What is an Immediate Annuity?

Immediate annuities are contracts with an insurance company that convert a lump sum into an income stream guaranteed for life or a set period of time, with payments beginning in the first twelve months.

You have spent forty years saving a nest egg, but now you face the hardest part of retirement planning: turning that pile of cash into a paycheck that lasts as long as you do.

The fear of running out of money is real. For many retirees, Social Security covers the basics, but a gap remains between those checks and the lifestyle they want. This is where a Single Premium Immediate Annuity (SPIA) fits in.

Think of a SPIA as buying a personal pension. You hand over a lump sum to an insurance company, and in return, they promise to pay you a guaranteed income for the rest of your life—or a set period—starting almost immediately. It is the oldest, simplest, and most transparent type of annuity available.

Here is a detailed breakdown of how SPIAs work, the returns you can expect, and whether trading liquidity for guaranteed income makes sense for your portfolio.

What Is a Single Premium Immediate Annuity (SPIA)?

A Single Premium Immediate Annuity is a contract between you and an insurance company where you pay a lump sum upfront in exchange for guaranteed periodic payments that begin within one year.

Unlike complex variable annuities or indexed products tied to the stock market, a SPIA is a straightforward transfer of risk. You give the insurer your capital; they take on the risk of you living to age 105.

The “Single Premium” refers to the one-time funding method. You cannot add money to this account later. The “Immediate” indicates that the income phase starts right away, typically 30 days after the contract is signed.

The Core Components

- The Premium: The lump sum you invest (e.g., $100,000).

- The Payee: The person receiving the income (usually you).

- The Annuitant: The person whose life expectancy determines the payment amount.

- The Carrier: The insurance company backing the guarantee.

How Does a SPIA Actually Work?

A SPIA works by pooling your money with thousands of other investors to create “mortality credits,” allowing the insurance company to pay you more than you could safely withdraw on your own.

When you buy a SPIA, the insurance company invests your money in conservative bonds and treasuries. However, your return isn’t just based on interest rates. It is based on three factors:

- Interest Rates: The yield the insurer earns on its portfolio.

- Principal Repayment: Part of every check you receive is simply your own money being returned to you.

- Mortality Credits: This is the unique advantage of annuities. The funds from annuitants who die earlier than expected subsidize the payments for those who live longer.

Because of mortality credits, a SPIA will almost always generate a higher monthly income than a bond or CD with a similar interest rate. The trade-off is liquidity. Once you hand over the check, that money is generally no longer yours to spend freely. It has been converted into an income stream.

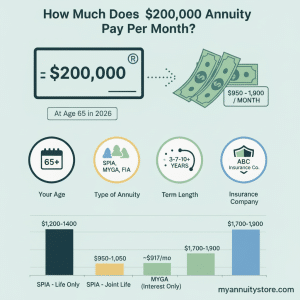

How Much Income Will $100,000 Buy in 2026?

The payout rate of a SPIA depends heavily on your age, gender, and current interest rates. Older buyers get higher payments because the insurance company expects to pay them for fewer years.

Below are estimated monthly payouts for a $100,000 investment in a “Life Only” SPIA (payments cease at death) based on current rate environments. You can use our immediate annuity calculator to see how much an annuity would pay you.

| Age / Gender | Monthly Income | Annual Payout Rate |

|---|---|---|

| 60 Male | $585 | 7.0% |

| 60 Female | $565 | 6.8% |

| 65 Male | $645 | 7.7% |

| 65 Female | $620 | 7.4% |

| 70 Male | $740 | 8.9% |

| 70 Female | $705 | 8.5% |

| Joint (65/65) | $545 | 6.5% |

Note: These are estimates for educational purposes. Actual quotes vary by carrier and daily interest rate changes. Read How Much Does a $100,000 Annuity Pay Per Month?

Real Scenario: The Income Gap

Consider Robert, age 66. He has $400,000 in savings and receives $2,200 from Social Security. His monthly expenses are $3,000. He has an $800 monthly shortfall.

