What Exactly Is a Fixed Annuity?

A fixed annuity is an insurance product that guarantees your money will grow at a set interest rate and protects your principal from market losses. Unlike variable annuities, where your returns depend on how the stock market performs, a fixed annuity puts the investment risk on the insurance company — not you. Your account value cannot go down because of a bad quarter on Wall Street.

But “fixed annuity” is broader than most people realize. It is not one product — it is a category of products. Some fixed annuities are designed to grow your money over a set period. Others convert a lump sum into guaranteed income that lasts for life. One type even ties your interest to a market index while still protecting your principal. Understanding which type does what is the first step toward choosing the right one.

All guarantees in a fixed annuity are backed by the claims-paying ability and financial strength of the issuing insurance company — not the federal government and not the FDIC. Fixed annuities are regulated at the state level by insurance departments, not by the SEC (which oversees variable annuities and securities). The National Association of Insurance Commissioners (NAIC) provides consumer resources on how annuity regulation works across all 50 states.

What Can a Fixed Annuity Do for You?

Regardless of which type you choose, every fixed annuity offers three core benefits:

- Tax-deferred growth. Your money grows faster because you do not pay taxes on earnings until you actually withdraw them or receive income payments. This compounding advantage is the single biggest edge fixed annuities have over bank CDs, where interest is taxed every year.

- Guaranteed income that can last for life. When you are ready, a fixed annuity can provide monthly income payments guaranteed to continue as long as you live — no matter how long that is or what happens in the market.

- A way to transfer money to loved ones. If you pass away before taking all your money out, the remaining value goes to the beneficiary you named on the contract — bypassing probate entirely.

Who Is Who in an Annuity Contract?

Before looking at the different types, it helps to understand the parties involved in any annuity contract. How you structure these roles affects your income payments, tax treatment, and what happens to the money when someone passes away.

- Insurance company. The company that issues the contract, manages the money, and guarantees the interest rate and income payments.

- Owner. The person (or entity, like a trust) who purchases the annuity and controls the contract. The owner chooses the annuity type, terms, and beneficiaries. The owner also decides when to take withdrawals, make changes, or surrender the contract.

- Annuitant. The person whose age, life expectancy, and gender are used to calculate annuity payments. The owner and annuitant are often the same person, but they do not have to be. The annuitant receives the income payments when the contract is annuitized.

- Beneficiary. The person or entity who receives the remaining value if the owner or annuitant dies before all benefits have been paid. This is a detail that is surprisingly overlooked — if you do not name a beneficiary, the money goes to your estate and may be subject to probate court. Beneficiaries can generally be changed at any time, so keep this information current.

What Happens to a Fixed Annuity When You Die?

If you pass away before you begin receiving lifetime income or any other annuity payout option, your named beneficiary typically receives the full contract value — the premiums you paid plus all accumulated interest. This transfer happens outside of probate, which is one reason naming a beneficiary matters so much.

There is one important difference between an annuity death benefit and a life insurance death benefit: life insurance proceeds are generally income-tax-free to the beneficiary, but annuity proceeds are not. The taxable portion of the beneficiary benefit — the earnings above your original premium — is subject to ordinary income tax when the beneficiary receives it. The portion that represents a return of your original principal is not taxed.

For example, if you contributed $100,000 to a MYGA and it grew to $125,000 before you passed away, your beneficiary would receive the full $125,000. The $25,000 in earnings would be taxable as ordinary income. The $100,000 in original principal would not be taxed.

Beneficiary options vary by contract type. Some deferred annuities allow your beneficiary to take the full amount as a lump sum, spread it over five years, or continue the contract. SPIAs and DIAs with a “period certain” or “cash refund” feature guarantee that if you die before receiving payments equal to your premium, the remaining balance goes to your beneficiary. A “life only” SPIA with no refund feature, however, pays nothing to beneficiaries after the annuitant dies — all payments stop. This is the tradeoff for the highest monthly payout.

What Are the Types of Fixed Annuities?

There are five main types of fixed annuities, divided into two groups: those designed to accumulate money (deferred) and those designed to distribute money as income.

Deferred Fixed Annuities (Accumulation)

Deferred fixed annuities grow your money at a guaranteed interest rate while you save for retirement. You are deferring — waiting to take income later. All three types below protect your principal and offer tax-deferred growth.

