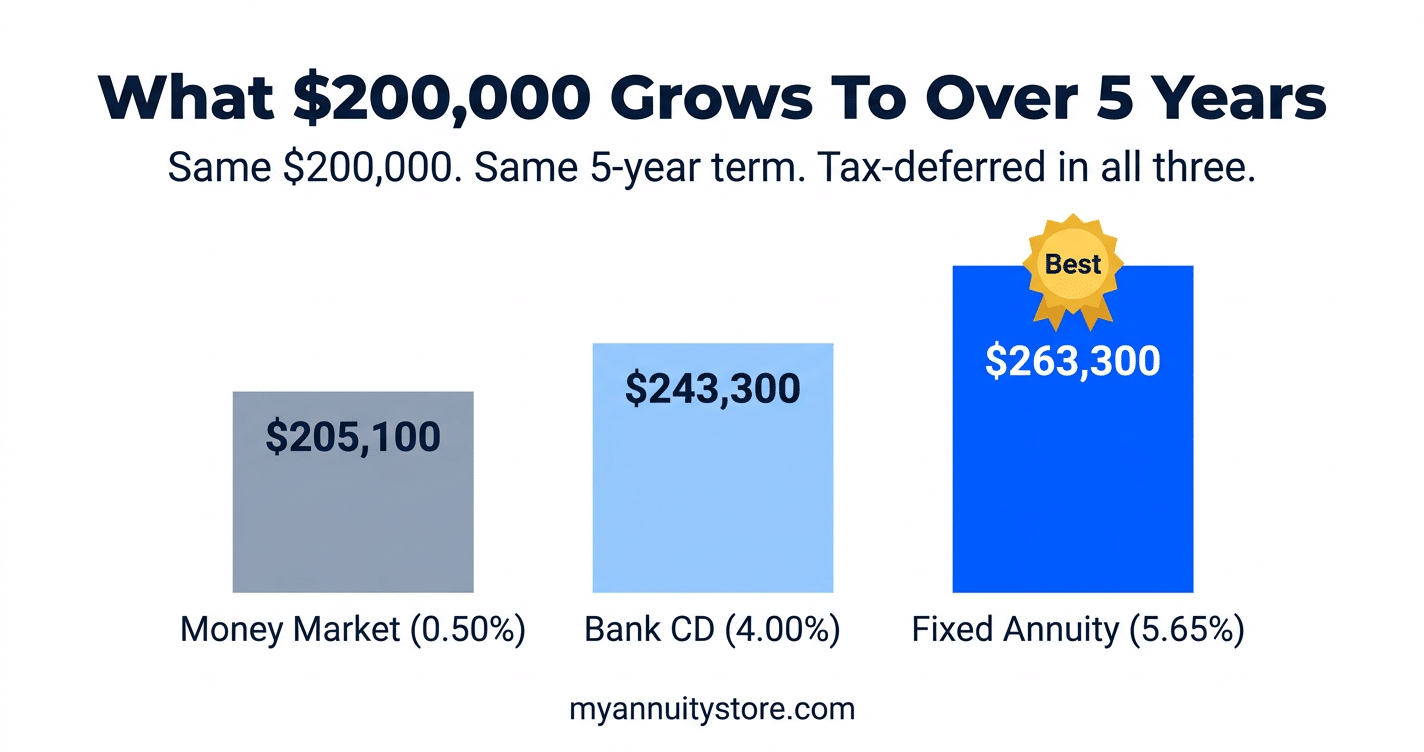

How Much Can You Earn Rolling an IRA Into a Fixed Annuity?

Take a real example. Susan, age 63, has $200,000 in a traditional IRA sitting in a money market account earning 0.50% annually. She rolls it into a 5-year MYGA at 5.65%.

After 5 years, her MYGA balance is approximately $263,300. In the money market, the same $200,000 would have grown to roughly $205,100. The fixed annuity produces about $58,200 more, and all growth remains tax-deferred until she makes withdrawals.