Robert could withdraw from his portfolio, but he worries about market crashes. Instead, he takes $130,000 of his savings and buys a SPIA. This generates roughly $850 a month guaranteed for life.

His essential expenses are now fully covered by guaranteed sources (Social Security + SPIA). The remaining $270,000 in his portfolio can remain invested in the market for growth or emergencies, and he sleeps better knowing his bills are paid regardless of what the S&P 500 does.

What Are the Pros and Cons of Immediate Annuities?

SPIAs offer unmatched security, but they require giving up control of your capital.

The Advantages

- Longevity Protection: You cannot outlive the income. If you live to 102, the insurance company loses, and you win.

- Higher Cash Flow: Because you are consuming principal along with interest, the monthly cash flow is significantly higher than dividends or bond yields.

- Simplicity: There are no annual fees to track, no investment decisions to make, and no market charts to watch.

- Creditor Protection: In many states, annuity income is protected from lawsuits and creditors.

The Disadvantages

- Loss of Liquidity: This is the biggest hurdle. Once you buy the contract, you typically cannot ask for your $100,000 back to buy a vacation home or pay for a medical emergency.

- Inflation Risk: A fixed payment of $1,000 today will buy much less in 15 years. (You can add inflation protection, but it lowers your starting payment.

- Opportunity Cost: If the stock market booms, your annuity payments stay the same. You miss out on potential high growth.

SPIA Payout Options: Life Only vs. Period Certain

Your payout amount changes drastically based on the guarantees you add to the policy. The more risk you transfer to the insurer, the higher your check.

1. Life Only (Straight Life)

This option pays the highest monthly amount. Payments continue for as long as you breathe. However, when you die, the payments stop immediately. The insurance company keeps any remaining money.

- Best for: Maximizing income for a single person with no heirs.

2. Life with Cash Refund

This is the most popular option. It pays you for life, but if you die before receiving your total original investment back, the difference is paid to your beneficiaries.

- Example: You invest $100,000. You receive $20,000 in payments and then die in a car accident. Your beneficiary gets a check for $80,000.

- Trade-off: The monthly payment is usually 2% to 5% lower than the “Life Only” option.

3. Life with Period Certain

This guarantees payments for your life, and a minimum number of years (e.g., 10 or 20 years). If you die in year 3 of a 10-year period-certain annuity contract, your beneficiary gets the checks for the remaining 7 years.

- Trade-off: Lower payments than Life Only, but ensures the family gets something if you die early.

4. Joint Life Survivor

This covers two lives, typically spouses. Payments continue until the second person passes away. You can structure this to pay 100% to the survivor, or reduce it to 50% or 75% to increase the initial payout.

How Are SPIA Payments Taxed?

The taxation of your SPIA income depends entirely on the source of the money used to purchase it.

Qualified Funds (IRA/401k)

If you use pre-tax money from a Traditional IRA or 401(k) to buy the annuity, 100% of the income is taxable at your ordinary income tax rate. The IRS has never taxed this money, so they tax the entire distribution. This also satisfies Required Minimum Distributions (RMDs) for the portion of your IRA used to buy the annuity.

Non-Qualified Funds (Cash/Savings)

If you use after-tax cash (money sitting in a checking or brokerage account), the taxation is more favorable. The IRS uses an “Exclusion Ratio.”

Because you already paid taxes on the principal, the IRS considers part of every monthly check a return of principal (tax-free) and part of it interest (taxable).

- Example: You buy a SPIA with $100,000 of non-qualified cash. The exclusion ratio might be 80%.

- If your monthly check is $600, then $480 is tax-free. You only pay income tax on the remaining $120.

- This creates a very tax-efficient income stream for retirees in high tax brackets.

Is a SPIA Right for Your Retirement Plan?

A SPIA is not an investment for growth; it is an insurance policy for income. It belongs in the “safety” bucket of your portfolio.