1. Traditional Fixed Annuity (Declared-Rate)

A traditional fixed annuity guarantees an interest rate for an initial period — usually one to three years. After that, the insurance company declares a new rate each year at their discretion. Every contract includes a guaranteed minimum interest rate (often 1.00% to 3.00%) that the insurer can never go below, no matter what.

The renewal rate the carrier actually credits each year can be anywhere between that minimum floor and whatever they choose to declare. Some carriers have strong track records of crediting rates well above the minimum. Others let rates drift toward the floor. This makes traditional fixed annuities less predictable than MYGAs but more flexible — many are flexible-premium, meaning you can add money over time rather than committing a single lump sum.

Traditional fixed annuities are a good fit if you want ongoing flexibility to add contributions and are comfortable with annual rate adjustments, especially if the carrier has a history of competitive renewals.

2. Multi-Year Guaranteed Annuity (MYGA)

A MYGA locks in a guaranteed interest rate for a specific term — typically 3, 5, 7, or 10 years. Your rate does not change during the term. Period. At maturity, you can withdraw the full balance, roll into a new MYGA at current rates, or exchange into a different annuity type via a tax-free 1035 exchange.

MYGAs are single-premium products — you fund them with one lump sum, not ongoing contributions. They are the closest annuity equivalent to a bank CD, but with higher rates and tax-deferred compounding. In 2026, top 5-year MYGA rates are running between 5.00% and 5.55%, roughly 0.50% to 0.75% above the best bank CDs.

MYGAs are the most popular type of fixed annuity sold today. According to LIMRA’s 2024 annuity sales report, MYGA sales reached record highs driven by the elevated interest rate environment. For a deep dive into how MYGAs work, current rates, and who they are best for, see our complete MYGA guide.

3. Fixed Index Annuity (FIA)

A fixed index annuity is a type of fixed annuity that credits interest based on the performance of a market index — such as the S&P 500 — rather than a rate declared by the insurer. Your principal is fully protected: if the index goes down, your account value does not. But your upside is limited by caps, participation rates, or spreads set by the carrier.

In a good year, an FIA may credit 4% to 8% depending on the index performance and the contract terms. In a bad year, you earn 0% — not a loss, just no gain. This puts FIAs between traditional fixed annuities and variable annuities on the risk-and-reward spectrum. You give up some potential upside in exchange for a guarantee that you cannot lose principal.

FIAs are more complex than MYGAs or traditional fixed annuities because the crediting methods (annual point-to-point, monthly averaging, participation rates, caps) vary widely between carriers. They also tend to have longer surrender periods — often 7 to 10 years. For a complete breakdown, see our fixed index annuity guide.

Fixed Income Annuities (Distribution)

Fixed income annuities convert a lump sum into guaranteed income payments. Instead of accumulating money, you are spending it down in a controlled, predictable way that you cannot outlive.

4. Single Premium Immediate Annuity (SPIA)

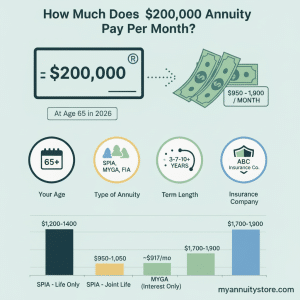

A SPIA converts a single lump-sum payment into guaranteed income that begins within 12 months of purchase — usually within 30 days. You hand the insurance company a premium, and they pay you a fixed amount every month (or quarter, or year) for a period you choose: 5 years, 10 years, 20 years, or for the rest of your life.

SPIAs are the original annuity — the word “annuity” literally means a series of payments. They are ideal for retirees who need predictable monthly income to cover essential expenses regardless of what the stock market does. A 65-year-old man investing $200,000 in a life-only SPIA might receive roughly $1,200 to $1,350 per month for life, depending on current rates and the carrier.

The tradeoff: once you purchase a SPIA, the decision is generally irrevocable. The money is converted into income, and you typically cannot get your lump sum back. Some SPIAs offer a “cash refund” or “period certain” option that guarantees your heirs receive at least your original premium if you die early, but these options reduce the monthly payment. For more on how SPIAs work, see our income annuity guide.

5. Deferred Income Annuity (DIA)

A deferred income annuity works like a SPIA with a delayed start date. You pay a lump sum now, but income payments do not begin for 2 to 40 years. The longer you defer, the larger each payment becomes — because the insurance company has more time to invest your premium before they start paying you.