The comparison also holds up against a bank CD. If the best 5-year CD pays 4.00%, $200,000 grows to roughly $243,300. The MYGA at 5.65% still comes out about $20,000 ahead over the same term. Inside an IRA, both accounts grow tax-deferred, so the rate difference is the key variable.

See current offers on our fixed annuity rates page to compare live rates by term and carrier.

Pros and Cons of Rolling Your IRA Into a Fixed Annuity

Pros

- Guaranteed rate. Your return is locked in regardless of what interest rates do during your term.

- Principal protection. Fixed annuities do not lose value due to market movement.

- No contribution limits for rollovers. You can roll any amount from an existing IRA. This is a transfer, not a new contribution.

- Predictable growth. You know exactly what your balance will be at maturity before you sign.

- RMD-friendly. Most MYGAs allow penalty-free withdrawals to satisfy required minimum distributions.

Cons

- Surrender charges for early access. Withdrawing more than the free amount during the term triggers a penalty. Most MYGAs allow 10% annual free withdrawals, but larger amounts cost extra.

- RMDs still required. If you hold a traditional IRA MYGA, RMDs are required starting at age 73. Confirm that the contract allows penalty-free RMD withdrawals before you apply.

- Rate lock can work against you. If rates rise significantly after you lock in, you are stuck at your original rate until the term ends.

- No upside beyond the stated rate. If markets outperform, you will not participate.

Who Should Consider an IRA Fixed Annuity Rollover?

A fixed annuity IRA rollover works best for people who want guaranteed growth and cannot afford a significant loss. If you are within 5 to 10 years of needing the money for retirement income, a MYGA offers stability that stocks and bonds do not provide.

It also makes sense for people who are uncomfortable leaving IRA money in low-yield savings accounts or money market funds. If your IRA is sitting in cash earning under 1%, rolling into a MYGA at current rates is a straightforward upgrade with no added risk to principal.

It is generally not the right move for someone in their 40s with a 20-year horizon who can absorb market volatility. At younger ages, growth-oriented investments tend to outperform over long periods. The MYGA’s value is in the guarantee, not the maximum possible return.

Browse top-rated fixed annuity companies to compare carriers, financial strength ratings, and current rates before deciding. Or request a free quote and we will match you with the best options for your IRA amount and timeline.

Frequently Asked Questions

Can I roll my entire IRA into a fixed annuity?

Yes. There is no limit on how much you can roll from an existing IRA into a fixed annuity. This is a transfer between retirement accounts, not a new contribution, so annual contribution limits do not apply.

Is there a penalty for rolling an IRA into a fixed annuity?

No, as long as you use a direct rollover. The funds move from your current IRA custodian directly to the annuity company. There are no taxes and no IRS penalties when the transfer is handled correctly.

Do I have to take RMDs from an annuity IRA?

Yes, if it is a traditional IRA. Required minimum distributions begin at age 73 under current law. Most fixed annuities allow penalty-free withdrawals to satisfy RMDs. Confirm this with the carrier before you apply.

Can I roll a Roth IRA into a fixed annuity?

Yes. The annuity is set up as a Roth IRA. Growth and qualified withdrawals remain tax-free. Roth IRAs do not have RMDs during the owner’s lifetime.

What happens at the end of my MYGA term?

At maturity, you typically have three options: renew into a new term at the current rate, roll the funds into a different annuity or IRA, or begin taking withdrawals. Most carriers offer a 30-day window at maturity during which you can move funds without surrender charges.

Sources & Citations

- IRS Publication 590-A – Contributions to Individual Retirement Arrangements. Covers rollover rules, transfer rules, and eligibility requirements for all IRA types.

- IRS IRA Rollover FAQs – Official guidance on the once-per-year rollover rule, the 60-day deadline, and tax treatment of IRA distributions.

- FINRA: Annuities – Overview of annuity types, features, and investor considerations from the Financial Industry Regulatory Authority.

- National Association of Insurance Commissioners (NAIC) – State regulatory guidance on annuity products and consumer protections.

- U.S. Department of Labor – IRA rollover rules and fiduciary guidance for retirement account transfers.