What Is the Nasdaq FC Index (BOFANFCC)?

The Nasdaq FC Index (ticker: BOFANFCC) is one of the most widely used volatility-controlled indexes in fixed index annuities today. Designed by Bank of America, it applies patent-pending “Fast Convergence” technology to the Nasdaq-100 to rebalance as often as every hour, far more frequently than competing indexes that only adjust once per day.

If you own or are considering an Athene fixed index annuity, there’s a good chance the Nasdaq FC Index is one of your crediting strategy options. Here’s what you need to know about how it works, its historical performance, and whether it’s worth selecting.

What Is the Nasdaq FC Index (BOFANFCC)?

The Nasdaq FC Index is a volatility-managed version of the Nasdaq-100 Total Return Index. It was created on January 29, 2020 by Bank of America and targets 12.5% annualized volatility.

What makes it different from other volatility-controlled indexes is its Fast Convergence (FC) technology, a patent-pending rebalancing mechanism that adjusts exposure to the Nasdaq-100 as often as every hour during the trading day. Most competing indexes (like the S&P 500 Daily Risk Control) rebalance only once per day at market close.

This hourly rebalancing is designed to do two things:

- Reduce drawdowns faster, when volatility spikes intraday, the index can cut exposure before the close

- Capture upside more efficiently, when markets trend steadily higher, the index can apply up to 175% leverage to the Nasdaq-100

The result is an index that aims to deliver smoother, more consistent returns, which in turn allows insurance carriers like Athene to offer higher participation rates on annuity crediting strategies linked to it.

How Does the Nasdaq FC Index Work Inside an Annuity?

You don’t invest directly in the Nasdaq FC Index. Instead, you select it as a crediting strategy inside a fixed index annuity. The annuity carrier uses the index’s performance to calculate your annual interest credit, subject to a participation rate, cap, or spread.

For example, inside an Athene Performance Elite 7, the Nasdaq FC Index is available with these crediting options:

| Crediting Method | Term | Current Rate |

|---|---|---|

| Annual Point-to-Point w/ Participation Rate | 1 Year | 47% Participation |

| Biennial Point-to-Point w/ Participation Rate | 2 Year | 70% Participation |

How the math works: If the Nasdaq FC Index returns 10% over a 1-year period, you’d be credited 4.7% (10% × 47% participation). If the index returns -5%, you get 0%, your principal is protected from market losses. That’s the core value proposition of a fixed index annuity: upside participation with a floor of zero.

The Nasdaq FC Index is also available inside other Athene products, including the Athene Ascent Pro 10 and the Athene Aviator 5.

Why Do Carriers Use Volatility-Controlled Indexes?

This is the question most people skip, but it’s critical to understanding why the Nasdaq FC Index exists.

Insurance carriers fund your annuity’s upside potential by purchasing options on the underlying index. The cost of those options depends heavily on the index’s implied volatility, the more volatile the index, the more expensive the options, and the lower the participation rates they can offer you.

Volatility-controlled indexes like BOFANFCC are designed to maintain steadier, more predictable volatility. This makes the options cheaper, which allows carriers to offer higher participation rates compared to the raw Nasdaq-100 or S&P 500.

The trade-off: in a straight-up bull market with low volatility, a volatility-controlled index may underperform the raw index. But in choppy or declining markets, the volatility management can significantly reduce losses, which matters when your annuity measures performance over fixed periods.

Historical Performance

The Nasdaq FC Index launched on January 29, 2020, right before the COVID crash, which makes its early track record an interesting stress test.

Key performance data points:

- During Q4 2021, the Nasdaq-100 returned over 11%. The Nasdaq FC Index captured 7.4% of that return.

- Exposure to the Nasdaq-100 ranged from a low of 42.3% to a maximum of 175% over that period.

- In October 2021 specifically, the FC Index captured 72% of the Nasdaq-100’s 7.9% return (5.7% vs 7.9%).

- When volatility spiked in early December 2021, the index rapidly cut exposure below 50%, preserving prior gains.

Source: Bloomberg, BofA Securities. The index was created on 1/29/2020. Data before that date represents hypothetical backtested performance. Past performance is not indicative of future results. The index includes a 50bps fee drag.