DIAs are sometimes called “longevity annuities” because they protect against the risk of running out of money late in retirement. A 55-year-old who buys a DIA with payments starting at age 75 will receive a dramatically higher monthly payout than if they bought a SPIA at 75 — because the insurer had 20 years to grow the premium.

A specific type of DIA called a Qualified Longevity Annuity Contract (QLAC) can be purchased inside an IRA or 401(k) with up to $200,000 of qualified money. The IRS finalized the SECURE 2.0 Act rules in 2024, eliminating the old 25%-of-account-balance cap and setting the flat $200,000 limit. QLACs are exempt from required minimum distributions (RMDs) until payments begin, which can be deferred to as late as age 85. This makes them useful for reducing taxable RMDs in your early retirement years.

How Do These Five Types Compare?

| Feature | Traditional Fixed | MYGA | Fixed Index (FIA) | SPIA | DIA |

|---|---|---|---|---|---|

| Primary purpose | Accumulation | Accumulation | Accumulation | Immediate income | Future income |

| How interest is credited | Declared rate, resets annually | Fixed rate for full term | Linked to market index (with floor) | Built into income payments | Built into income payments |

| Rate guarantee period | Year 1 (sometimes 2-3), then renewal | Full term (3-10 years) | Caps/rates reset annually | Fixed payout for life or period | Fixed payout once income starts |

| Premium type | Often flexible (add money over time) | Single premium only | Usually single premium | Single premium | Single premium |

| Can lose principal? | No | No | No | N/A (converted to income) | N/A (converted to income) |

| Access to lump sum | Yes, with surrender charges | 10%/yr free, full at maturity | 10%/yr free, full after surrender period | Generally no | Generally no |

| Typical surrender period | 5-10 years | 3-10 years (matches term) | 7-10 years | N/A | N/A |

| Best for | Flexible savers, ongoing contributions | CD-like savers, rate certainty | Growth seekers who want downside protection | Retirees needing income now | Pre-retirees planning future income |

Single-Premium vs. Flexible-Premium: What Is the Difference?

This is a distinction that cuts across all fixed annuity types:

- Single-premium means you fund the annuity with one lump-sum payment at purchase. MYGAs, SPIAs, and DIAs are almost always single-premium. You commit a set amount and the contract is built around that number.

- Flexible-premium means you can make an initial payment and then add more money over time. Many traditional fixed annuities and some FIAs offer this option. This is useful if you want to contribute regularly from income rather than committing a large sum all at once.

If you are rolling over a CD, a 401(k), or an IRA, a single-premium product works naturally — you already have the lump sum. If you are still working and want to build savings gradually with guaranteed growth, a flexible-premium traditional fixed annuity may be a better fit.

How Are Fixed Annuities Taxed?

Every fixed annuity — regardless of type — offers tax-deferred growth on non-qualified (after-tax) money. You do not pay income tax on interest or earnings until you take a withdrawal or receive a payment. Here is how the tax rules work depending on how the annuity is funded:

Non-Qualified (Funded with After-Tax Dollars)

- You only pay taxes on the earnings when you withdraw them. Your original premium comes back tax-free.

- Withdrawals from a deferred annuity (before annuitization) are taxed on a last-in, first-out (LIFO) basis. This means earnings come out first and are fully taxable. You do not get to your tax-free principal until all gains have been withdrawn.

- Income payments (after annuitization) are taxed using the exclusion ratio. Each payment is split into a taxable portion (earnings) and a non-taxable portion (return of your original premium). This means a portion of every income payment is tax-free for the life of the payout.

- Withdrawals before age 59½ trigger a 10% IRS early withdrawal penalty on the earnings portion, in addition to ordinary income tax. The IRS early distribution rules include limited exceptions (disability, substantially equal periodic payments under IRC Section 72(t), etc.).

- There are no government-imposed limits on how much you can contribute to a non-qualified annuity (though carriers may set their own limits).

Qualified (Funded via IRA or 401(k) Rollover)

- The entire withdrawal is taxable as ordinary income, since the original contribution was pre-tax.

- Tax deferral offers no additional benefit inside a qualified plan — the IRA or 401(k) already provides it. The reason to use a fixed annuity inside a qualified account is for the guaranteed rate, principal protection, and lifetime income options — not for extra tax savings.

- RMDs apply at age 73 for traditional IRAs (age 75 starting in 2033 under the SECURE 2.0 Act). Inside a Roth IRA, qualified withdrawals are tax-free.