You Should Consider a SPIA If:

- You have a longevity gap: Your basic living expenses exceed your Social Security and pension income.

- You fear spending your principal: Many retirees are afraid to withdraw from their savings. A SPIA automates the “decumulation” phase, giving you permission to spend.

- You want to simplify: You are tired of managing a bond ladder or worrying about rebalancing a portfolio.

- You are between 70 and 80: This is often the “sweet spot” where mortality credits kick in heavily, offering payouts significantly higher than standard interest rates.

You Should Avoid a SPIA If:

- You have poor health: If your life expectancy is significantly shorter than average, you will likely lose money on the deal.

- You have limited assets: If you have less than $200,000 in total savings, locking a large portion away in an illiquid contract is dangerous. You need cash accessible for emergencies.

- You are highly concerned with leaving a large inheritance: While “Cash Refund” options exist, a simple investment portfolio is usually better for maximizing legacy.

Strategies to Maximize Your SPIA Income

Don’t just buy the first annuity your local agent pitches. Use these strategies to get the most value.

1. The Laddering Strategy

Instead of dumping $200,000 into a SPIA all at once, buy smaller contracts over time.

- Buy a $50,000 SPIA at age 65.

- Buy another $50,000 SPIA at age 68.

- Buy a third at age 72.

This helps you catch different interest rate environments and take advantage of higher payouts as you age.

2. Inflation Protection (COLA)

You can purchase a Cost of Living Adjustment (COLA) rider that increases your payments by 2% or 3% annually.

- Warning: This is expensive. Adding a 3% annual increase might lower your starting payment by 20% to 30%.

- Alternative: Many advisors suggest simply buying a flat-payment SPIA and keeping a separate investment portfolio to grow and cover inflation later in life.

3. Shop the Market

Annuity rates are like mortgage rates—they vary wildly between carriers. For the exact same $100,000 deposit, Company A might offer $580/month while Company B offers $640/month. That is a $720 difference per year, for life. Always use an independent broker who can quote multiple carriers.

Frequently Asked Questions About SPIAs

What happens if the insurance company goes bankrupt?

Annuities are not FDIC insured. However, they are backed by State Guaranty Associations. If a carrier fails, the state association steps in to cover the policy up to a certain limit.

- Limit: Most states cover up to $250,000 in present value for annuity benefits.

- Strategy: If you plan to invest $500,000, split it between two or three different insurance carriers to stay within state coverage limits.

Can I get my money back if I change my mind?

Generally, no. Most SPIAs have a “free look” period (usually 10 to 30 days) after you sign the contract where you can cancel for a full refund. Once that period ends, the decision is irrevocable. You cannot cash out a SPIA like a CD.

Does a SPIA affect my Social Security taxes?

Yes and no. The income from a SPIA counts toward your “Provisional Income,” which the IRS uses to determine how much of your Social Security is taxable. If you use pre-tax IRA money, the full amount counts. If you use after-tax money, only the interest portion counts.

Is a SPIA better than a MYGA?

They serve different purposes.

- MYGA (Multi-Year Guaranteed Annuity): Acts like a CD. You park money for 3-5 years, it grows at a fixed rate, and you can take the lump sum back at the end.

- SPIA: Is for income now. You generally don’t get the lump sum back.

- If you need a monthly paycheck to pay the electric bill, get a SPIA. If you just want safe growth for your savings, get a MYGA.

The Bottom Line

A Single Premium Immediate Annuity is the most efficient way to turn a lump sum of cash into a guaranteed income stream. It isn’t exciting, and it won’t make you rich. But for a retiree worried about market volatility and outliving their savings, it provides the one thing a stock portfolio cannot: certainty.

Evaluate your “must-have” expenses. If Social Security doesn’t cover them, a SPIA is a logical tool to bridge the gap. Just ensure you leave enough liquid cash elsewhere for the surprises life inevitably throws your way.