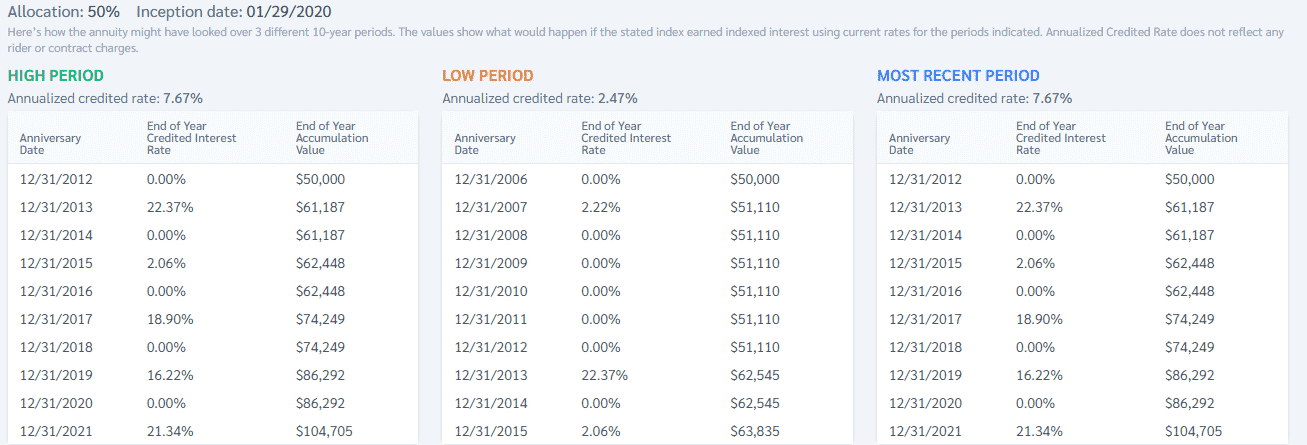

Hypothetical Performance Inside Athene Performance Elite 7

The tables below show what a $50,000 allocation to the Nasdaq FC Index crediting strategy might have returned inside the Athene Performance Elite 7 over three different 10-year backtested periods.

2-Year Point-to-Point (70% Participation Rate):

1-Year Point-to-Point (47% Participation Rate):

These are hypothetical illustrations based on backtested data and current participation rates. Actual credited rates will vary. Annualized credited rates do not reflect rider or contract charges.

Nasdaq FC Index vs. Other Volatility-Controlled Indexes

The Nasdaq FC Index competes with several other volatility-managed indexes commonly found in fixed index annuities:

| Index | Underlying | Vol Target | Rebalancing |

|---|---|---|---|

| Nasdaq FC (BOFANFCC) | Nasdaq-100 | 12.5% | Hourly |

| S&P 500 Daily Risk Control 5% | S&P 500 | 5% | Daily |

| BNP Paribas Multi Asset Diversified 5 | Multi-asset | 5% | Daily |

| Barclays Atlas 5 | Multi-asset | 5% | Daily |

The Nasdaq FC’s 12.5% volatility target is notably higher than most competitors, which typically target 5%. Combined with the hourly rebalancing and ability to apply up to 175% leverage, it’s among the more aggressive volatility-controlled indexes, which can mean higher highs in trending markets but also wider swings in choppy conditions.

Which Athene Annuities Offer the Nasdaq FC Index?

The Nasdaq FC Index is available as a crediting strategy in several Athene fixed index annuities:

- Athene Performance Elite 7, 7-year surrender, annual and biennial PTP options

- Athene Ascent Pro 10, 10-year surrender, higher participation rates for longer commitment

- Athene Aviator 5, 5-year surrender, shorter commitment with competitive rates

- Athene Agility 10, 10-year surrender with bonus

For a full overview of Athene’s product lineup, AM Best ratings, and company background, see our Athene Annuity Review.

Should You Choose the Nasdaq FC Index in Your Annuity?

The Nasdaq FC Index makes the most sense if you:

- Want growth-oriented exposure, the Nasdaq-100 skews heavily toward technology and innovation companies

- Are comfortable with a higher volatility target, the 12.5% target means more market exposure than a 5% vol-controlled index

- Have a longer time horizon, the 2-year point-to-point option (70% participation) tends to smooth out short-term volatility

- Want to diversify your crediting strategies, most advisors recommend splitting your allocation across 2-3 indexes rather than going all-in on one

It may not be the best fit if you’re extremely conservative and would prefer a lower-volatility index with less exposure to tech-heavy sectors. In that case, a strategy linked to the S&P 500 or a multi-asset index may provide a smoother ride.

Not sure which crediting strategy is right for you? Request a free quote and we’ll walk you through the options based on your goals.

Frequently Asked Questions

What is the Nasdaq FC Index?

The Nasdaq FC Index (BOFANFCC) is a volatility-managed index designed by Bank of America that applies Fast Convergence technology to the Nasdaq-100 Total Return Index. It rebalances as often as hourly to manage exposure, targeting 12.5% annualized volatility. It’s used as a crediting strategy option inside certain fixed index annuities.

Can you lose money with the Nasdaq FC Index in an annuity?

No, if the Nasdaq FC Index returns a negative number over your crediting period, your annuity is credited 0% for that term. Your principal is protected from market losses. This is a core feature of all fixed index annuities. However, if you surrender your annuity early, surrender charges could reduce your account value.

Why is the participation rate lower than 100%?

Insurance carriers purchase options on the index to fund your upside. The participation rate reflects how much of the index’s return they can afford to pass on to you after accounting for the cost of those options, their own expenses, and the downside protection guarantee. Volatility-controlled indexes like BOFANFCC typically allow for higher participation rates than raw market indexes.

Is the Nasdaq FC Index better than the S&P 500 for annuities?

Neither is inherently “better.” The Nasdaq FC Index offers exposure to tech-heavy Nasdaq-100 companies with hourly rebalancing, while S&P 500-linked strategies provide broader market exposure. Many annuity owners split their allocation across multiple indexes. Your best mix depends on your risk tolerance and market outlook.

Which annuities offer the Nasdaq FC Index?

The Nasdaq FC Index is primarily available in Athene fixed index annuities, including the Performance Elite 7, Ascent Pro 10, and Aviator 5. For Athene’s full product lineup and ratings, see our Athene carrier review.