- Contributions are subject to IRS contribution limits for the plan type.

For the full rules, see IRS Publication 575 on pension and annuity income.

The Tax Deferral Advantage in Dollars

Carol, age 58, rolls $150,000 from a maturing CD into a 5-year MYGA at 5.30%. Her federal tax bracket is 24%.

In a taxable CD at the same rate, Carol pays taxes on the interest every year. After tax, her effective annual return is 5.30% x (1 – 0.24) = 4.03%. After five years, $150,000 grows to approximately $183,100.

In the MYGA, interest compounds at the full 5.30% with no annual tax drag. After five years, $150,000 grows to approximately $194,700. When Carol withdraws and pays tax on the $44,700 in gains, she nets approximately $184,100 after tax — and that assumes she takes it all in a single year. If she spreads withdrawals over several years in lower tax brackets, the advantage widens further.

On $150,000 over five years, the tax deferral adds roughly $1,000 to $5,000 in after-tax wealth depending on her withdrawal strategy. It scales with the amount and duration.

Fixed Annuity vs CD vs Bond: How They Compare

| Feature | Fixed Annuity (MYGA) | Bank CD | Treasury Bond |

|---|---|---|---|

| Typical 5-year rate (2026) | 5.00% – 5.55% | 4.25% – 4.75% | ~4.40% |

| Principal protection | Yes (insurer backed) | Yes (FDIC up to $250K) | Yes (U.S. government) |

| Tax treatment on interest | Tax-deferred until withdrawal | Taxable every year | Federal taxable, state exempt |

| Early withdrawal penalty | Surrender charge schedule | Interest penalty (varies) | Market price fluctuation if sold early |

| Minimum deposit | $5,000 – $10,000 | $500 – $1,000 | $100 (TreasuryDirect) |

| 1035 exchange available | Yes | No | No |

| Can convert to lifetime income | Yes (annuitize or 1035 to SPIA) | No | No |

The MYGA rate advantage over CDs is consistent — typically 0.50% to 0.75% higher on equivalent terms from top-rated carriers. But the real differentiator is flexibility: a CD matures and you get cash. A fixed annuity matures and you can withdraw, roll to a new annuity, exchange into an income product, or begin lifetime payments — all without a taxable event if you use a 1035 exchange. See our MYGA vs CD comparison for the full analysis.

Surrender Charges: What You Need to Know

Surrender charges apply to deferred fixed annuities (traditional, MYGA, and FIA) during the contract’s surrender period. They compensate the insurer for investing your premium in longer-duration instruments to support your guaranteed rate. A typical 5-year schedule looks like this:

| Contract Year | Surrender Charge |

|---|---|

| Year 1 | 8% |

| Year 2 | 7% |

| Year 3 | 6% |

| Year 4 | 5% |

| Year 5 | 4% |

| After maturity | 0% |

Surrender charges apply only to withdrawals above the free withdrawal amount (usually 10% of account value per year). If you take your annual 10% and nothing more, you never pay a surrender charge.

Most deferred fixed annuities also include a premium waiver provision: if you are confined to a nursing home or diagnosed with a terminal illness, surrender charges are typically waived. For the full mechanics, see our guide to surrender charges.

SPIAs and DIAs do not have surrender charges in the traditional sense — because once you purchase them, your premium is converted into a guaranteed income stream. There is no account balance to “surrender.”

Are Fixed Annuities Safe?

Fixed annuities are not FDIC insured — they are products of insurance companies, not banks. But they are protected by a system with a strong track record.

Every state has a life and health insurance guaranty association that steps in if an insurer becomes insolvent. Coverage limits vary by state but are typically $100,000 to $500,000 per annuitant per carrier. The National Organization of Life and Health Insurance Guaranty Associations (NOLHGA.com) maintains a directory of all state guaranty associations and their coverage limits.

Beyond the guaranty association, carrier financial strength matters. AM Best ratings are the industry standard: look for A- or better. Carriers rated A+ — such as Allianz, Nationwide, and MassMutual — have the financial depth to honor guarantees through serious economic disruption. For deposits above the guaranty limit, spreading across two carriers from different parent companies is prudent. Coverage limits differ by state — check your state’s limits on our annuity rates by state page.

Read our full guide to annuity safety for a complete breakdown of how insurer protection works.

Who Is a Fixed Annuity Best For?

- Pre-retirees who cannot afford to lose principal. Within 5 to 10 years of retirement, principal protection removes the risk of a bad market year wiping out savings you cannot recover. See our retirement planning hub for strategies on building a guaranteed income floor.

- CD holders seeking better rates with tax deferral. If your CD is maturing and you do not need the money immediately, a MYGA offers a higher guaranteed rate with tax-deferred compounding. See our MYGA vs CD comparison for a detailed breakdown.

- Retirees who need guaranteed income. A SPIA or DIA converts savings into a paycheck you cannot outlive — regardless of market conditions or how long you live.

- Higher-bracket earners who want to control when they pay taxes. Deferring income from a fixed annuity until a lower-bracket retirement year is a legitimate and effective tax strategy.

- IRA holders who want guaranteed growth. A MYGA inside a traditional IRA adds a guaranteed rate and principal protection to money that is already tax-deferred.

- Savers with more than $250,000 at a single bank. FDIC insurance covers $250,000 per depositor per bank. A fixed annuity from an A-rated carrier backed by your state’s guaranty association lets you diversify beyond the FDIC limit.

Who Should NOT Buy a Fixed Annuity

- Anyone who may need the full amount before maturity. The 10% free withdrawal provision helps, but if there is a real chance you need all your money in year 2 or 3, keep it in a CD or high-yield savings account.

- Investors with a long time horizon and high risk tolerance. If you are 45, have 20 years before retirement, and can tolerate market swings, a low-cost equity index fund will almost certainly outperform a fixed annuity over that period.

- Anyone putting in their only liquid savings. Keep at least 6 to 12 months of living expenses in liquid accounts before tying up funds in any annuity.

How to Choose the Right Type of Fixed Annuity

- If you want to grow a lump sum at a guaranteed rate for a specific period: A MYGA is your best option. You know the rate, the term, and the maturity date before you sign.

- If you want flexibility to add money over time with guaranteed growth: A traditional fixed annuity lets you make ongoing contributions with a guaranteed minimum rate and annual renewal rates.

- If you want growth potential tied to the market without the risk of loss: A fixed index annuity gives you upside linked to an index with a 0% floor protecting your principal.

- If you need income starting now: A SPIA converts your lump sum into immediate guaranteed payments. No other financial product does this.

- If you want to guarantee income starting 5, 10, or 20 years from now: A DIA locks in a future income stream at today’s rates — and the longer you defer, the larger each payment.

- If you are not sure: Start with a MYGA. It preserves your options. At maturity, you can withdraw, renew, or 1035 exchange into a SPIA, DIA, or FIA without triggering taxes.

Not sure where to start? Our guide to buying an annuity walks through the process step by step, and our annuity company directory profiles the carriers behind these products. You can also browse the best fixed annuity companies ranked by rate competitiveness and financial strength.

Today’s Best Fixed Annuity Rates

MYGA rates change frequently as carriers adjust to the interest rate environment. The difference between the best and worst rate for the same term and credit quality can be 0.50% or more — meaningful on a $200,000 deposit over 5 years. For guidance on rate timing, see when is the best time to buy an annuity.

Rates shown are for informational purposes only and subject to change without notice. Products marked SI use simple interest — effective compound yield is lower than the stated rate. Minimum premiums shown are for non-qualified (after-tax) funds. Always verify current rates with a licensed annuity professional before purchasing.

See our full fixed annuity rate comparison for current rates across all terms and carriers, updated daily.

Fixed Annuity FAQ

What is the difference between a fixed annuity and a MYGA?

A MYGA is one type of fixed annuity. “Fixed annuity” is the broad category that includes MYGAs, traditional fixed annuities, fixed index annuities, SPIAs, and DIAs. All fixed annuities guarantee your principal. A MYGA specifically locks in a guaranteed interest rate for a set term (3 to 10 years), which is what makes it distinct from a traditional fixed annuity that resets the rate annually after the first year.

What is a traditional fixed annuity vs a MYGA?

A traditional fixed annuity guarantees your interest rate for the first year (sometimes 2-3 years), then the carrier declares a new rate each year going forward. The rate can never drop below the contract’s guaranteed minimum. A MYGA guarantees the rate for the entire term — 3, 5, 7, or 10 years — with no renewals or adjustments. Both protect your principal. The MYGA gives you rate certainty; the traditional fixed annuity offers more flexibility, including the ability to add money over time.

Is a fixed index annuity a type of fixed annuity?

Yes. A fixed index annuity (FIA) falls under the fixed annuity umbrella because it guarantees your principal — you cannot lose money due to market performance. The difference is how interest is credited: a traditional fixed annuity or MYGA pays a declared rate, while an FIA’s interest is linked to a market index like the S&P 500, subject to caps and participation rates. The principal protection makes it a fixed product; the index-linked crediting method makes it more complex.

Can I lose money in a fixed annuity?

You cannot lose principal due to market performance — the guarantee is contractual. You could lose a portion of interest if you surrender early and surrender charges exceed the earned interest, particularly in the first one to two years. In the unlikely event of an insurer failure, state guaranty associations provide a safety net. No annuity holder at an A-rated carrier has lost guaranteed principal in modern U.S. insurance history.

How much does a $100,000 fixed annuity earn?

It depends on the type. In a 5-year MYGA at 5.30%, $100,000 grows to approximately $129,600 by maturity — a gain of $29,600, all tax-deferred. In a SPIA, $100,000 for a 65-year-old man might generate roughly $600 to $680 per month for life. Use our fixed annuity calculator to model your specific situation.

Can I put a fixed annuity inside my IRA?

Yes. MYGAs and traditional fixed annuities are commonly funded with IRA or 401(k) rollover money. Inside a qualified account, the tax deferral is redundant — the IRA already provides it. The value of a fixed annuity inside an IRA is the guaranteed rate, principal protection, and lifetime income options. RMDs at age 73 apply to annuity balances held inside traditional IRAs.

What happens if the insurance company fails?

Your state’s life and health insurance guaranty association steps in to protect policyholders up to the state’s coverage limit, typically $100,000 to $500,000 depending on your state. Visit NOLHGA.com to find your state’s specific limits. Buying from carriers rated A- or better by AM Best significantly reduces this risk.

What is the difference between single-premium and flexible-premium?

A single-premium annuity is funded with one lump-sum payment at purchase. MYGAs, SPIAs, and DIAs are almost always single-premium. A flexible-premium annuity allows you to make an initial payment and add more money over time. Many traditional fixed annuities offer this option. If you are rolling over a CD or IRA, a single-premium product works naturally. If you want to contribute from ongoing income, look for a flexible-premium option.

Sources

- Internal Revenue Service. Publication 575: Pension and Annuity Income (2024). Covers tax rules for annuity distributions, exclusion ratio calculations, and early withdrawal penalties.

- Internal Revenue Service. Retirement Topics — Tax on Early Distributions. Rules and exceptions for the 10% early withdrawal penalty on annuity earnings before age 59½.

- Internal Revenue Service. IRA Contribution Limits. Current annual contribution limits for traditional and Roth IRAs funding qualified annuities.

- U.S. Federal Register. Required Minimum Distributions — Final Rule (2024). Finalized SECURE 2.0 Act rules including the $200,000 QLAC limit and elimination of the 25% account-balance cap.

- U.S. Congress. SECURE 2.0 Act of 2022 (H.R. 2954). Legislation raising the RMD age to 73 (and 75 in 2033), expanding QLAC eligibility, and other retirement plan reforms.

- National Organization of Life and Health Insurance Guaranty Associations (NOLHGA). NOLHGA.com. State guaranty association coverage limits and the process for protecting policyholders if an insurer becomes insolvent.

- National Association of Insurance Commissioners (NAIC). NAIC Annuity Resources. Consumer guidance on annuity regulation, suitability standards, and state-level insurance oversight.

- AM Best. Understanding Best’s Credit Ratings. Explanation of the AM Best rating scale used to evaluate insurance company financial strength and claims-paying ability.

- LIMRA. 2024 Individual Annuity Sales Results. Industry data on annuity sales volume by product type, including record MYGA sales driven by the interest rate environment.

- FDIC. Understanding Deposit Insurance. FDIC coverage limits ($250,000 per depositor per bank) referenced in the CD vs. fixed annuity comparison.

- Pacific Life Insurance Company. Understanding Fixed Annuities. Educational brochure covering fixed annuity types, contract structure, tax treatment, and the parties involved in an annuity contract.

- U.S. Department of the Treasury. TreasuryDirect — Bond Rates. Current Treasury bond and savings bond rates used for comparison with fixed annuity rates.

Keep Reading

Explore more: Income Annuities | MYGA vs CD | Types of Annuities | All Comparisons